by Gregor Macdonald

Northern Indiana Public Service Company (NIPSCO) watches over one of the larger portfolios of coal-fired power generation in the Midwest. A provider of residential electricity, NIPSCO serves a customer base dominated by industrial firms. Just five companies – British Petroleum in particular, with its enormous refinery in Whiting, Indiana, along with Praxair and three large steelmakers – make up 40% of its energy demand.

But in 2018, when NIPSCO looked ahead to the next decade, it saw a 2.09 GW portfolio of coal-fired generation that would continue to provide sufficient power, no doubt, but one that would also incur increasing economic losses. After conducting an extensive study, in which six feasible energy mixes were considered, NIPSCO chose a plan that would offer the best prices to customers: shutting 78% of its coal capacity by 2023 – the final 22% by 2028 – and replacing this capacity with a combination of wind, solar and storage. The portfolio transformation will initially be led by adding wind power through 2022, with solar and solar+storage dominating new generation thereafter.

The solar+storage component of NIPSCO’s plan is notable, as U.S. projects that pair the two are becoming increasingly common. “I’ve recently come to the conclusion that in the future we’re not going to build much solar without storage,” says Cody Hill, a veteran storage engineer and developer based in Oakland, California. “All the easy-to-build solar – that supplies power midday – that opportunity is eventually going to be eaten up. So you’re going to have to start time-shifting at significant scale to keep growing the solar industry.”

Until recently, battery energy storage has largely served markets at the margin, offering short bursts of frequency regulation or light pricing arbitrage. Tesla’s early megaproject in Australia offered an algorithmically driven battery bank that could jump into the larger grid for small timeframes to better match spikes in load, for example. In other domains, EV charging companies have started to time-shift small tranches of load, using EV fleets as demand-side management – opening the door to their use as a collective battery. Early storage projects have mostly been small, too: battery capacity to compliment emerging municipal fleets of electric buses, or local experiments with microgrids.

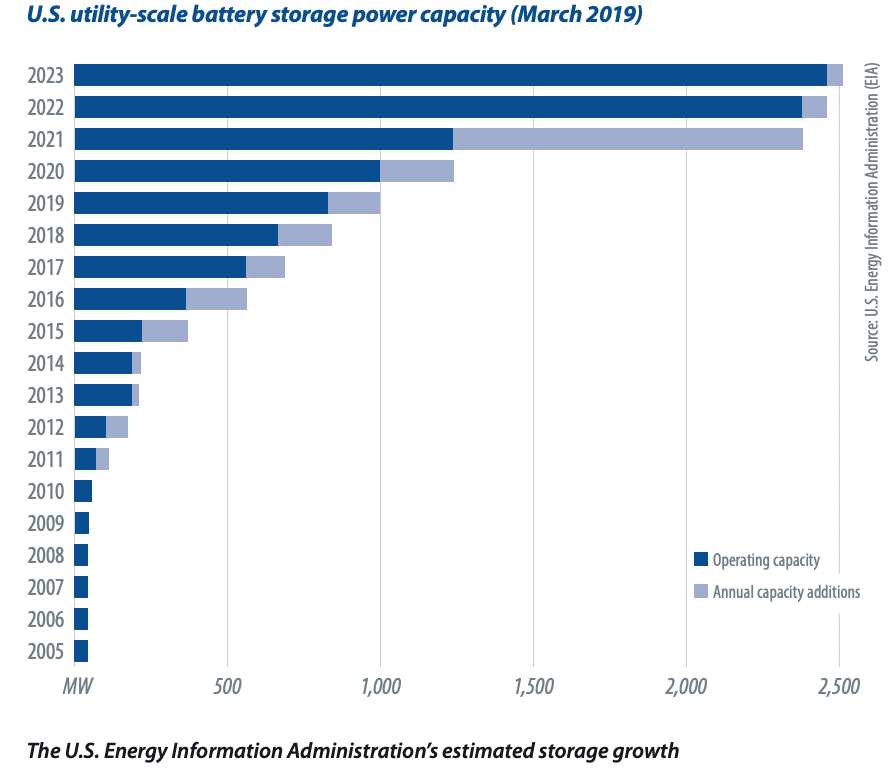

According to the U.S. Energy Information Administration (EIA), however, utility-scale storage is about to leap forward in the U.S., following a long period of slow growth. More than doubling from this year’s 1 GW of capacity to nearly 2.5 GW by 2021, the jump is spearheaded by two megaprojects – the 409 MW Manatee unit in Florida and the 316 MW Ravenswood unit, to be built out in stages, in Queens, New York. The growth is being driven not just by falling storage costs, but also continuous price drops for clean generation. Forecasters largely missed this emerging dynamic. Although storage’s progress down the cost curve has historically been slower, whole system costs have continued to fall as wind and solar became the cheapest form of generation.

But storage also has achieved rapid cost declines. The levelized cost of electricity (LCOE) of lithium-ion dropped by 35% to $187/MWh from just the first half of 2018 into 2019, according to a report released earlier this year by BloombergNEF. Gap moves of that magnitude now open up storage for a new role, increasingly marshaled as a form of generation – at least during times of peak load. Unsurprisingly, this will place further pressure on incumbents. “The folks that are struggling are the baseload generators, those that can’t shut down and start back up very fast,” says Hill. “They have to generate even when they are losing money for every megawatt-hour they are putting onto the grid. They are really struggling with renewables, and that’s why coal is struggling, and nuclear is struggling.”

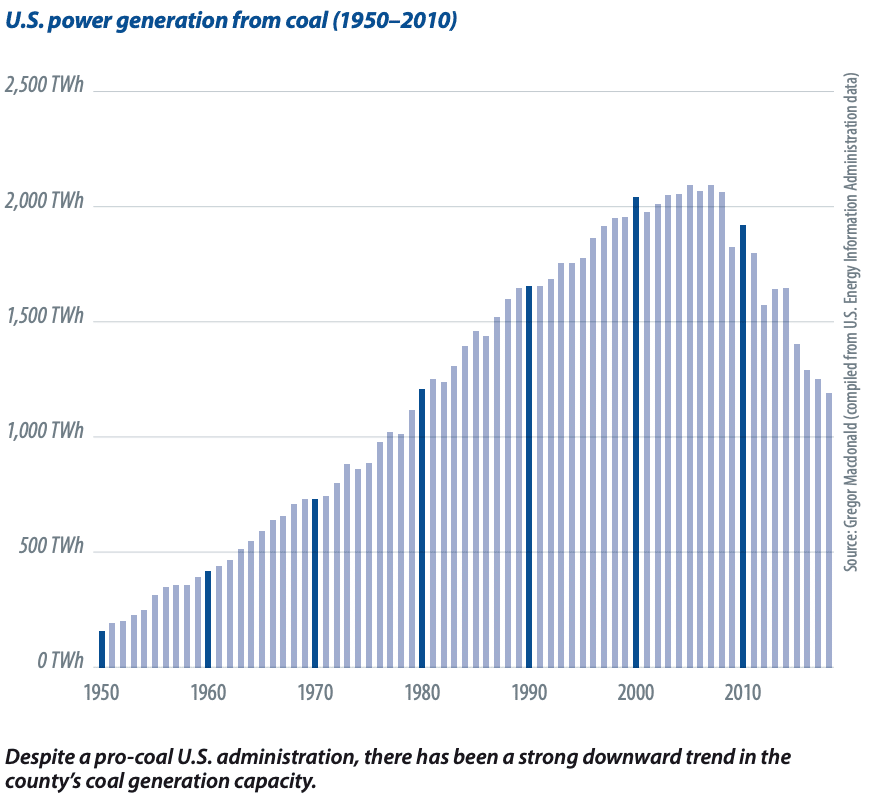

The NIPSCO resource plan decision shocked the U.S. power industry. Steelmaking and coal have long been intertwined, and that’s especially true in Indiana, where the minimill revolution – a technique to use electricity to melt scrap into hot rolled steel – owes its beginnings to a plant Nucor Corp. established in Crawfordsville in the early 1990s. Minimills can exert a large pull for power grids when their electricity demand spikes upward. But this decade has seen a far more extended wave of coal retirements than expected, with 55 GW of capacity closed from 2007 through 2017. Most assumed this would eventually slow under a coal-friendly administration in Washington. Alas, not so. Last year saw more than 10 GW retired, the second highest year since 2015, when over 14 GW were closed. With coal’s contribution to U.S. electricity generation having fallen from 50% to nearly 25%, there’s a reasonable prospect that coal generation in the U.S. will, as it has done in Britain, head toward zero.

NIPSCO is not the only utility sending out a warning signal. California’s Pacific Gas and Electric (PG&E) and Arizona Public Services (APS) both recently announced plans to deploy storage, either obviating the need to build new generation, or in the case of PG&E, to replace existing generation. Taken together, storage is now pulling into peer position with wind and solar technology. And in time, storage will likely be regarded as standard when deploying new capacity of any kind. While assessing the economics of storage can be more complicated due to its broad menu of revenue-generating services (the ROI can vary depending on how it’s utilized by the owner), utilities now recognize that building storage creates an asset of real versatility, no matter the mix of their generation portfolio.

“Solar, once it’s built, looks like a fixed income type of asset. It looks like a bond,” says Hill. “Storage however is not like a bond, but really more like a basket of options. The option to sell power at different times. What’s interesting is that peaking power also looks like a basket of options – albeit with a different mechanical structure around it. But financially speaking, storage looks more akin to the development of peaking generation.”

In the case of APS, Arizona was in a perfect position to purchase surplus power when vast solar capacity lit up midday across California’s deserts, exceeding load. More telling is that APS initially thought of adding a much smaller amount of storage but, seeing the attractiveness of the bids, added more. By the mid 2020s, APS plans to have built 850 MW of storage. One conclusion that might be drawn from the APS strategy is that new generation growth, especially from wind and solar, is becoming common and routine. The strategy to build storage, therefore, is obviously for the purpose of arbitrage – buying supply when power is cheap, and selling it back into the market when it’s more valuable. The difference here is the scale: As with similar projects, the battery storage design is generally aligning to four hours of output. APS will be able to use this storage capacity to provide power, likely during the high demand window between 4 p.m. and 8 p.m.

Back across the state line in California, PG&E also announced last year its own plan to replace 670 MW from three retiring natural gas plants with 567 MW of total storage. Storage economics benefit from scale of course, and the size of each battery unit is important. APS had already retrofitted an existing solar facility with 50 MW and plans a 100 MW unit. Now comes PG&E with plans for a 300 MW unit, and the next decade will bring the 400 MW unit from Florida Power and Light’s Manatee project. This is how the learning rate works in practice: Size expansion improves unit economics for the owners, but also drives manufacturing costs downwards as output rises. Eventually, all future buyers of storage will benefit from the low prices created by early demand.

the United States is not entirely tied to price. Arcane financing structures – ones that create separate income streams for generators even on loss-making capacity – and also varying regulatory environments, can mean that legacy generation can carry onward. The recent bailout of existing nuclear and coal capacity in Ohio, for example, offers an instructive contrast to NIPSCO’s plan, as the future losses from Ohio Valley Electric’s coal plants are being subsidized. Leah Stokes, a professor in the Department of Environmental Studies at UC Santa Barbara, observes that Ohio is looking to cover losses in the same way that NIPSCO is looking to avoid them. “If you’re not building the future, you’re continuing to invest in old technology. And, that will have a cost at some point when you use billions to invest in coal plants, instead of building new wind, solar and storage that would create longer life value.” The plan unsurprisingly will add new fees to ratepayers’ bills and raises the specter that Ohio residents will face a double loss: having to pay extra in the present for old technology, while also missing out on the opportunity to own new technology. “Eventually, there will be some federal climate legislation and Ohio is going to be way behind the mark, and its citizens will have to pay for that. It’s tragic,” says Stokes.

Clean generation paired with storage is moving fast. At the end of July, NextEra announced it was building a 700 MW triple hybrid project for the Western Farmers Electric Cooperative in Oklahoma, composed of 250 MW of wind and solar generation each, plus 200 MW of storage. While storage is not yet in a position to act as long-duration supply, there are indeed systemic effects likely to appear. Hill points out that historically, pumpedhydro built in the middle part of the 20th century offered a way for original coal and nuclear generators in the West to improve their economics on a plant-by-plant basis. And he speculates that lithium-ion battery storage is about to echo that history, as pairing becomes more common.

“Right now, in terms of [larger battery] duration, we are in the realm of single digit hours. Not all day, and not many days,” says Hill. But even that short duration is enough to vastly improve the value of new wind and solar capacity.

With wind and solar quickly becoming cheap commodities, built easily across various regions, their collective presence is disrupting power markets and triggering a new set of decisions by utilities. As storage starts to become as ubiquitous, it too will start to influence how power grids evolve. Battery units of 300 MW or even 400 MW are certainly large, standalone units. But what will happen when 10 such units are located in a single region? A network effect now seems inevitable for storage. Rather than replacing generation with single battery projects, collective capacity will act like virtual generation as regional storage resources move from the MW level to the GW level. If storage is indeed a basket of options, that makes for a very large basket.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

When construction of fueled power generation costs so much up front, that it takes 30 or more years to amortize the asset, how can a utility continue to DO the same thing and expect to survive? REALLY? Commodity fuels that can be affected by demands, political unrest, labor strikes, weather and just plain inefficiency in the way things are done. Energy storage, save as much cheap non-fueled energy generation you can get and sell the electricity later on at a “better” price. $2 billion dollars for a coal fired generation plant that wastes about 50% of the energy put into the system to create the electrical output or $2 billion dollars on energy storage that can be locally and regionally constructed that saves energy for now and controls the flow of energy later, without having to run a plant in “spinning reserve” 24/7.

So, does Las Vegas have a statistics board for energy storage and who dives into the fray to create the multi-day energy storage system ? Right now runners like NextEra are constructing large scale solar PV generation in States like Florida right now. Redox flow battery manufacturers are beginning to come to market with large scale product designs in mind. In the U.S. no large scale systems have been adopted to date. Wind and Solar PV farms are usually hundreds to thousands of acres in size, within that project there is plenty of area available for a couple of hundred acres of GW plus redox energy storage available. somewhere, sometime, one of these utilities will have to make the jump to GW of storage. My best guess is Texas and ERCOT.