Worldwide, production of lithium-ion battery cells is expanding rapidly. Electric vehicles are the dominant driver of demand, and both home energy storage and grid-scale batteries are expected to contribute as well.

A report from Clean Energy Associates (CEA) outlined that by 2025, global manufacturing of lithium-ion battery (LIB) cells is expected to triple from 2022 levels. It said the U.S. is expected to produce more battery cells than the European Union, largely due to incentives created by the Inflation Reduction Act of 2022.

“The IRA attracted outsized investments in domestic cell production capacity with $35 per kWh tax credit available and bolstered by an additional $10 per kWh tax credit for assembled modules,” said the report.

CEA is a manufacturing quality assurance firm with insight into global battery energy storage systems supply chains. Its Q4 2023 report focuses on emerging trends in this space.

While the U.S. and Europe have a sizeable share of the global LIB battery production supply chain, it is still heavily dominated by China, said the report.

CEA said the U.S. has taken an “aggressive approach” to LIB supply chain expansion, offering a “raft of incentives” via the Inflation Reduction Act. However, upstream legs of the supply chain take a long time to set up, with brine mining, refinement, separators, and more requiring considerable time to reach operations. CEA said western markets need “a sense of urgency” if supply chain diversification is a desired goal.

CEA said collapsing lithium prices has led to a cooling-off in demand for chemical alternatives to the mainstream nickel manganese cobalt (NMC) and lithium-ferro-phosphate (LFP) chemistries. This leads to a negative impact on commercialization for new technologies like sodium-ion batteries. However, CEA said more evolutionary chemistries like lithium manganese iron phosphate (LMFP) may find their way into electric vehicles and energy storage sectors as early as 2025.

Growth in midstream production capacity is helping push cost reductions for LIB cells, said the report. Cathode active materials and anode active materials are being produced with increasing capacity, lowering the overall cost of batteries.

The report said that supply chain growth is outpacing demand as major economies aim public policy at localization of battery cell and cell subcomponent production assets.

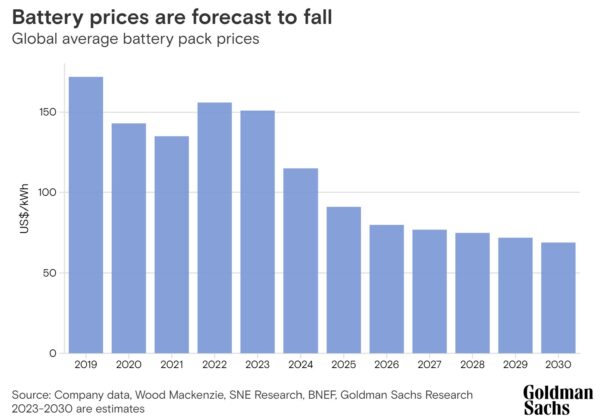

A report from Goldman Sachs forecasts a 40% reduction in battery pack prices over 2023 and 2024, followed by a continued decline to reach a total 50% reduction by 2025-2026. Goldman predicts that these price reductions will make electric vehicles as affordable as gasoline-powered vehicles, leading to increased demand.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.