Two and a half years ago, Vivint Solar was at the top of its game. The company had grown rapidly with the rise of the third-party solar model, and was on the cusp of being acquired by SunEdison. But as SunEdison’s investors began to revolt against the company’s buying spree and debt burden and the company’s stock began to plummet, Vivint Solar found itself caught up in one of the greatest crashes that the industry has seen to date.

As of Vivint Solar’s Q4 2017 results the company has regained its footing and most critically its access to financing. However under new leadership it is a smaller but more profitable company, and one that is reacting to larger changes in the residential solar market.

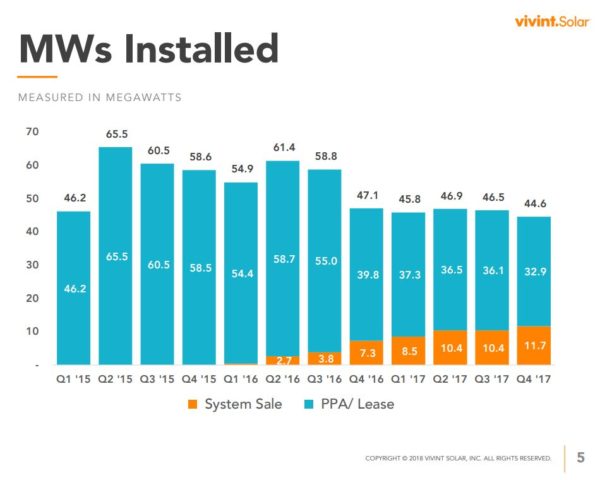

Vivint installed a mere 44.6 MW of solar during Q4 2017, its lowest level in at least three years, as the company continues its transformation. Like Tesla/SolarCity, Vivint is moving away from the third-party solar model, and for the first time more than ¼ of its sales by volume were for cash, not under a leasing arrangement.

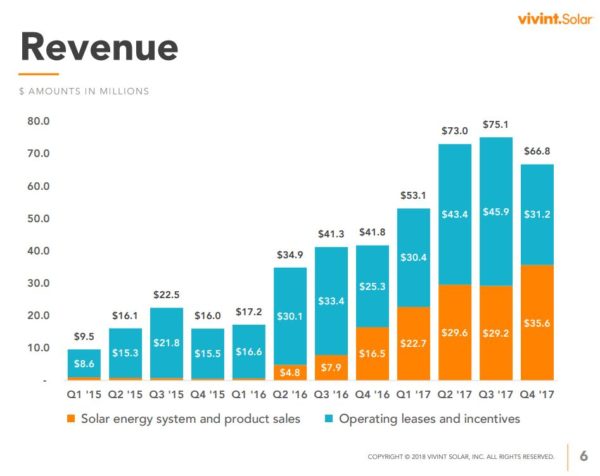

This also means that Vivint’s revenue and profitability are improving. For the first time direct sales brought in more than half the company’s quarterly income. Overall revenues increased to $66.8 million, 60% more than a year ago.

And while it is normal for a company that gets most of its sales volume from leases to show a loss, Vivint has brought its operating loss to $26.7 million, as opposed to $38.1 million a year ago. Along with this Vivint has kept its install price below $3.00 per watt during all of 2017, despite the jump in module prices in anticipation of Section 201 import tariffs.

In terms of profitability, last December’s federal tax reform was also good to Vivint Solar. The company was able to revalue deferred tax liabilities, which brought in a $188 million non-cash gain. This means that despite its negative operating margin Vivint turned a $183 million profit during the quarter.

Vivint’s transformation is not limited to moving away from the third-party model. Vivint is currently undergoing two big shifts: moving to dynamic pricing for its sales teams, as well as beginning to work with a dealer network as opposed to keeping its installations in-house.

Vivint began deploying a dynamic pricing model on a trial basis during Q4, which it says is essential to competing in sunnier markets as well as retaining a “world class” direct sales organization. This will inevitably bring up the company’s sales costs, but Vivint says that it is well worth it, as it enables a “shift to capturing most valuable systems”. This is particularly true in California, the nation’s largest market, where the pull-back of Tesla/SolarCity has left an opening for other companies.

Along with this Vivint plans to begin working with third-party dealer networks, which it says will also allow it to compete better in an environment where the big third party solar companies are no longer growing. “Most of the growth in the industry comes from dealers,” stated CEO David Bywater on the company’s results call. “It’s all upside for me.”

With these changes and its improved profitability, Vivint says that it expects to go back to a growth path. After a slow Q1, where Vivint expects installs to fall again to only 40 MW “due to transitional activities”, Vivint expects to grow again in Q2 and over the full year 2018.

Underlying this growth, it is important that the imposition of the BEAT tax does not appear to have shut off tax equity financing for Vivint. The company was running out of tax equity funds at the end of 2017, but since that time signed a new tax equity partnership for $75 million, which will support 52 MW of installs, as well as $401 million in non-binding tax equity term sheets for five partnerships which if signed will enable it to install roughly 265 MW.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

The numbers are dropping because consumers are becoming aware of the criminals they are, and the thousands of victims they have racked up. My home has over $367,000 in damages, others have non working panels still after a year, some have lost their homes, and Vivint is collecting tax credits on homes with no solar panels. They are being exposed for the crooks they are. Google Vivint Victims, or vivint complaints and have your eyes opened about this company.

Well, those are interesting allegations. And while it is true that they have 565 complaints registered through the Better Business Bureau over the last three years, they have resolved 138 of them to the customers’ satisfaction, and maintain an A+ rating.

https://www.bbb.org/utah/business-reviews/solar-energy-contractors/vivint-solar-in-provo-ut-22302389