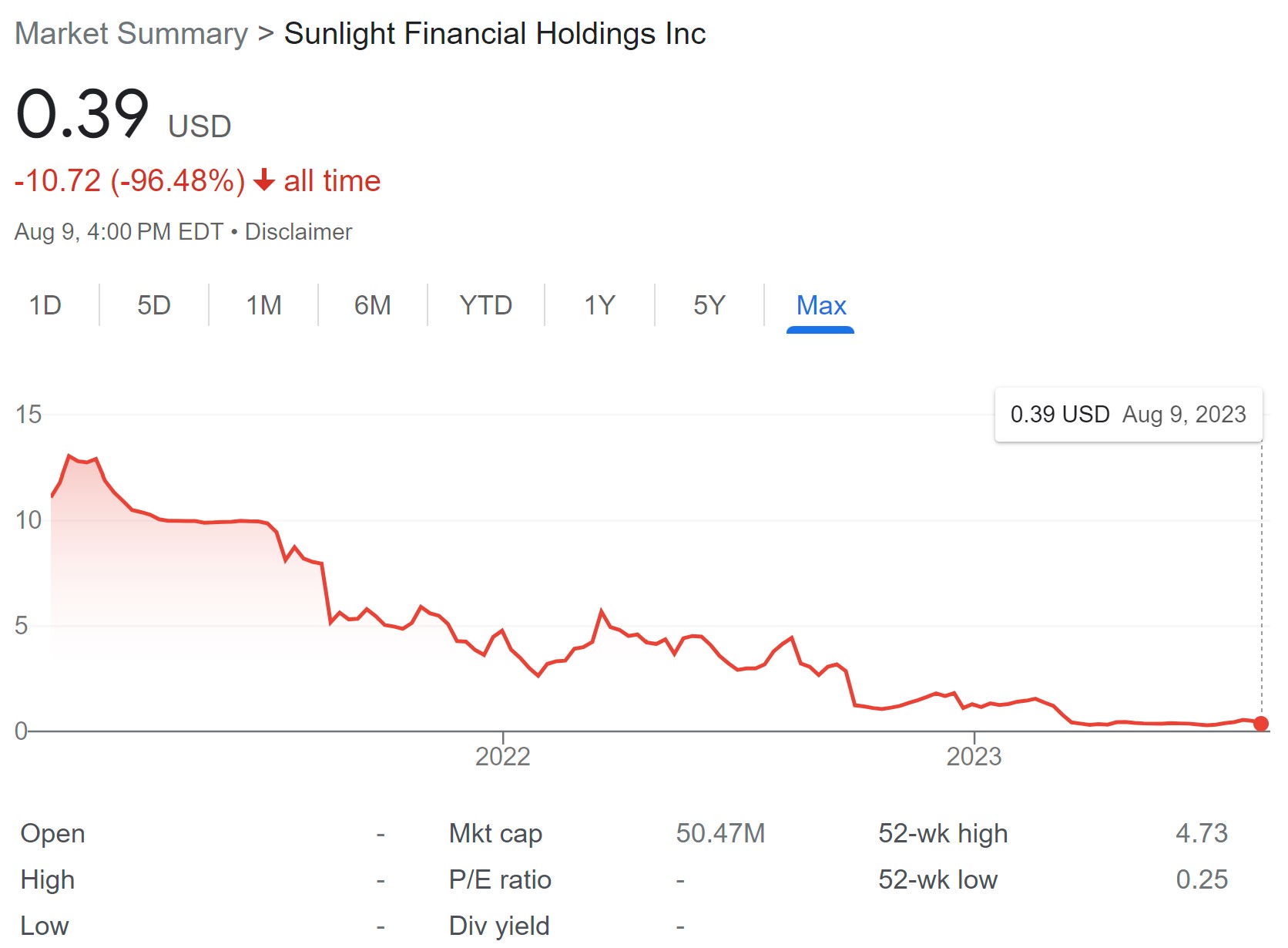

Sunlight Financial Holdings, known for its residential solar financing, has raised substantial doubts about its future operational viability. Their 10-Q financial documents, released on August 9, 2023, highlight a note about the company’s ability to continue as a “going concern” due to issues regarding raising cash for new loans.

The primary challenge for Sunlight arises in their “Indirect Loan” product. Starting in the second half of 2022, this product has been at the forefront of Sunlight’s offerings, and they’ve now acquired nearly $550 million worth of them. Yet, it has simultaneously placed the company in a precarious financial position. Sunlight has been holding these loans on its balance sheet, awaiting the right opportunity to sell them and thereby raise cash for the issuance of new loans – however – to date, the company has struggled to find buyers at a profitable price.

Recent Sunlight stock performance paints a grim picture: a 23% drop in the past five days and a staggering 96.4% plummet since its January 2021 launch. Roth MKM, a focused solar power analyst, once maintained a neutral stance toward Sunlight. However, post this disclosure, they’ve shifted Sunlight’s status to “Under Review”, citing unreliability in their data.

According to Sunlight’s 10-Q, the company faces difficulty in selling these Indirect loans:

- at or above previously forecasted pricing

- at or above Sunlight’s cost basis in these Loans

- within previously forecasted timeframes.

The Federal Reserve’s decision to raise interest rates is playing the leading role in this challenge. With interest rates climbing from 0% in March of 2022 to a substantial 5.25% today, the financial environment has turned volatile. Sunlight’s process means that loan approvals preceded specific cost amendments, meaning that Sunlight adjusted rates slower than the Federal Reserve escalated theirs.

To mitigate the ongoing rate increases, Sunlight took “pricing actions” on these loan products. The expectation was to offload these loans at a profit, but prevailing market conditions hindered such sales. As a result, Sunlight now has a backlog, with products valued (as per their former evaluations) at $550 million on their balance sheets. Although their financial partners have waived a cap surpassing $500 million, Sunlight clarifies that this is a short-term concession.

The 10-Q further sheds light on Sunlight’s Q2 performance. Key metrics, such as revenues, net income, and adjusted earnings before interest, taxes, depreciation and amortization (EBITDA), are all down significantly.

In 2022, the residential sector was the bright spot in the U.S. solar market, boasting a 40% increase in installed solar capacity. This growth came even as the nation’s overall solar installations dwindled due to challenges from solar module import tariffs. Pioneering market leaders like Sunlight contributed to this rise, leveraging aggressive financing strategies to offer affordable loans to homeowners eager to invest in solar power.

For example, SolarEdge witnessed record revenue growth in 2022, buoyed largely by its U.S. sales volume. Yet, despite posting record revenue and experiencing global growth, their most recent quarterly report indicated softness in the U.S. market, which subsequently impacted their stock price.

Industry analysts, such as Ohm Analytics, have noted a shift: residential solar contractors are transitioning away from challenging solar finance states like Texas and Florida. Instead, they’re gravitating toward states offering greater incentives or those with elevated electricity prices to augment sales. This shift follows a conundrum for companies that relied heavily on loan financing structures, such as upfront payments upon deal closure, from entities like Sunlight Financial. Without a steady influx of capital, these companies are grappling with operational challenges.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.