Many US states offer incentives to promote residential rooftop solar adoption; however, as prices of solar have declined, the incentives have phased down or out. The truth remains, though, that for low- to moderate-income (LMI) households, the relatively high up-front costs of going solar are often a deterrent.

Eric O’Shaughnessy, a researcher at Lawrence Berkeley National Lab, studied the importance of subsidies in driving solar adoption among LMI households. His report, “Rooftop Solar Incentives Remain Effective for Low- and Moderate Income Adoption,” indicates that incentives drove adoption for about 80% of LMI households that otherwise would not have gone solar – implying that ongoing incentive support will be rewarded by strong solar policies.

Definitions vary, though a common definition for low- to moderate-income in the United States is earning less than 80% of the area median income. In California’s San Francisco County, for example, the household would have to make less than around $95,310 to qualify. In Connecticut’s Fairfield County, the cutoffwould be around $78,031.20.

According to another recent LBL report, “Residential Solar-Adopter Income and Demographic Trends: 2022 Update” a large number of solar adopters in 2020 could be considered “middle income” – 32% have household incomes in the $50,000 to $100,000 range. Solar adopter incomes skew high relative to the population at large: Median income of all US households was $63,000 in 2020, compared to $115,000 for 2020 solar adopters.

LBNL

According to O’Shaughnessy, it was important to study LMI solar incentives to understand whether these incentives are still driving adoption. Broader incentives have phased out because incentives become less influential in adoption decisions as prices decline. It is generally inefficient to continue offering incentives to households who would have adopted otherwise. However, even if incentives no longer drive adoptions among high-income households, incentives could still play a role in supporting LMI solar markets.

Two programs

Many states offer some form of incentives to help LMI households go solar including rebates, production-based (such as a renewable energy certificates), or tax credits. “A real disadvantage for LMI households is that many lack the tax appetite to directly benefit from tax credits,” said O’Shaughnessy. His Berkeley Lab study focuses on the California Single-Family Affordable Solar Homes program and the Connecticut Solar for All program, examining the impacts these programs have had on LMI solar adoption. He chose these programs because they’re relatively large and have many years of data.

California has by far the largest subsidy program, putting aside 10% of its California Solar Initiative funds to support LMI. “The maximum deployment could be 10% of the program’s total, but in reality, it is far less,” O’Shaughnessy said. He explained that to subsidize a typical relatively highincome adopter, “they were motivated by partial subsidies that reflected relatively small portions of the system cost.” But with the LMI programs, which are trying to promote equity, the subsidies are more generous per customer. “When a state has a 10% carve-out for LMI program funding but LMI incentives are higher per customer than other incentives, you’ll have proportionally fewer installations,” said O’Shaughnessy.

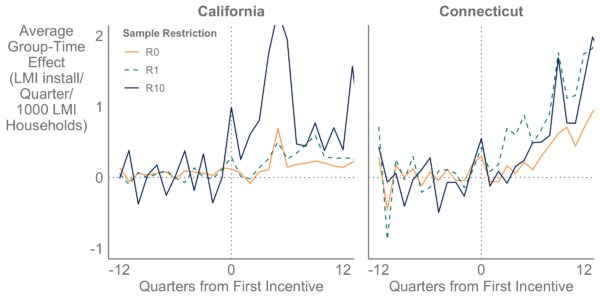

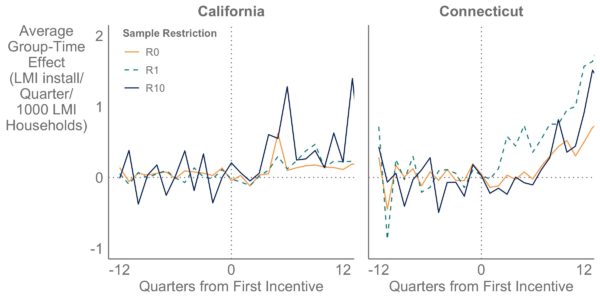

The study found that in the cases of California and Connecticut, LMI solar subsidies increased solar adoption. Through econometric analysis, the Berkeley researchers estimate that roughly four of five LMI subsidy recipients in California and Connecticut would not have adopted solar without some kind of subsidy. In addition, the research shows that the programs had sustained impact over several years, showing spikes that occur at the time the subsidies are offered, and then adoption spikes back up.

Eventually you

are giving incentives

to households who

would have adopted

anyway and at that

point the incentives

aren’t effective

anymore. Eric O’Shaughnessy

The reason for the spike could be that the programs continue to reach new people, that installers continue to market in specific LMI areas, and that some wait until others have successfully navigated the process before jumping in themselves. Another effect of LMI incentive programs is that some LMI households chose to adopt solar even without receiving subsidies, and this is called “spillover.”

Spillover theory

In his report, O’Shaughnessy directly tests the spillover hypothesis by looking at areas where LMI incentives are offered and then exploring changes in adoption patterns among households that did not receive incentives. Previous research shows that when a neighbor sees that a neighbor has installed solar, they become interested and are “primed” for adopting solar themselves. It appears that is still true for LMI households, O’Shaughnessy said. Some of the spillover customers will qualify for incentives, and others may even install it themselves without incentives, according to O’Shaughnessy.

Targeted incentives

While the overall conclusion of the report is that targeted incentives are a key component of nascent LMI rooftop markets, the question remains as to how long these markets will be nascent. O’Shaughnessy said that they still are, but that may be changing. The study found that eight out of 10 recipients would not have installed solar without some form of incentive, but that will decline over time.

O’Shaughnessy explained that, for example, the number of households that would not install solar without the incentive would soon be seven out of 10, then six out of 10, and so forth. “Eventually you are giving incentives to households who would have adopted anyway and at that point the incentives aren’t effective anymore,” said O’Shaughnessy. “It’s not effective because those customers don’t need the incentive, prices have come down and the market has taken over.”

The issue of rooftop solar equity is an emerging trend that has somewhat tarnished the image of solar and undermined public support because people see solar customers as those with high incomes. Utilities and regulators are obligated to deliver energy that is just and reasonable to everyone, regardless of income.

The Rooftop Solar Incentive report notes that fewer than a quarter of PV adopters are LMI households. “If solar were perfectly equitably adopted then 50% of adopters would earn less than the national median, but instead about a quarter earn less than the median – so there is the equity gap,” O’Shaughnessy said. The good news, though, is that it is changing. Just like any technology, O’Shaughnessy said, “it expands and diffuses.” As you get more LMI households adopting solar, the average income of adopters goes downyear over year.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

Utilities, Like PG&E in California, require a system of at least 2,000 watts of solar panels with a grid tied inverter before you can even apply to grid connect for a $145.00 fee. The city of Union City, California requires a $395.00 permit fee every time you install or additionally install solar panels or equipment. The minimum sized system would cost $6,000.00 for the system, $395.00 for permits and $145.00 for the utility connection or $6,540.00 for the minimum system installed by a licensed contractor if you could find one. Most contractors want you to install a minimum size 4,000-watt system because the costs of doing the job per unit are reduced the more solar the customer puts in. That brings the price up to $12,540.00 for the 4,000.00 system and for low-income people, that pay no Federal income taxes, the Federal Solar Tax Credit does not apply. If they made the “solar tax credit” like the “child tax credit” that is a real government refundable credit, then maybe more low-income people would be able to install the discounted rooftop solar. The $3120.00 Federal tax credit could potentially lower the cost of a 4,000-watt system to $9,420.00 after permits and utility connection fees. With a Federal or State sponsored 5% interest fully amortized solar loan for 10 years The monthly payment would be $98.00 per month. A well placed, unshaded 4,000-watt system will produce 5400 kilo watt hours per year of clean renewable power or about 450 kilo watt hours per month. Where utilities charge 27.5 cents per kilo watt hour, like PG&E in California, that would normally cost $121.50 per month, the savings would basically pay for the solar under NET metering NEM-2.0. If NEM-3.0 was implemented the savings would disappear and the system would never pay for itself.

Anything we can do to boost residential PV is a good thing. How about adding the cost of the PV to the mortgage? So the homeowner pays maybe $10 more/month, instead of a big lump sum?

Do the math. Every $1,000.00 you add to the loan of thirty years (360 monthly payments) you add about $5.00 when you include interest at around 6%. Higher interest rates the monthly amount goes up. On a new home, the purchase price is the property tax base price so the solar would become taxable on the property tax bill unless the state has a waiver. A 4,000-watt system, costing $12,000.00 would add about $60.00 to the monthly payment for 30 years eventually costing $21,660.00. The utility savings, at today’s PG&E rates that you know will be going up every one of those 30 years so a minimum savings of $121.00 per month times 360 equals $43,740.00 and even as the panels degrade to 80%, the accumulated savings of the utility bills would be in excess of $34,992.00. $34,992.00 – $21,660 = $13,332.00 net profit on the deal. If you get a 10-year solar loan and pay 120 X $98.00 = $11,760.00 after a real Federal Solar tax Rebate would give a net profit of $34,992.00 – $11,760.00 = $23,232.00. With a 30-year loan you give about $10,000.00 in your net gain to the bank in the form of mortgage interest, but you would still come out ahead. The figures change depending on the Federal Solar Tax Credit and how you apply it to the loans. I personally do not like adding appliance upgrades, solar panels or other depreciating things to the mortgage and tax base but purchase them separate because when they wear out, you are still paying for them in the taxes and interest even after you buy their replacements.

Yeah, there’s gotta be a way to get everyone on board. I’d like to see panels or solar roofs on all new homes. Prices continue to drop and efficiency goes up. Panel life is still not certain; today’s panels lose maybe 1% output/yr, but no one knows how long they will last. 50 years from now they could still be making juice.

California seems schizophrenic. They want solar, they require it on all new houses, yet the utilities make it hard and expensive. And the Federal tax credit should instead be a direct payment to the homeowner, regardless of his/her tax situation.

Rooftop solar initiially was very attractive to customers with ample means wanting to take advantage of the 30% FETC, currently 26% and phasing out to zero in 2024. “Free electricity” eventually. Why not?

Utility scale solar in Florida has a capacity penetration 5X that of rooftop’s 0.6% to 1%, depending on the utility. With installed costs of ~$1.00/W on the ground, or less than 1/4th that for rooftop it’s no wonder.

Recently announced plans for tens of 75-MegaWatt solar farms by Duke, FPL and TECO should have Florida at 25% to 30% solar with some battery storage by 2030. All their utility customers should ultimately benefit by lower generation costs and especially associated environmental bennies like a lower sea-level increase rate that doesn’t appear in ones’ bills.

Many rooftops are unsuitable for solar due to orientation, shade and age. One must own their roof to install solar, leaving renters, many HOA and most Condos, especially condo towers out of the mix.

Utility scale solar is ultimately the way to go since it should lower costs to all while making a more substantial environmental impact than rooftopcs scale and timeframe.

Duke’s recently launched Clean Energy Connection (CEC) program has a LMI set-aside, but buying Duke Stock [DUK] with 3.65% dividend has a 2X better return than the 4-Cents/kWh usage credit for all subscribers, and investors can choose how much to invest and where to spend their earnings, including reducing their water bills. Investment in assets accumulate year over year, unlike CEC’s monthly debited subscriber fees.

The prevailing incentive for rooftop solar was “effectively wiping out one’s high electric bill with net-metering” and “free electricity” after break-even primarily in northern and western states. Especially where TAX FUNDED funded rebates and incentives along with “magical deregulation” made rates worse, MUCH WORSE!

As solar penetration increased, bills became a tad (0.5% to 1% in Florida) higher as solar shove off costs in rates affected non-solar customers and politics come to the fore to rectify real or imagined negatives associated with rates vs environmental impacts. Net-metering caps for one.

Plants, poles, wires and transformers don’t last forever. And a non-monopoly mix of Tom, Dick and Harry electric companies with a mix of separate and shared distribution assets would lead to litigated finger pointing when there’s a blackout and solar customers’ inverters remain OFF even when the sun is shining.

FETCs have been subsidized by all of us tax payers since 2005. They’ll continue at 10% for commercial & industrial inatallations, meaning utilities will continue to benefit. And businesses depreciation writedowns are icing on the cake residential rooftop solar customers can’t lick. Like loss of $Billion$ of fuel/road taxes due to E-Vehicles, states are scrambling to balance a variety of inequities so as to be fair to all. And Legi$lated $olutions always come at a price.

While net-metering sounded good at the outset, it may have run its course at sunset with the reality that net-metering doesn’t work for food, fuel, water or sewage finally obvious to everyone.

That Monopoly Utilities, especially investor owned ones like Duke, pay a much better dividend than savings accounts and money markets provides a non-solar option to everyone to tailor their lifestyle to live within their abilities and means.

Otherwise State Government, or worse Federal monoplies like our USPS delivering junk mail and Amazon stuff will be the end result.

I don’t remember wishing for all of this when I paid cash for my 9.5kW rooftop solar in 2015. It just sort’a happened…😜