U.S. distributed generation solar module prices increased in Q3, 2025, likely due to policy deadlines and ramped up procurement strategies, said a report from supply chain platform Anza.

Projects over 1.5 MW in capacity were faced with a September 2, 2025 deadline to reach a 5% project spend threshold to qualify for the federal Investment Tax Credit. This led to a rush in procurement in Q3, pulling ahead Q4 demand and pushing prices higher, said Anza.

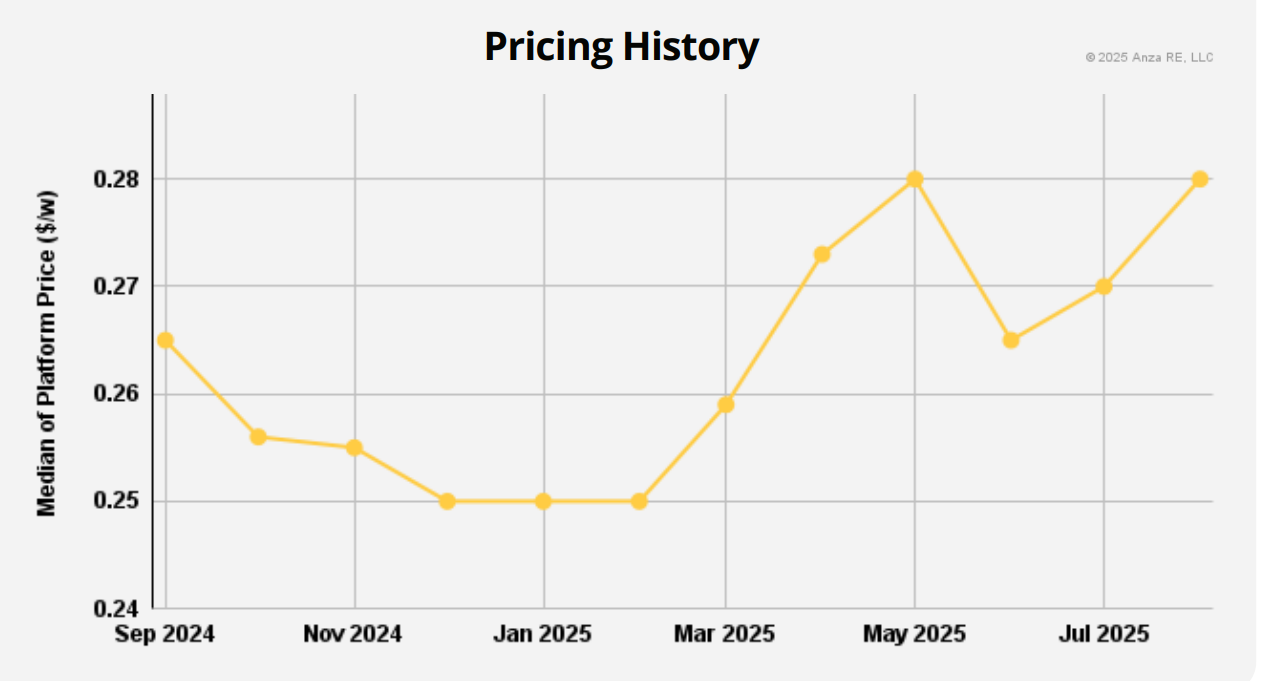

Median Anza platform prices rose 3.7%, or $0.015 per watt from June to August, returning to the May high of $0.28 per watt.

The price data in the report reflects median distributed generation list prices from over 40 module suppliers participating in the Anza platform, which the company said captures over 95% of the U.S. module supply.

Another policy altering procurement patterns is the restrictions on solar imports from nations deemed Foreign Entities of Concern (FEOC). The act denies technology-neutral tax credits, including the 48E Investment Tax Credit and the 45Y Production Tax Credit to projects that are in violation of FEOC rules. And 45X manufacturing tax credits are denied to U.S.-produced components that exceed allowed thresholds of Chinese material inputs. Generally, FEOC restrictions apply to Chinese businesses or entities in which China has “influence” or ownership stake. Read a guide to FEOC compliance here.

Anza said FEOC-noncompliant module prices s increased 9.2% from June to August, while FEOC-compliant prices rose 4.9%. The report said the pattern “reflects buyer reliance on established suppliers and early FEOC planning.”

“Many buyers rushing to lock the ITC before September 2 appear to have leaned on familiar brands and existing relationships rather than FEOC status, which could have contributed to the sharper FEOC-noncompliant price increase,” said Anza.

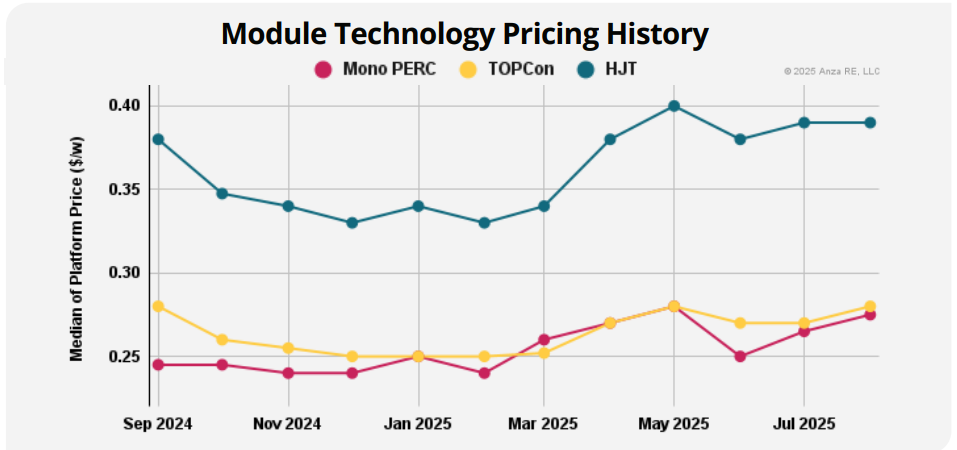

Mono PERC solar modules rose approximately 10% during the period, which Anza said possibly reflects its reliance on a more mature supply chain compared to alternatives.

The report said the PERC vs. TOPCon spread compressed to nearly zero, with U.S. suppliers favoring PERC likely due to intellectual property concerns surrounding TOPCon. HJT supply remains limited, with pricing at a premium, said Anza.

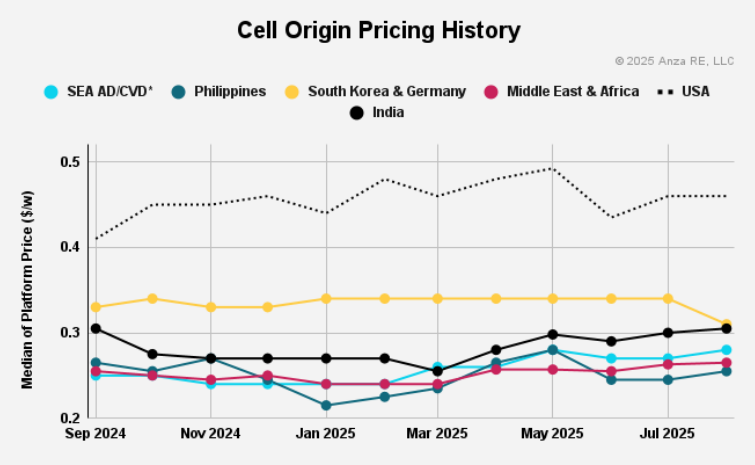

As for solar cells, prices changed based on country-of-origin from the period of June through August. For U.S. solar cells, Pricing increased 2.5 cents (5.7%), reaching $0.46 per watt.

Cells from Malaysia, Thailand, Vietnam, Indonesia, Laos increased 1 cent per watt, or 3.7%, reaching $0.305/W as AD/CVD exposure kept capacity tight, said Anza. Cell prices in India increased 1.5 cents (5.2%) to $0.305 per watt. And cells originating in South Korea and Germany fell 3 cents (-8.8%) to $0.31 per watt.

“Looking ahead, pricing trends will depend on factors such as supplier origin strategies, trade actions, and compliance preparations. In particular, anticipated AD/CVD determinations on India, Indonesia, and Laos, as well as a potential Section 232 tariff on polysilicon and its derivatives, could create material upward pressure on module costs in Q4, especially if the polysilicon tariff is applied broadly rather than with limited country exemptions,” said Anza.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.