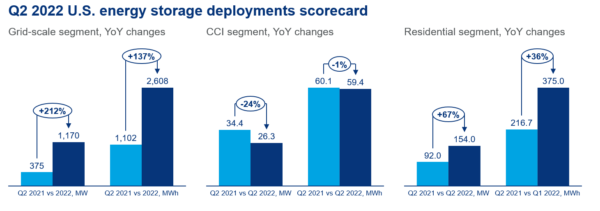

The United States utility-scale energy storage market continues to accelerate as 2,608 MWh of storage was brought online in Q2, 2022.

According to Wood Mackenzie and American Clean Power Association (ACP), grid-scale battery growth was largely driven in Texas, which deployed about 60% of the nation’s installed capacity.

However, the sector has been weighed down by supply issues. Project pipelines are facing rolling delays into 2023 and beyond. More than 1.1 GW of projects projected to come online in-quarter were delayed or cancelled, but 61% of this, 709 MW, is scheduled to reach commercial operations this year, said Wood Mackenzie.

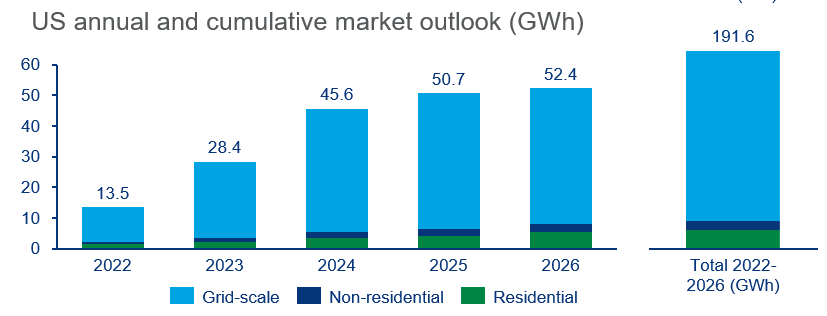

Wood Mackenzie said it sees the United States on a path to be a 27 GW annual market by 2031, and 83% of that figure will be utility-scale storage. However, projections for 2022 and 2023 have been trimmed by 34% and 27%, respectively, due to disruptions from antidumping and countervailing duties tariff suit in the second quarter. Solar-plus-storage projects were impacted heavily by the investigation, leading to about 35% of grid-scale projects being delayed as a result.

“Supply chain issues, transportation delays and interconnection queue challenges were the main drivers behind delays in the commercial operations date for many projects,” said Vanessa Witte, senior analyst at Wood Mackenzie’s energy storage division. The ongoing enforcement of the Uyghur Forced Labor Prevention Act (UFLPA) is expected to continue to hamper imports.

Key drivers for growth in energy storage are the Investment Tax Credit for co-located solar and storage and the standalone energy storage credit, both set at 30% of the cost of equipment. Following the passage of the Act, Wood Mackenzie forecasts 59.2 GW of storage capacity will be added through 2026.

“The U.S. energy storage industry is reaching maturity,” said Jason Burwen, vice president of energy storage at ACP. “Energy storage is now regularly being installed at over a gigawatt per quarter. In addition, Texas overtaking California this quarter should serve as a reminder that generators, customers, and grid operators in all geographies are increasingly relying on energy storage. Combined with the tailwinds of newly available tax credits from the Inflation Reduction Act, the question for investors and grid operators now is not whether to deploy storage, but how much storage to deploy – and how fast.”

Residential energy storage had a record quarter as well, with 375 MWh installed in Q2, building upon the previous record of 334 MWh installed in Q1. Demand continues to rise in this segment, boosted by increased grid failures and extreme weather events. An increased number of solar installers now offer energy storage as part of their offering. The standalone energy storage tax credit in the Inflation Reduction Act is expected to support the market for retrofitting batteries to existing residential solar systems.

Community, commercial and industrial storage installed 59.4 MWh, making it the lowest quarter recorded for MWh capacity since 2019. “Market players look forward to the emergence of a more diverse market, but current deployment remains limited to a few policy leaders in California, New York and Massachusetts,” said Chloe Holden, research analyst at Wood Mackenzie, and one of the authors of the report.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

In a Zero Pollution Earth (led by USA…???) requiring 180,000TWhrs/yr of Energy to meet ALL its Energy Needs, it would require 40,000TWhrs/yr of S2S (Sunset-To-Sunrise) Energy Storage or 120TWhrs/DAY.

The USA would require about 10% of the above. These “Mickey Mouse” Steps and Projects (2.6GWhrs/yr) will take the USA … 4000+ years… Is this REAL…???

Just use UHES (see… youtube channel zeropollution …. UHES ). for the Solution for S2S Energy Storage… Grid Size…