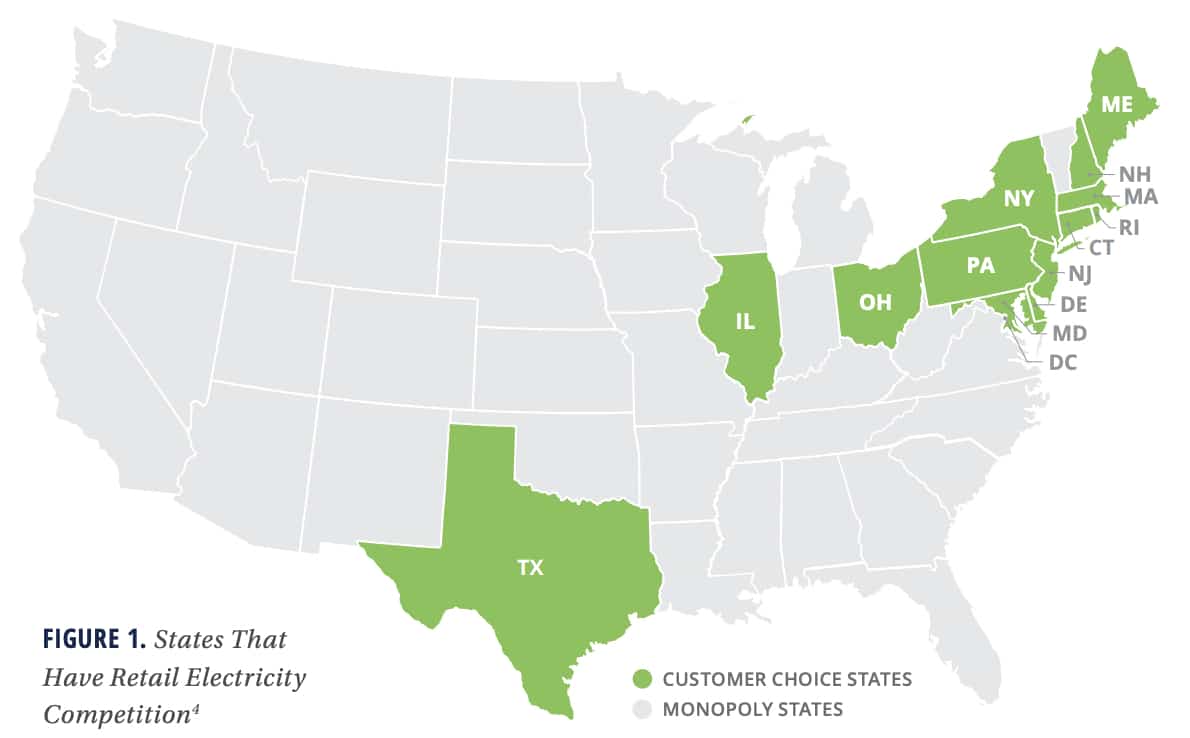

NRG Energy signed 1,300 MW of solar power purchase agreements (PPAs) in Texas last summer, thanks to Texas retail competition policies that create favorable conditions, says Travis Kavulla, NRG Energy’s vice president of regulatory affairs. Yet those conditions are missing in the 13 other states that have retail competition, “where utility incumbents still dominate,” he said. (Those other states are shown in the map above.)

Texas, where NRG Energy is a competitive retail electricity provider, gives all retail providers “a significant incentive” to reduce the impact of price swings in the wholesale power market by entering long-term supply arrangements such as PPAs, said Kavulla.

In the other 13 states with retail choice in the Northeast and Midwest, program attributes have created roadblocks that prevent retail power providers from signing solar PPAs or otherwise securing long-term power supply, says a report from Wind Solar Alliance, which Kavulla calls “a major contribution to the conversation.” (The 34-page report was written by Rob Gramlich of Grid Strategies and Frank Lacey of Electric Advisors Consulting.)

As a result, although many retail choice states have policy goals to increase renewables generation, their retail providers are not in a position to help meet those goals, said Kevin O’Rourke, executive director of the Wind Solar Alliance.

Lower prices

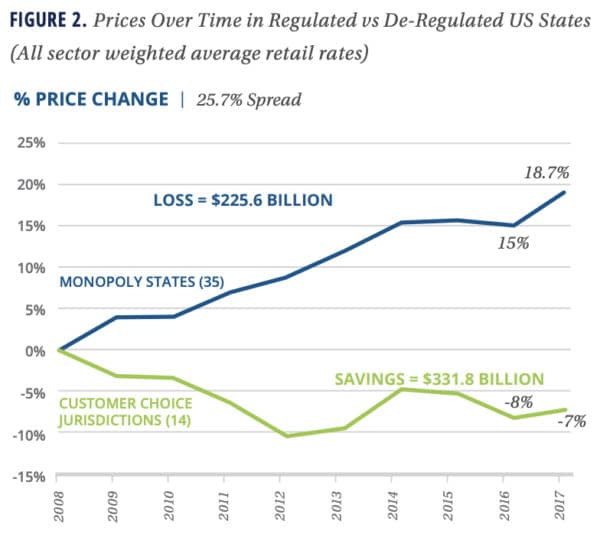

The good news across retail choice states is that electricity customers benefit, says the report, from “much lower” prices for electricity than consumers in states with monopoly utilities, partly because reductions in wholesale power prices have been passed on to retail customers more quickly in retail choice states. Over a nine-year period, price increases in monopoly states cost customers $226 billion, while price reductions in retail choice states saved customers $332 billion:

Renewables investments

The report gives Texas a grade of “A” for affording retail providers an incentive to invest in generation resources, including low-cost renewables, while three other states considered in case studies—New Jersey, Maryland and Pennsylvania—receive far lower grades.

In Texas, retail suppliers are not pitted, as in other retail choice states, against an incumbent utility that may be favored in ten different ways, says the report.

For example, a typical rule in the 13 states besides Texas assigns all customers to the incumbent utility unless they opt out, whereas in Texas, customers must choose a provider in order to obtain electric service. And in the other states, incumbent utilities can undercut retail competitors on price as they shift “about 1-2 cents per kWh,” says the report, from the power prices they charge their retail customers to the distribution (wires) charges for which they bill everyone in their distribution area.

The report details other provisions that limit the ability of retail energy providers (REPs) to enter long-term contracts for generation resources. In all retail choice states, “Since REPs are never sure how much of their contracted customer load will stay with them from year to year, there is a role for another sort of entity to share in the risk of long-term contracting,” says the report. In Texas, it adds, “intermediaries that are financial players will often directly sign the contracts with generation on one side, and with REPs on the other side. As end-users shift from one REP to another, the intermediary experiences little risk, because the load still exists and is willing to buy the power they own.” In other words, in Texas the load cannot shift away from the REPs back to an incumbent utility, because there is none.

In the retail choice states besides Texas, while some retail providers market “100 percent clean” electricity, these retailers cannot drive development of new renewable resources, “because they do not make direct purchases of renewable energy from developers,” said Kevin O’Rourke, executive director of the Wind Solar Alliance. “Instead, they buy energy from the wholesale grid operators and are forced to buy generic capacity resources from the heavily regulated capacity constructs,” he said.

Adequate capacity

While the report does not focus on capacity markets, it notes that Texas—specifically, the ERCOT grid—does not have a capacity market. Even so, Texas has continued to meet peak demand, as documented by the North American Electric Reliability Corporation.

Meanwhile, in the PJM, NYISO, and ISO-NE grid regions where other retail choice states are located, says the report, “capacity payments make up around 30 percent of the value of the total wholesale energy market.”

In Texas, adequate capacity, also called reserve margins, “are produced because suppliers build enough to cover their obligations under contracts to deliver to their REP customers, and the REP customers have the incentive and ability to pay for enough capacity to cover various scenarios including generator outages,” says the report.

Australia, New Zealand and the United Kingdom also use the Texas approach to retail choice, says the report, which notes that “scarcity-based prices can reach $9,000 per MWh in Texas and $14,000 per MWh in Australia. Those prices can be thought of as speeding tickets or penalty payments for those who leave themselves too exposed by failing to procure the resources they need.”

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

Deregulation is the path to take. I have made this argument to Kentucky’s Public Service Commission as well, as the utilities try to destroy residential solar in Kentucky through government intervention. As a consumer, private citizen and plain old human being, I do not want government involved in my success or failure, I will lose almost every time. As an individual, I can’t buy an elected official a steak dinner! As a former elected official myself, I am pretty familiar as to how this works.

“”Australia, New Zealand and the United Kingdom also use the Texas approach to retail choice, says the report, which notes that “scarcity-based prices can reach $9,000 per MWh in Texas and $14,000 per MWh in Australia. Those prices can be thought of as speeding tickets or penalty payments for those who leave themselves too exposed by failing to procure the resources they need.””

Summer in Brisbane Australia or in Austin Texas can be unbearable and these rate spiking “periods” of $9/kWh to $14/kWh of electricity use only needs a few hours of this type of electricity pricing a month to double, maybe triple an electric bill. Folks need solar PV and ESS installed on their residences and small businesses to protect them from this type of “regulatory usury”. This rate spiking shows the Achilles heel of Deregulation. It is actually a “disincentive” for utilities to install alternative non-fueled energy generation and quickly get rid of old fueled generation assets, a majority of which have not amortized yet. That $9 to $14/kWh passed along to the ratepayers will allow that amortization of old fueled generation assets sooner than later IF these power entities (don’t) install more non-fueled generation capacity and continue to depend on high dollar fueled generation to meet grid demands. This is not working like those who proposed the deregulation of the electricity market first envisioned it. This will require many residential individuals to install and use their own solar PV with ESS for their home’s energy needs. I can see the electricity marketplace shifting to an “on demand” merchant energy market, where electricity price spiking could come along in as little as 15 minute or perhaps even 1 minute use periods. This will require smart ESS technologies to track actual battery energy storage with solar PV output and the home’s energy requirements to determine when to use battery power to offset merchant rate spiking times of the day, which could shift during the day depending on what’s going on with grid demands and responses. A national holiday’s merchant energy use will look different than the work day energy use.

The people I know in Texas have plans that allow up to XkWh per month and don’t include demand or peak charges so they wouldn’t suddenly have their bills double or triple.

The build out of solar PV in Texas is going to squash these $9-14/kWh pricing either this year or next year depending on how fast the PV can get in the ground in Texas.

I read about a coal plants in San Antonio that were making lots of money off these extreme prices. Can’t wait to read the story about them having to shut down because of all the money they are losing to PV.

Also, on utilitydive yesterday they had a story about coronavirus cutting demand and peak. Basically a lot of weekday grids are starting to look like weekend grids. Italy has seen an 18% to 21% reduction in peak demand and energy use on a year-over-year basis. Depending on how long it takes to deal with the coronavirus it could bring about interesting things in electricity demand.