Robb Wilson of sPower – which owns 1,340 MW solar photovoltaic projects, 1,240 MW of which the in-house operations and maintenance (O&M) team “sPower Services” manages – presented at PV Operations Dallas 2019. His presentation covered a history of O&M budgets, a high level summary of components of these budgets, an example budget, and some insight on how ‘soft costs’ are really figured out.

One clear message in Wilson’s talk was that the slow build of institutional knowledge, not module efficiency as he was specifically asked, has had the most significant effect on the decline in O&M costs.

Wilson noted that some of the large solar project sales in his early days at FirstSolar included “all in” O&M budgets priced from $10-18/kWdc/year. All in is being defined as taking on all O&M labor, as well hardware warranty/replacement risk. These all-in budgets were structured this way by groups like FirstSolar because they made the modules, developed the project, worked with inverter manufacturers, and built the project – so they had confidence in taking on the risk. They also worked this way because the big money buying the projects didn’t have enough history to base their purchases on, and needed that type of contract to balance risk.

As the industry has evolved, with O&M teams now generally separate from those who develop and build projects, the distribution of risks changed from the prior arrangement. This meant that risk shifted back to the project owners, which pushed pricing for O&M contracts down. During this progression, solar power operations and maintenance pricing fell from $10-18/kWdc/year to $4-9.50/kWdc/year – more than 50%.

Now, there are fixed and unplanned portions of the contract that are budgeted. Wilson suggested values ranging from $3-6/kWdc/year for the fixed labor portion, and the unplanned costs (which Wilson noted are estimated based on relations and experience versus data) between $1-3.50/kWdc/year.

As well, due to experience and new technologies the techniques and risks of O&M have evolved. For instance, Wilson said at some point his team thermally scanned hardware and visited sites six times a year to gain knowledge on performance – but slowly found that those scans didn’t generate value equivalent to their costs, and – slowly, but surely – remote monitoring has now mostly replaced site visits.

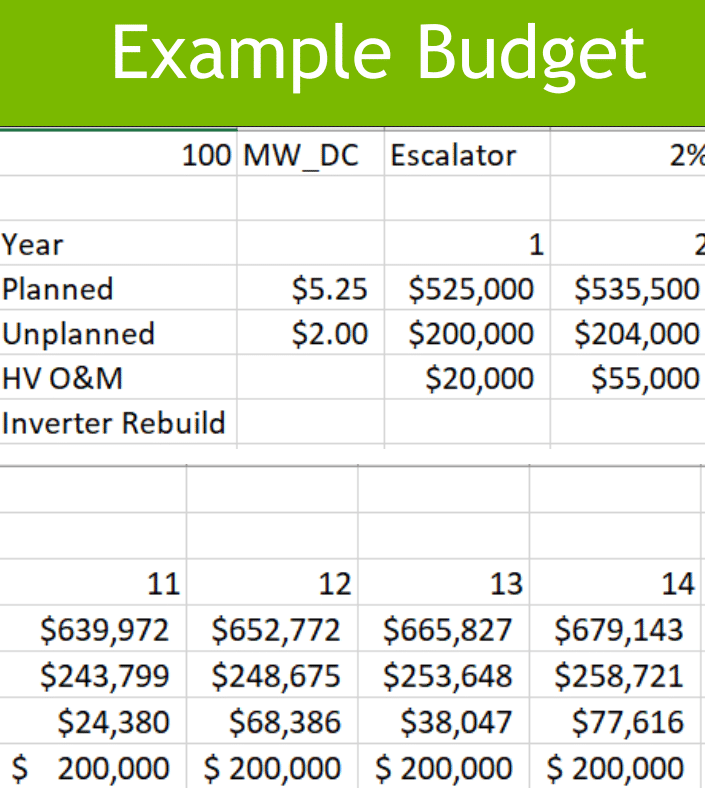

The above example budget crosscut came from Wilson’s presentation. Among his observations is that there ought be an escalator as much of O&M is based on human labor costs. This contradicts the idea that many have of no escalator based on the declining costs of hardware.

When asked about budgeting for substation and high voltage O&M – Wilson said their schedule does include work on all aspects of the hardware short of the power lines. As well, the budget is a bit more complex than the single line shown above – for instance step up transformers have a multiple year O&M schedule that includes fuses one year, maybe a replacement of gaskets and oiling the next year, followed by a possible replacement at a different time.

Going back to the institutional knowledge line of thought, throughout Wilson’s presentation he referenced that his teams were continually learning, and this learning was still heavily influence his pricing, his actions and his judgments. For instance, he noted that if your warranty information in your contracts said “to manufacturers specifications”, he’d think that you don’t actually know the O&M requirements. By delving into the details on these topics he is able to build discipline in pricing and management, as well as to put leverage on developers for pricing and procurement since not all manufacturers have the same O&M requirements.

When questioned by this pv magazine USA author what it’s like, as sPower does, getting investment from conservative partners like pension funds, Wilson noted:

First off, we’re bonded. As well, there is a part of the sales process that is a literal showing of the O&M process – you bring them out to the guys working on the plants. However, it ends with them looking at the numbers – with us saying, ‘here’s our historicals’ – and that’s when we gain confidence with those types of investors.

In our continuing coverage of the meat of actually running solar power systems (versus the beautiful headlines of the latest, greatest, cheapest and the future), we’re hoping to fill holes in our knowledge on fire risks, wind defenses, and the evolving of operations and maintenance practices. This knowledge is new knowledge as our industry is new; of the ~75 GWdc installed in the USA – around 50% has been installed in the past three years, and this volume might just double before the effects of the investment tax credit wane.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

Like the picture of the truck with derrick and spray heads to hose down the heliostats or solar PV panels for the next days generation period. It’s becoming a SCADA kind of operation. One where rich data points with feedback from operations giving temperatures, pressures, solar insolation, monitoring energy storage systems for heat, fire, intrusion, air conditioning failures, fire suppression systems activation, voltages, currents, individual energy storage packs health and function. Instead of two hundred guys to operate a plant, you have twenty roving employees taking care of operations and maintenance. Now what is the O&M costs there?