There are many future projections suggesting significant volumes of solar power will be deployed across the United States in the coming years. For instance, there are currently implemented state laws which will drive an estimated 73 GW of renewable capacity through the end of the decade, there are hundreds of gigawatts in grid operator queues through the end of 2023, and of course the fact that wind and solar are about the cheapest electricity sources – and getting cheaper.

Fitch Solutions’ 10-year forecasts for the US wind and solar power sectors project capacity growth to average 3.9% and 7.9% between 2022 and 2028, respectively – with upward forecast revisions likely as more corporations commit to renewable electricity targets and the procurement process is further simplified.

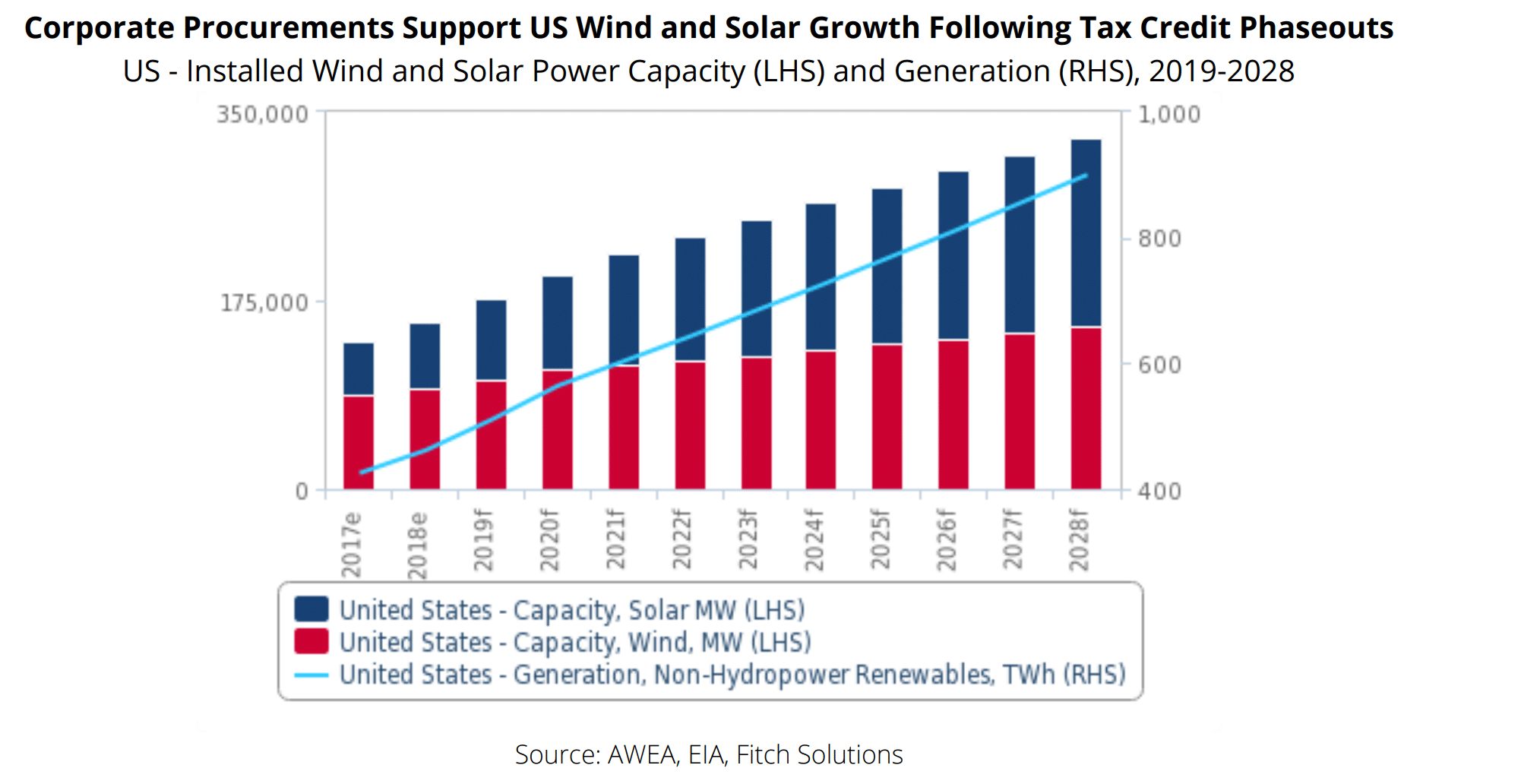

As a whole (below chart) they see US wind and solar cumulative volume to increase from approximately 175 GW of capacity at the end of 2019, to just short of 1 TW of capacity. Concurrently with this growth, they see electricity generation from these sources to increase from just over 400 TWh of generation in 2017 just over 900 TWh in 2028. US electricity use has been steady just short of 4,000 TWh for about a decade.

Fitch cites two sources for historical data. Rocky Mountain Institute is reporting 15.5GW of renewable electricity capacity from wind and solar projects between 2014 and 2018. And, via BloombergNEF, in the first half of 2019, U.S. companies procured 5.9 GW, which was near the 2018 full year total of 6.5 GW.

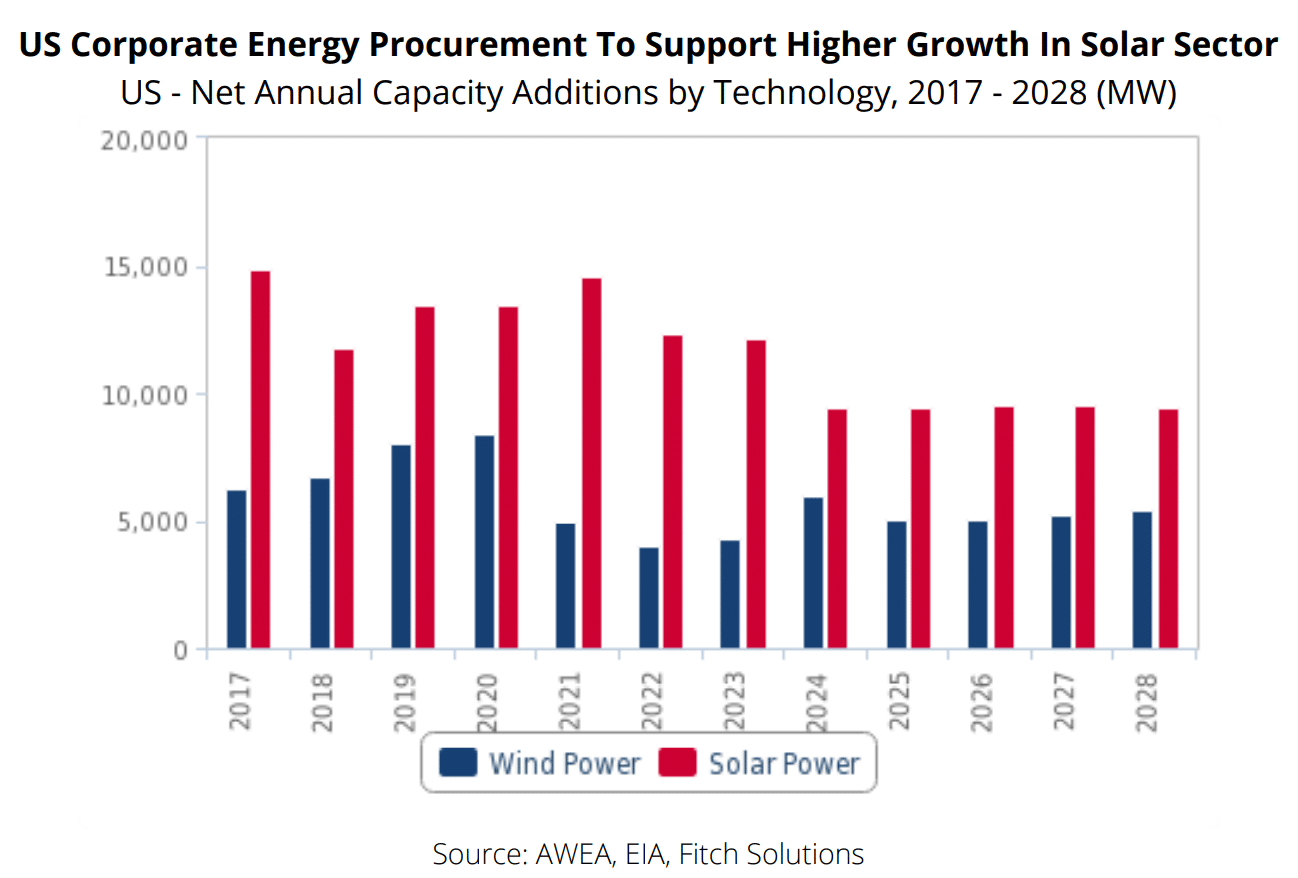

Going forward, Fitch sees solar power likely overtaking wind, as solar can more often be installed onsite, it has a more favorable tax credit phase out schedule – as well – its time of generation more so lines up with peak demand from many companies.

As pv magazine USA has noted, power purchase agreements (PPA) for solar have become more varied in what is offered. Fitch suggested that developers would increasingly seek corporate PPAs to diversify revenue, contract with credit-worthy corporate buyers and, with multi-buyer PPAs, diversify payment default risk. In gaining these corporate contracts, Fitch suggests that increasing flexibility in contracts, including shorter-term term PPAs of 5 to 10 years and multi-buyer PPAs, to fit a wider variety of company goals.

The report notes that Engie expects half of its renewable projects between 2019 and 2021 to come from PPAs with companies or cities. Engie has has signed a total of 3GW of corporate PPAs with US customers including Target, Boston University, and T-Mobile.

Over the course of the period studied, solar procurement is projected to peak at just short of 15 GW in 2021 and then tail off toward 10 GW per year through 2028 – for around 117 GW of total capacity by the end of 2028.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

Am I missing something? From the first chart it looks like they are saying that wind+solar capacity will go from 175GW to under 350GW (left hand side) and production will go from 400TWh to 900TWh (right hand side).

That will be a real shame if we can only double s+w capacity in 10 years. I like the 5x in the article better, but then production should be closer to 2,000TWh.