After years of declining technology costs, federal incentives, and state-level net metering programs that helped drive growth, policymakers are now asking a more nuanced question: how can they keep distributed solar growing while addressing affordability, grid constraints, and changing utility cost structures?

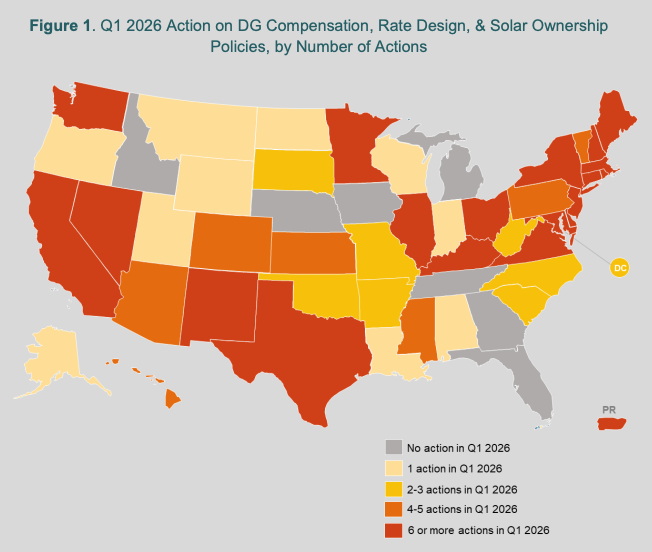

That tension is central to the North Carolina Clean Energy Technology Center’s 50 States of Solar: Q1 2026 Quarterly Report, which tracked 253 distributed solar policy and rate design actions across 44 states, Washington, D.C., and Puerto Rico during the first quarter of 2026.

Most actions focused on distributed generation compensation rules, interconnection rules, and community solar, signaling that states are increasingly examining how distributed solar connects to the grid, interacts with grid operations, and receives compensation for its value.

The report suggests that distributed solar policy is moving beyond the earlier era of broad market enablement. States are no longer simply deciding whether to support rooftop solar, community solar, third-party ownership, or customer generation. Instead, they are refining program rules, rethinking compensation structures, and designing new frameworks intended to balance customer adoption with utility system costs and grid reliability.

The policy activity comes as solar and storage continue to scale rapidly across the broader U.S. power sector. The U.S. Energy Information Administration expects developers to add a record 86 GW of new utility-scale generating capacity in 2026, with solar accounting for 51% of planned additions and battery storage another 28%.

At the distributed level, Berkeley Lab’s latest dataset includes roughly 4.5 million individual distributed solar and solar-plus-storage systems installed through the end of 2024, underscoring why state regulators are increasingly focused on compensation, interconnection, and rate design.

Distributed generation

The largest category of activity during the quarter was distributed generation compensation, with 61 actions across 27 states and Puerto Rico. Interconnection followed closely, with 51 actions across 20 states, Washington, D.C., and Puerto Rico. Community solar accounted for 46 actions across 20 states and Puerto Rico, while residential fixed-charge or minimum-bill increases accounted for 43 actions.

The core policy debates shaping distributed solar are no longer limited to net metering. They now include how quickly projects can interconnect, how exports are valued, how shared solar programs are structured, and how utilities recover costs as more customers adopt behind-the-meter generation.

California, a state that has long served as a trend indicator for the U.S. solar industry, remains one of the most closely watched examples. During the quarter, the state’s First Appellate District Court of Appeals upheld Net Energy Metering 3.0, the state’s net billing structure that accounts for customer production and consumption in real time and compensates for exports based on avoided costs. Plaintiffs argued the structure failed to account for the broader social benefits of customer-generated power, but the court found that the program met regulatory requirements.

Rhode Island is moving through a similar policy review process. Governor Daniel McKee issued an executive order directing the state Office of Energy Resources to review Rhode Island’s net metering program and Renewable Energy Growth Incentive Program. The review aims to control program costs and prevent undue financial burdens while continuing to support emissions reductions.

Connecticut regulators also released a report recommending successor structures for both net metering and community solar. The proposal calls for a unified program designed to provide long-term market stability, with lower credit rates and instantaneous netting for future residential net metering, standard offer credit rates and budget-based caps for non-residential net metering, and a future community solar program targeted specifically to low-income customers. In early May, the Connecticut General Assembly passed HB 5340, which aligns significantly with the regulators’ report. The bill is now with Governor Ned Lamont for signature.

Community solar

One of the clearest examples of the shift toward a focus on market design is in community solar. New Jersey Governor Mikie Sherrill issued an executive order directing the Board of Public Utilities to accelerate solar deployment through the state’s Competitive Solar Incentive program and release 3,000 MW of capacity for registration under the Community Solar Energy Program. Since the order was signed, regulators have released a new solicitation, allocated new community solar capacity to individual utilities, and issued new rules addressing community solar credits and project registration.

At the same time, several states are using community solar as an energy affordability tool. Maryland lawmakers passed legislation to study an opt-out community solar model aimed at low-income customers. New Jersey revised eligibility rules so that new community solar systems must provide at least a 20% bill discount to all subscribers and at least a 25% discount to low-income subscribers. Washington established a new treasury account to improve energy affordability through community solar. At the same time, Illinois revamped incentives for low-income solar, and Nevada regulators approved changes to NV Energy’s Expanded Solar Access Program to target low-income customers exclusively.

This affordability focus may become one of the most important trends in distributed solar in 2026. As electricity costs rise and utility bills become a larger political issue, solar policy is increasingly framed not just as climate policy but also as consumer protection and household affordability policy.

Interconnection

The report highlights growing interest in flexible interconnection, which allows utilities to control when distributed generation systems export to the grid so that export volumes better align with available grid capacity.

Connecticut utilities filed a proposal for flexible interconnection, Massachusetts Governor Maura Healey signed an executive order directing utilities to implement it, and Xcel Energy and PPL Utilities are developing proposals as part of broader distributed generation plans. Maryland utilities are also compiling information on possible changes to the existing flexible interconnection implementation.

Flexible interconnection could become an increasingly important tool as distribution grids become more congested, said the report. Rather than forcing every project to wait for costly infrastructure upgrades, flexible export rules may allow more distributed energy resources to come online sooner, provided customers and developers can accept certain operational limitations.

Plug-in solar

The report also identifies a newer and more unexpected trend: plug-in solar. Lawmakers in ten states advanced legislation during the quarter to allow portable solar generation or plug-in solar devices. Many of the bills contain similar provisions, including exemptions from existing interconnection and net metering requirements, capacity limits of 1,200 W or less, compliance with the National Electrical Code, and certification by a nationally recognized testing laboratory. Maine was the only state to enact such a bill during the quarter, while Maryland’s bill awaited a gubernatorial decision, and Virginia’s governor returned legislation with recommendations.

Although plug-in solar remains a small segment of the market, the legislative activity reflects broader interest in expanding access to lower-cost, smaller-scale solar options. If adopted more widely, these policies could create new entry points for renters, multifamily residents, and households unable to install full rooftop systems.

Virginia also emerged as one of the most active states for distributed solar policy during the quarter. The General Assembly advanced several bills later signed by Governor Abigail Spanberger, addressing issues such as community solar program capacity, standby charge applicability, and smaller systems’ access to power purchase agreements. The governor also returned bills related to a DER Task Force and plug-in solar with recommendations.

The volume and variety of Virginia’s activity reflect the broader direction of the distributed solar market. Policy is becoming more layered, more technical, and more closely tied to questions of grid management and customer equity. The DSIRE report demonstrates the distributed solar market shift from growth-stage to becoming a core part of state energy policy, utility planning, and affordability strategy.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.