The next decade and beyond are going to bring about development in the battery and energy storage sector the likes of which the world has yet to see. And, while this is an idea that has been gaining momentum for a time now, a new report by Rocky Mountain Institute represents a more rapid shift than has been predicted, one not necessarily lead by lithium-ion.

The report, Breakthrough Batteries, outlines how increased demand for electric vehicles (EVs), grid-tied storage, and other emerging battery applications, in conjunction with cost and performance improvements are fueling a cycle of cycle of investment and cost declines.

In just the first half of 2019 alone, we have seen more than $1.4 billion invested in battery technologies. According to the report, the total investment in battery manufacturing, both previous and planned, until 2023, represents around $150 billion. What’s more is that projections of the advancement that these investments can drive are not linear. What that means is that as the capital cost for new planned battery manufacturing capacity drops (RMI predicts that drop to be 50% by 2023), technologies become cheaper and that money can drive even greater adoption.

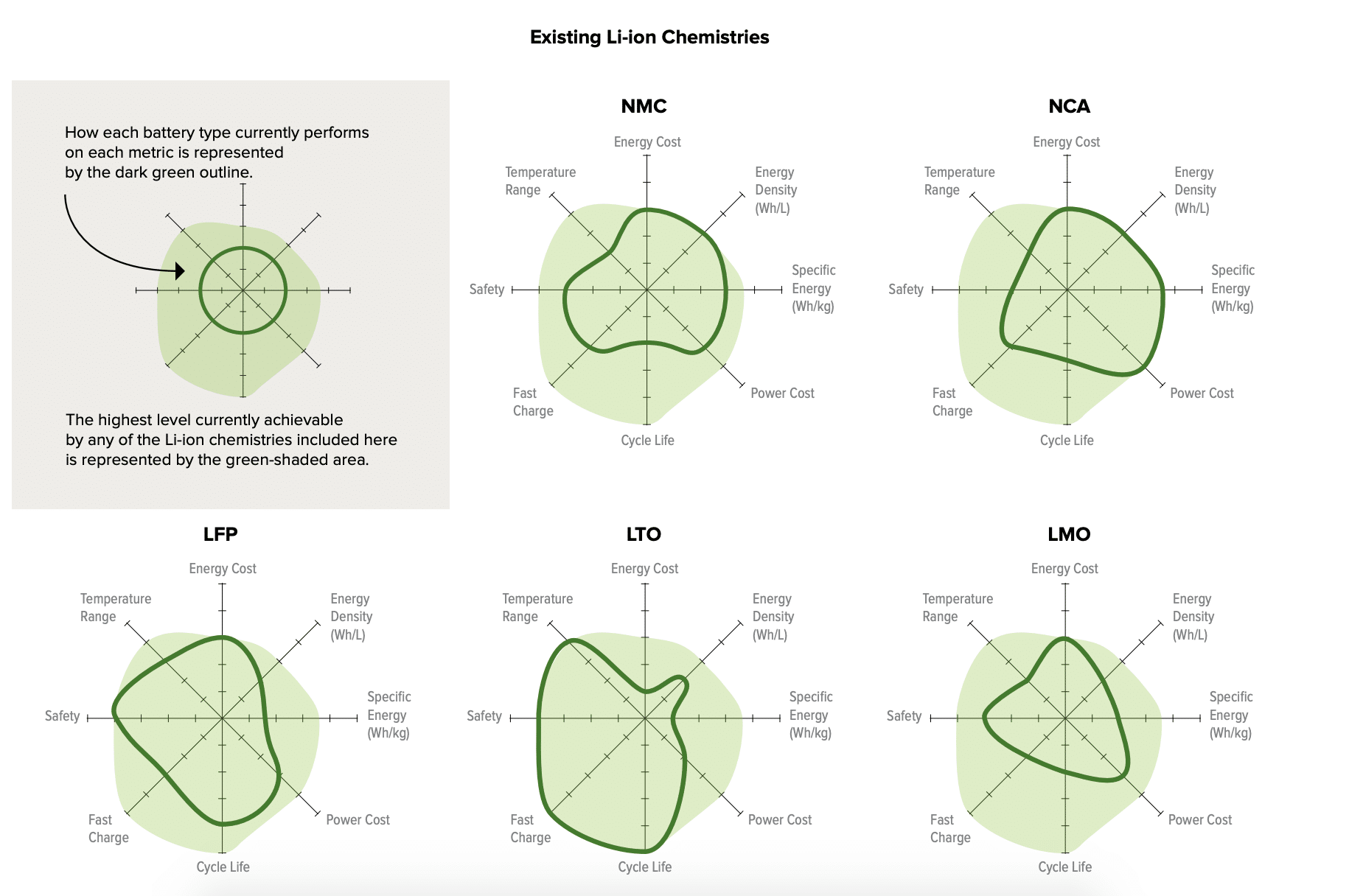

So what are the technologies that will lead us into this battery powered brave new world. Well, according to RMI, much of the same, or at least derivatives of the same, until 2025. The word same, in this instance, is referencing lithium-ion (li-ion) technologies. However, in opposition to what has been seen in the solar energy industry, the efficacy of li-ion batteries will come from the diversity available. Each different ionic compound in the various forms of li-ion batteries has specific strengths and weaknesses over its brethren, as displayed in the provided graphic:

All that is said to also say that li-ion batteries are not a perfect technology. Li-ion technologies may be outcompeted by other technologies based on the requirement of costly thermal management systems, providing an inherent risk of fires, the incremental improvements in energy density not matching that of future competition and the necessities of li-ion batteries to reach 100% depth of discharge and double their current duration life to even compete with emerging technologies from a hardware perspective.

But enough conjecture, what are these emerging technologies that have li-ion batteries shaking in their boots? The report identifies three categories:

Solid state batteries, such as rechargeable zinc alkaline, Li-metal, and Li-sulfur that will help electrify heavier mobility applications; low-cost and long-duration batteries, such as zinc-based, flow, and high-temperature technologies that will be well suited to provide grid balancing in a high-renewable and EV future; and high-power batteries, which are well positioned to enable high penetration and fast charging of EVs.

The projection by RMI is that, regardless of the favored technology, battery technology will contribute to the replacement of natural gas plants and gain a foothold in other new market segments, including heavy trucking and short-range aviation.

These projections, along with the 2.5 GW of battery storage predicted by the U.S. Department of Energy to be on-line by 2023 portray a rapidly changing energy future.

To date, the United States has only completed 899 MW of operating battery storage. And while that figure is anticipated to reach 1 GW by year’s end, even then this is 1/67th of the total installed solar capacity and an even smaller percent of installed renewable energy capacity. From the end of 2014 to this past March, the volume of installed battery storage increased more than four times from 214 MW to 889. With that kind of exponential capacity jump already existing. it is of little doubt that greater strides can be made as the technologies and manufacturing become more advanced and cheaper.

We’ve said it before at pv magazine and we’ll say it again (because we like saying it): We have seen the future and there are batteries there, lots of them.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

Good Paper and excellent presentation.

I would request PV Team to publish detailed findings of fire in Li-ion storage battery in New York and other places. Is the fire result of high temp. defective ventilation, some chemical imbalance, platform software in accurate performance, etc.

Irrespective of designer, manufacturer, erector, transporter ,operator, the report shall clearly mention responsibility of each.

Where does stacked concrete storage fit into the mix of electric storage. It seems to me that the storage of excess electricity could be managed rather inexpensively with little risk of chemical Pollution by utilizing a potential energy storage system.