Today, Duke Energy released its Sustainability and Climate Reports, with the energy giant highlighting that the company met its 2020 owned renewable capacity goal and has expanded on it accordingly.

Duke Energy now owns, operates and contracts 8,000 MWs of wind, solar and biomass across the U.S. Broken down, Duke owns 2,500 MW of wind generation and 1,500 MW of solar, while purchasing 4,100 MW of generation, with the company reporting that 90% of its purchased power comes from solar facilities. This puts the company around 14% renewable now, capacity-wise, according to a company spokesperson.

By 2025, Duke is looking to double these marks, setting the goal to own or purchase 16,000 MW of renewable energy capacity (wind, solar and biomass).

Additionally, the company shares that it has lowered carbon emissions 39% below 2005 levels, which is 8% lower than last year’s mark of 31%. In doing so, the company is on track to achieve its goal of reducing CO2 emissions from electricity generation by at least 50% of 2005 levels by 2030.

Gas is here to stay

As quickly as Duke is projected to double its renewable capacity and reduce carbon emissions 50%, some industry experts have pointed out that a commitment to gas and nuclear, as well as capacity reservations for “zero-emitting load-following resources” (ZELFRs), technology which is not yet widely commercially available, is troubling.

As Ben Inskeep, principal energy policy analyst at EQ Research points out (thread), Duke maintains that natural gas units remain a necessary and economic resource to ensure reliability in the face of intermittent renewable generation, and to allow for widespread coal abandonment. Even under this accelerated abandonment, Duke doesn’t plan to close its last coal plant until 2045.

Duke Energy has released their 2020 Sustainability and Climate reports.

A couple highlights from the latter, which is called "Achieving a Net Zero Carbon Future." (Spoiler alert: it doesn't tell us how to realistically achieve a net zero carbon future.)https://t.co/Q2JCRXXp4s

— Ben Inskeep (@Ben_Inskeep) April 28, 2020

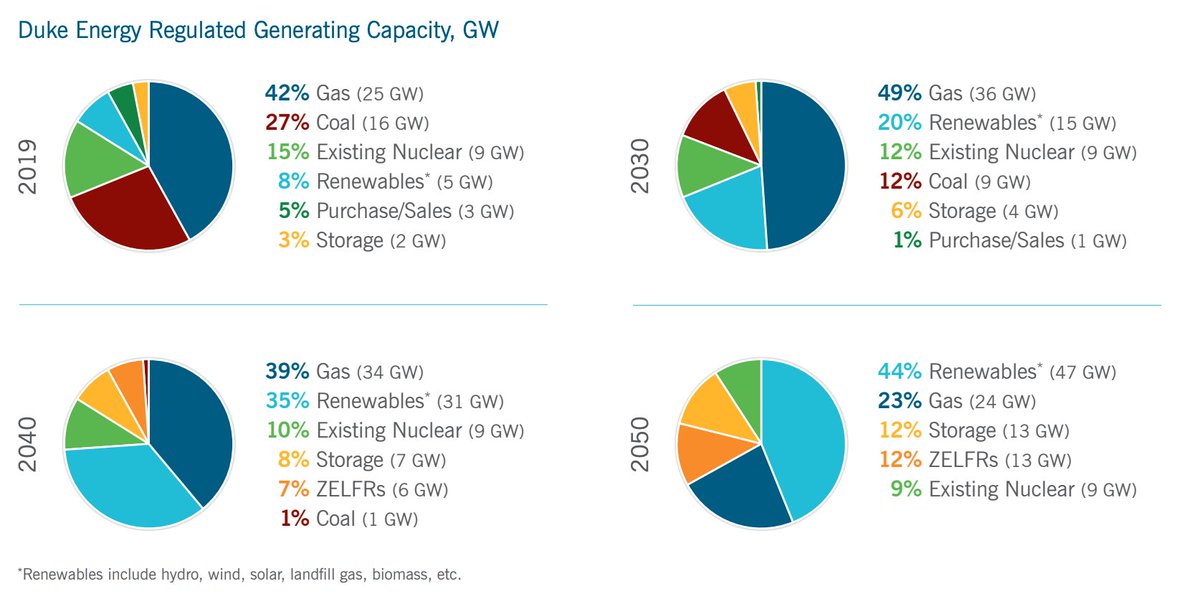

To quantify how each generation resource fits into the company’s future, Duke released graphs outlining the company’s intended energy mix by decade.

In the next decade, Duke plans to increase it’s natural gas capacity by nearly 50%, before ultimately curtailing it back down to modern-day levels by 2050. The company claims that by the end of that timeline, its gas fleet will shift from providing bulk energy supply, to more of a peaking and demand-balancing role.

While it’s accepted that some natural gas infrastructure is necessary to maintain a reliable and scalable energy supply, Inskeep sees it as Duke continuing to push a massive fossil gas expansion and “a big part of how they plan to increase shareholder profits over the next decade.”

Not stopping at the gas expansion, Inskeep also calls out the report’s ZELFR reliance: “While it [Duke] rejects relying on current techs as too expensive/hard, it says a big build-out of techs not commercially viable is reasonable.”

For the immediate counterpoint that storage can provide peak and demand-balancing benefits, Duke states that installation and operational challenges impede current commercially available storage options and claims that, in order to proceed with a no-gas future, the company would have to install over 15,000 MW of additional four-, six- and eight-hour energy storage by 2030. This would equate to 17 times more storage than the country has installed to date, ≈900 MW.

This seems to be where there is a disconnect between Duke and Duke’s critics. The above scenario is both drastic and unrealistic, but it’s also not the solution critics are calling for. The issue raised isn’t that Duke needs gas for peak demand and demand balancing, but rather that Duke plans to invest more than three times as much into gas and unproven ZELFRs than it does existing storage technologies, which can provide similar services to gas.

On the renewables side, Duke’s 2050 carbon-free plan outlines the addition of 40,000 MW of solar and wind, which will represent 40% of the summer 2050 nameplate capacity of Duke Energy’s system. As for who will own the 32,000 MW of new capacity that will come independent of Duke’s plan to own or purchase 16,000 MW of renewables by 2025, that is unclear.

https://twitter.com/Ben_Inskeep/status/1255164018744004615?s=20

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.