The US solar industry had its lowest quarter of installations since the start of the COVID-19 pandemic, according to the US Solar Market Insight report released by the Solar Energy Industries Association (SEIA) and Wood Mackenzie. In Q1 2022, price increases and supply chain constraints continued to suppress the solar market as the industry installed 24% less solar capacity than Q1 2021.However, the tide turned yesterday when the Biden administration announced a 24-month tariff exemption on solar modules manufactured in Cambodia, Malaysia, Thailand, and Vietnam. Without this action, massive project delays and cancellations would have continued throughout 2022, putting President Biden’s climate goals at risk.Since the Department of Commerce (DOC) announced in March that it would act on a petition filed by Auxin Solar and launch an antidumping investigation into Chinese companies working in Cambodia, Malaysia, Thailand, and Vietnam, solar module manufacturers halted shipments to the United States, causing an industry-wide module shortage. According to the US Solar Market Insight Q1 report, these supply constraints are expected to ease as manufacturers ramp up shipments to the United States in the coming months.

“The solar industry is facing multiple challenges that are slowing America’s clean energy progress, but this week’s action from the Biden administration provides a jolt of certainty businesses need to keep projects moving and create jobs,” said Abigail Ross Hopper, SEIA president and CEO. “President Biden has clearly taken notice of how drags on the industry are hampering grid resiliency. By acting decisively, this administration is breathing new life into the clean energy sector, while positioning the US to be a global solar manufacturing leader.”The effects of the DOC investigation was taking its toll on what was previously a burgeoning industry, with 2022 forecasts cut in half due to continued supply chain challenges and the anti-circumvention inquiry.

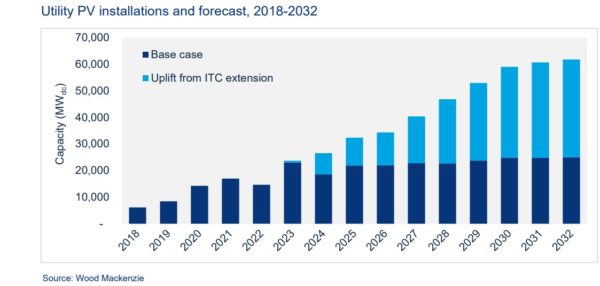

“The White House’s executive action brings relief to the US solar industry, which has been steeped in uncertainty regarding the anti-circumvention investigation initiated by the Department of Commerce in late March following a petition filed by Auxin Solar, a domestic module manufacturer,” said Michelle Davis, Wood Mackenzie’s principal analyst.“Despite this, this announcement is expected to create approximately 2 – 3 GW of upside potential to Wood Mackenzie’s 2022 base case outlook, assuming the global market resumes normal operations” Davis added.Nearly all areas of the industry had been hit, but the greatest pain was felt in the utility-scale sector. Utility-scale solar set an annual installation record in 2021 at nearly 17 GWdc; however, final installations in 2021 were lower than expected due to the many challenges faced in the industry. US solar suffered its sharpest decline in Q1 2022 and experienced its lowest quarter of installations since 2019. Multiple gigawatts of projects pushed their online dates from 2021 to 2022 or later. It also had the lowest number of new projects added to the pipeline since 2017.

The commercial solar market saw 28% quarter-over-quarter declines, while the community solar market shrank by 59% quarter-over-quarter. Project delays from interconnection challenges and supply chain constraints limited growth in both sectors.

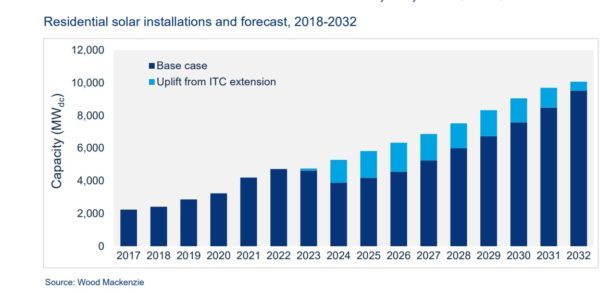

The bright spot in the US solar industry was the residential sector, where installations totaled 4.2 GWdc in 2021, setting an annual record and exceeding more than 500,000 projects installed in a year for the first time.

Residential solar has a bright future, as well. Wood Mackenzie forecasts 13% growth for residential solar in 2022, although analysts note that NEM 3.0 in California and the expiration of the ITC heavily impact the base case outlook from 2023 onward. California volumes are set to fall by 45% in the first full year of NEM 3.0, and Wood Mac forecasts a 2% market contraction in 2023. The market will grow everywhere but California by 18% during the same time period. An ITC extension would paint an even rosier picture, with residential increasing to 13 GWdc, or 21%, from 2023 to 2032.

Residential solar has a bright future, as well. Wood Mackenzie forecasts 13% growth for residential solar in 2022, although analysts note that NEM 3.0 in California and the expiration of the ITC heavily impact the base case outlook from 2023 onward. California volumes are set to fall by 45% in the first full year of NEM 3.0, and Wood Mac forecasts a 2% market contraction in 2023. The market will grow everywhere but California by 18% during the same time period. An ITC extension would paint an even rosier picture, with residential increasing to 13 GWdc, or 21%, from 2023 to 2032.

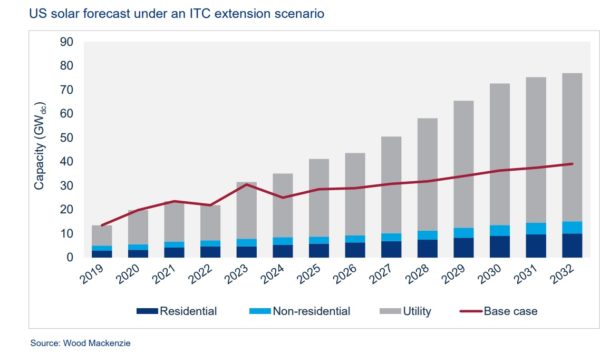

The 24-month tariff extension offers some certainty at a time when it is needed most, and it buys some time for industrial clean energy policies like long-term tax credits and manufacturing incentives to be put into place. Certainty around the investment tax credit (ITC) would be a major catalyst for the industry, increasing capacity installations over the next decade by 66%, according to the Q1 Insight report.

A 66% overall increase represents a 20% increase for residential, 15% for non-residential (commercial and community solar), and 86% for utility solar. Total installed solar in the United States under this scenario by 2032 would be nearly 700 GWdc compared to 464 GWdc in the base case.

For this Year in Review report, Wood Mackenzie released 10-year outlooks for each segment. Overall the solar industry is expected to more than triple from 120 GWdc installed today to 464 GWdc by 2032. While this is good news, it is far short of what’s needed to hit the Biden administration’s clean energy targets.

The Build Back Better (BBB) Act is unlikely to pass; however, there are opportunities for numerous clean energy provisions included in the BBB Act to make it to final legislation. The Wood Mac/SEIA report concludes that passage of an Investment Tax Credit (ITC) extension and other clean energy provisions would be a significant solar market catalyst, increasing installations by 66% in the next decade over the base case.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.