The United States added 20.2 GW of new solar capacity in 2022, down 16% decrease 2021. According to the U.S. Solar Market Insight 2022 Year in Review by the Solar Energy Industries Association (SEIA) and analyst firm, Wood Mackenzie, this was due in large part to an investigation into new anti-circumvention tariffs by the U.S. Department of Commerce, as well as equipment detainments by Customs and Border Protection under the Uyghur Forced Labor Prevention Act (UFLPA).

The decrease is an unfortunate result of these policies, however, it is much less than previously anticipated as SEIA had previously lowered its solar installation forecasts for 2022 and 2023 by 46%, and SEIA had predicted that the case will result in a drop of 24 GW of planned solar capacity over the next two years, which seemed drastic as it was more solar than the industry had installed in all of 2021.

While Q4 2022 was the best quarter of 2022 for the utility-scale segment, installing 4.3 GW, this was still the segment’s lowest fourth quarter since 2018. The report indicates that utility-scale installations fell by 31% year-over-year to 11.8 GW, the sector’s lowest total since before the COVID-19 pandemic. Commercial and community solar installations also fell by 6% and 16%, respectively. In addition to the policy constraints, interconnection backlogs are another factor limiting deployment in each market segment.

“Companies are aggressively shifting their supply chains, helping to ensure that solar installed in the U.S. is ethically sourced and has no connection to forced labor,” said SEIA president and CEO Abigail Ross Hopper. “While the solar and storage industry acts swiftly on supply chains and building a stronger domestic manufacturing base, ongoing threats of steep tariffs are holding back the potential of the historic Inflation Reduction Act.”

Residential was the bright spot in the U.S. solar market last year. With half the residential market installing domestically sourced solar modules, it is not as affected by trade issues. The residential sector experienced a 40% increase in installed solar capacity in 2022, and now 6% of all homes in the United States have solar.

More good news is that solar accounted for 50% of all new electricity-generating capacity additions in 2022, which is the fourth consecutive year that solar topped new additions. Looking ahead, the United States is expected to add over 570 GW of new solar capacity in the next decade, bringing installed solar capacity from 141 GW today to over 700 GW in 2033.

Energy storage

In 2022, the report estimates that 783 MW of new residential, commercial and community solar capacity deployed was paired with energy storage systems, a new record. By 2027, 33% of new residential solar capacity and 20% of new commercial and community solar capacity will be paired with storage.

Top states

California, Texas, and Florida were the top three states for new solar capacity additions for the third consecutive year, with California assuming the top position from Texas after the Lone Star State led the nation in 2021.

Looking ahead

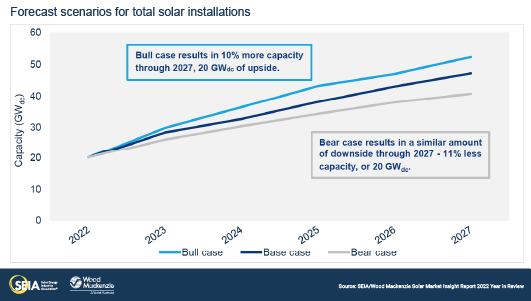

With the current supply chain constraints and myriad near-term uncertainties, for the first time Wood Mackenzie created two forecast scenarios. The bull case estimates 10% more capacity through 2027, assuming more availability of non-tariffed supply as well as a more optimistic view on how much, and how quickly, domestic manufacturing capacity comes online and supplies the US market. The bear case anticipates 11% less capacity through 2027, assuming a less favorable supply environment. The report notes that the alternative cases take into account the various outcomes related to the guidance from the U.S. Department of Treasury on qualifying for tax credits and associated adders of the Inflation Reduction Act.

“While 2022 was a tough year for the solar industry, we do expect some of the supply chain issues to ease, propelling 2023 growth to 41%,” said Michelle Davis, principal analyst at Wood Mackenzie and lead author of the report. “With major uncertainties ahead of the industry, our high- and low-case scenarios can help the industry benchmark potential outcomes. In each scenario, there is roughly 20 GW of upside or downside risk over the next five years — the same amount of capacity installed last year.”

Anticipating supply chain relief this year, the report authors expect a “robust return to growth in 2023,” forecasting that the United States is expected to add over 570 GW of new solar capacity in the next decade, bringing installed solar capacity from 141 GW today to over 700 GW in 2033. After another year of trade policy turmoil, the U.S. solar industry is hoping for supply chain relief in 2023, expecting shipments to accelerate in the second half of the year. Assuming policy stays a steady course, the report authors contend that we will see 2023 installations grow 41% over 2022 to 28.4 GW (DC).

Looking a decade out, the report authors anticipate that the solar industry will experience five-fold growth. The Base case forecasts cumulative solar installations by 2033 at over 700 GW (DC), compared to 141 GW (DC) installed as of year-end 2022, a five-fold growth over where we are today.

Download the full report here.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.