Of all the firms commenting on the Section 201 case, GTM Research is in a unique position to provide analysis. The company’s report series, published in collaboration with Solar Energy Industries Association (SEIA), has been the only reliable source of quarterly solar installation data for nearly a decade, and GTM Research exhaustively examines each segment the U.S. downstream solar market.

Late yesterday the company released more analysis on their expectations of the market effects of solar tariffs. And while the standard narrative has been that utility-scale solar will be the most affected, this analysis suggests that both residential and other distributed solar installations will also see meaningful market losses versus their baselines.

This ultimately has to do with the confluence of many factors in addition to the tariff levels, including policy changes and the sensitivity of the downstream solar market at the margins.

Residential solar to fall 9.9% versus base case

It is somewhat counterintuitive to think that residential solar will see significant effects, given that the cost of PV modules represents the smallest portion of overall system costs of any market segment. However, GTM Research expects the residential market to decline 9.9% over the next four years versus its base case.

The firm argues that the Section 201 tariffs will push back those markets where solar prices had recently achieved parity with electricity rates, mentioning Pennsylvania, Florida and Texas as the states where it expects the biggest declines on a percentage basis. And while the portion will be smaller in California and the Northeast, the company expects the biggest loss of volume installed in these larger markets.

It is important to note that in addition to the Section 201 tariffs, the U.S. solar market faces a number of other headwinds. The firm estimates that this market segment already fell 13% in 2017 due to “growing pains of national installers in major markets, in conjunction with segment-wide rising costs of customer acquisition”.

Non-residential to decline 10.7%

GTM Research lumps commercial, industrial, non-profit, government and even community solar installations into its “non-residential” segment. As this segment typically benefits more from economies of scale that bring down balance of systems and “soft” costs like installation on a per-watt basis, it is more sensitive to the increase in the price of modules than residential solar, but less than utility-scale solar.

The firm argues that this the combination of expiration of incentive programs and rate design changes at the state level will cause market declines in this segment. In terms of specific changes, GTM Research cites the shift in time-of-use periods in California, the transition to the SMART program in Massachusetts, and the oversupply in New Jersey.

The company also argues that community solar is sensitive to price increases because of the high costs of customer acquisition. Overall, GTM Research expects an 10.7% decline in the non-residential market versus its base case through 2022.

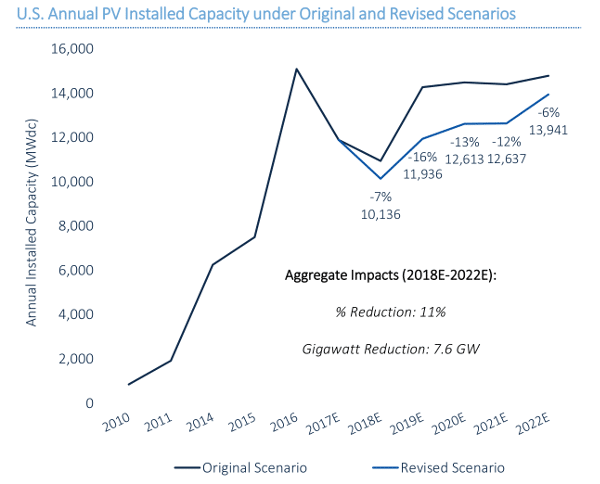

Biggest impacts in 2019

Overall, the utility-scale sector is still expected to see the biggest impacts, as modules make up the largest portion of system costs, which GTM Research puts at 40% to 45%. Since it is the largest market segment, this will also mean the biggest impact in terms of volume of solar that would otherwise be deployed.

In all three market segments, the effects of the Section 201 tariffs are expected to be felt most keenly in 2019, not 2018. GTM Research predicts only a 7% decline in installations versus its base case this year, but a 16% fall next year.

It cannot be overstated that these predictions are relative to the company’s previous forecasts. Due to the “hangover” from a construction boom in advance of the expected drop-down of the U.S. Investment Tax Credit (ITC), 2017 and 2018 installation levels were always expected to be lower than 2016. So what a 16% fall in 2018 really means is more muted recovery as the solar industry returns to a path of long-term growth.

When looking at these forecasts, it is important to note not only GTM Research’s extensive experience analyzing the U.S. solar industry, but also political factors. Executives from the firm testified against Section 201 tariffs during the International Trade Commission’s process, and GTM Research has worked closely with SEIA for years. SEIA fought tariffs using every means at its disposal and continues to agitate against them even after Trump’s relatively measured 201 decision.

It is also important to note that market analysts are inherently conservative, and that even the most optimistic of analysts underestimated the global growth of solar PV over the past 10 years. Even in its base case, GTM Research expected solar market growth to stop at a level around 14 to 15 GW in 2019. Such a stall would be a new development, as the U.S. solar market has been growing relatively consistently over the last 15 years.

The company has issued this forecast even as it notes that solar is becoming competitive with natural gas, currently the least expensive form of generation, and as the solar industry continues to gain political power at the national level.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.