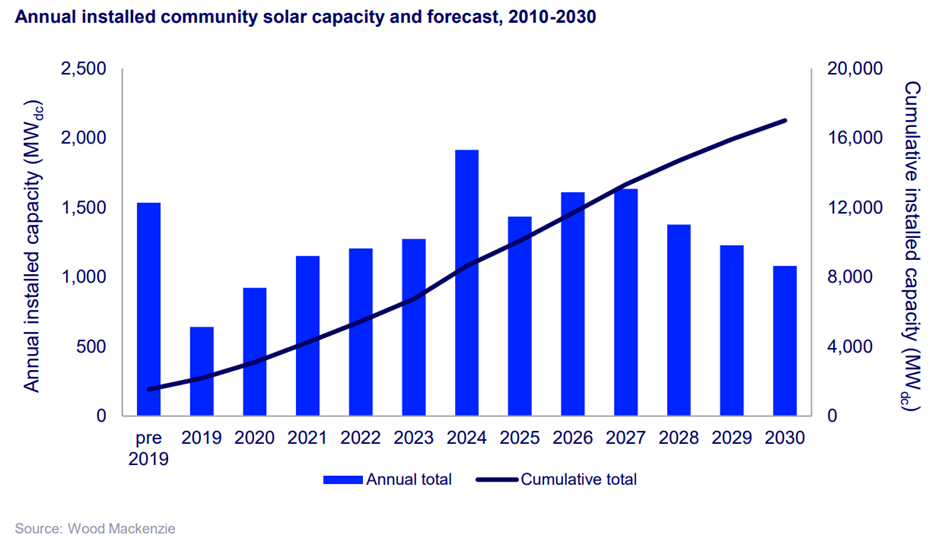

The U.S. community solar sector reached a major milestone in late 2025, officially surpassing 10 GW of cumulative installations. The milestone comes despite a tightening market that saw a 25% contraction in annual installations last year, according to the latest report from Wood Mackenzie and the Coalition for Community Solar Access (CCSA).

The industry installed 1.4 GW in 2025, a drop driven largely by a slowdown in mature markets like New York and Maine. However, analysts expect a rebound in 2026 with a projected 12% growth rate as new state programs and project pipelines begin to offset recent headwinds.

While annual growth in existing state programs is expected to contract by an average of 5% through 2030, the sector is currently supported by a massive development pipeline. Wood Mackenzie reports that more than 8 GW of projects are currently in development, with 29% of that capacity already under construction. Developers are currently working to meet strict start-of-construction and placed-in-service deadlines to secure the Investment Tax Credit (ITC) before federal policy shifts further.

Caitlin Connelly, senior analyst at Wood Mackenzie, said the segment’s near-term growth is anchored by a strong project development pipeline. She noted that developers are navigating a complex federal policy landscape and interconnection queue backlogs to ensure their current pipelines are built out as efficiently as possible.

With growth slowing in traditional hubs, the industry is looking toward Illinois and Mid-Atlantic markets to drive national numbers in 2026. Long-term growth is now heavily dependent on the establishment of new state markets in Ohio, Iowa, Pennsylvania, and Michigan. A new avenue for growth is the community-scale segment. These are projects up to 20 MW in size that connect directly to the distribution grid. Unlike traditional community solar that requires specific state legislation, these projects are being prioritized by utilities to meet rapid demand growth and improve grid reliability.

The cost to acquire subscribers fell 12% on average in 2025. Wood Mackenzie attributes this decline to the wider use of consolidated billing and digital marketing tools. Low-to-moderate income (LMI) subscribers remain the most expensive segment to acquire at $100 per kW. Additionally, the subscription management market is rapidly narrowing. Following Perch Energy’s acquisition of Solstice, four major entities now manage 55% of all operational community solar capacity in the U.S.

Wood Mackenzie maintains a base case for the industry to exceed 12 GW of potential through 2030, though the removal of the ITC in 2030 remains a significant concern for new program design. In a high-case scenario involving favorable state policy and interconnection reform, Wood Mackenzie projects a 1.2 GW uplift to the five-year outlook. Conversely, a low-case scenario driven by tax credit complications and limited state intervention could reduce the outlook by 1 GW.

Jeff Cramer, CEO of CCSA, said said the expansion of mid-scale, front-of-the-meter solar and storage into new markets signals that the industry is diversifying and adapting in ways that will serve customers and the grid for decades to come.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.