Lazard has released its Levelized Cost of Energy (LCOE), Storage, & Hydrogen indexes. For the first time in its history, the document has shown pricing increases for solar power’s LCOE. We’re also seeing continued price decreases in hydrogen as that industry scales.

The solar power price increases were noted to be at least partially driven by the increases in cost of capital. The higher the up-front cost of construction, the greater the increase in LCOE an electricity generation source will feel.

For the purpose of this document, LCOE v16.0, Lazard choses 8.0% as the cost of debt. The group’s sliding scale page shows various generation source’s sensitivities to cost of debt combined with cost of equity, and after tax IRR/WACC. For instance, the relatively low up-front costs of gas combined cycle shows a 16% increase in LCOE from 5% cost of debt to 10% cost of debt. While heavy up-front utility-scale solar increases from $45/MWh to $72 – a rise of 60%.

After being at just above 0% since 2019, the base U.S. interest rate has increased to nearly 5%.

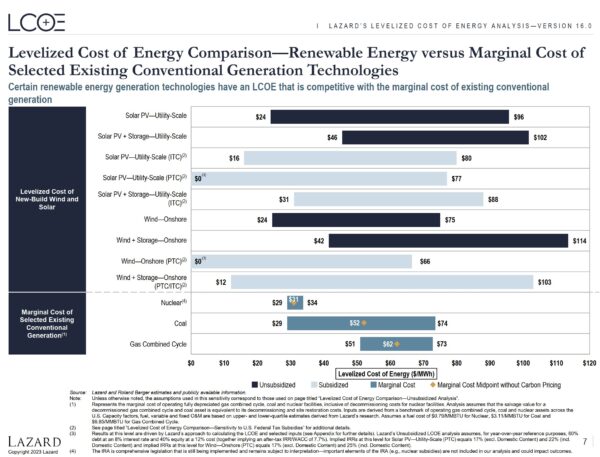

The Inflation Reduction Act (IRA) made its way into Lazard’s analysis and showed a potential for some wind and solar power projects to have an effective $0/MWh LCOE price. In the chart, the analysis compares renewable energy versus the marginal cost – essentially the cost of fuel and O&M – of running certain generation technologies.

In this comparison it could be that some new utility-scale wind and solar is cheaper than running all other generation source for instantaneously used generation.

The document suggests that some new wind and solar can potentially be obtained for an LCOE of $0/MWh. pv magazine USA has speculated on the same potential situation arising once the IRA gets going.

Lazard explained this chart anomaly:

Results at this level are driven by Lazard’s approach to calculating the LCOE and selected inputs (see Appendix for further details). Lazard’s Unsubsidized LCOE analysis assumes, for year-over-year reference purposes, 60% debt at an 8% interest rate and 40% equity at a 12% cost (together implying an after-tax IRR/WACC of 7.7%). Implied IRRs at this level for Solar PV—Utility-Scale (PTC) equals 17% (excl. Domestic Content) and 22% (incl. Domestic Content) and implied IRRs at this level for Wind—Onshore (PTC) equals 17% (excl. Domestic Content) and 25% (incl. Domestic Content).

Essentially, with the Production Tax Credit paying investors, and taking into account the Domestic Content 10% tax credit adder, a developer could price their power purchase agreement at $0 and still make all investors and themselves financially happy at standard market rates.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.