Utility-scale solar development was hit with a tough year, marred by tariff static that considerably crimped the pace of large-scale grid deployments. Wood Mackenzie forecast a 40% decline in utility-solar project deployments, but that hasn’t stopped developers from going bigger and bolder, including with batteries attached.

With the broader solar market forecast to see a 23% decrease in installation rates, utility solar is expected to wrap up at about 10.3 GWdc installed capacity, as the industry continues to weather supply chain challenges and trade disruptions from the Biden Administration’s PV module tariff imposition and flexing the Inflation Reduction Act to spur American-made modules.

Macro static aside, state system operators and corporate offtake customers continue to drive the theme of bigger is better, and yes, batteries also better, with PV Intel data showing that close to 50% of near-term utility solar projects are seeing energy storage systems enter the equation for grid resiliency measures.

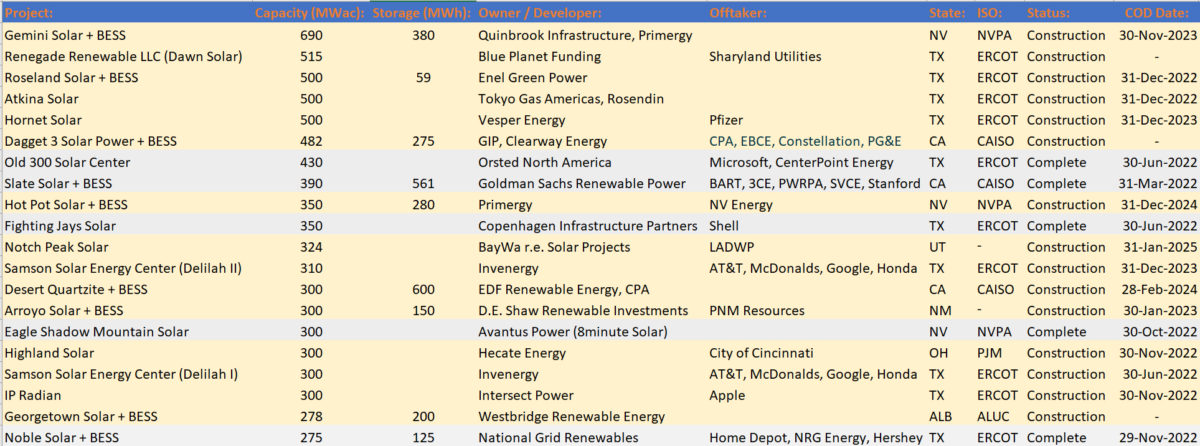

PV Intel examined projects with commercial operations falling within the next three years, encompassing utility projects aimed at being wrapped up in the 2023 or 2024 timeframe since just entering the discussion within the last year. While 2020-21 saw projects top out at 250 MW and 300 MW, the 2022 class of projects to enter the interconnection queue is roughly double the class of prior years, with many projects clocking in at 400 MW to 690 MW.

Among the 20 largest PV Intel projects, Texas, California and Nevada represented 15 of the largest projects among the latest slate of project developments, while three additional southwest projects popped up, one Ohio project and an Alberta project.

Image: PV Intel, EIA monthly dataset

What is more surprising is that almost 50% of the new large-scale projects pulled by PV Intel are being developed with an average of four-hours of grid-scale energy storage at co-located sites. Nine out of the 20 largest projects are being deployed with a battery storage system to keep electrons flowing into the night. That compares to about one-third of the previous slate of projects looked at through mid-2022 to utilize storage systems.

“In all cases, ambitious clean energy goals from both utilities and corporates are driving higher renewable penetration,” said Sylvia Leyva Martinez, a senior analyst in Wood Mackenzie’s utility solar group. “In the case of storage, price volatility and multiple revenue stream monetization is going to help increase the share of hybrids in the system.”

Leyva Martinez told pv magazine usa that corporate customers have driven up demand for large-scale utility solar project developments in Texas, while solar deployment in other states like California and Florida is driven by community choice aggregation or utility–specific procurement.

With the Inflation Reduction Act’s inclusion of a storage investment tax credit, Leyva Martinez said to expect to see the percentage of storage deployments accompanying grid solar projects to increase in 2023 and beyond.

Wood Mackenzie expects supply chain disruptions to dissipate toward the end of Q2 23, though Leyva Martinez said numerous domestic developers such as Intersect Power, Leeward Renewable Energy, and Primergy are sourcing solar modules from First Solar and other American-made suppliers to reduce trade policy risk affecting imported modules.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

Utilities are making it clear; they do not want rooftop solar competing with the large industrial solar farms. The CPUC used cost shifting as the main argument to unanimously push through NEM 3.0, yet the poor get nothing out of NEM 3.0 but more rate increases in California. Solar Farms and Utilites are “Big Business” and only work if there are enough customers to buy and use their products (energy). Rooftop solar eliminated customers and did nothing for the bottom line. With a purchase price of 3 cents per kilo watt hour from commercial solar farms, that make money at those prices, the utilities charging 36 cents per kilo wat hour to their customer base, it is no wonder why the NEM 2.0 customers are a thorn in the side of California utilities. The only way to break away from the exorbitant utility pricing will be to become a micro-grid and not connect the rooftop solar to the utility and use or store the sunlight created electricity on the spot. Once low-cost batteries are available, to rooftop solar adopters, the sooner they can cut the cord to the high utility prices.

I noticed that your reference to tariffs imposed on solar panels was attributed to the Biden administration:

With the broader solar market forecast to see a 23% decrease in installation rates, utility solar is expected to wrap up at about 10.3 GWdc installed capacity, as the industry continues to weather supply chain challenges and trade disruptions from the Biden Administration’s PV module tariff imposition and flexing the Inflation Reduction Act to spur American-made modules.

I guess you have forgotten that these tariffs were imposed by the Trump administration and reduced, though not eliminated, by the Biden administration.

here is a source you may want to review:

Biden admin eases Trump-era solar tariffs but doesn’t end them

https://www.reuters.com/business/energy/biden-extends-modifies-trump-era-solar-tariffs-says-official-2022-02-04/