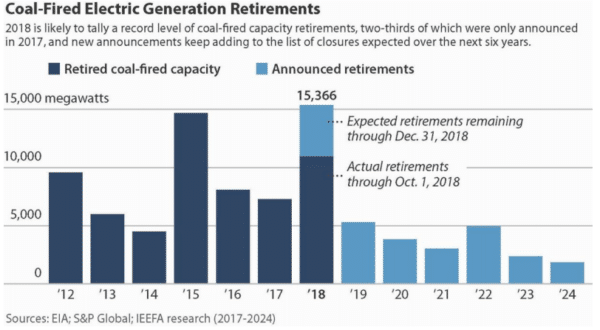

Despite President Trump’s promises to bring back coal, the burning of rocks to supply electricity is in a terminal decline, in the United States as well as globally. As the latest in this trend, the Institute for Energy Economics and Financial Analysis (IEEFA) has released a report which finds that by year’s end 15.4 GW of coal plants will have retired in the United States, the most in any year to date.

IEEFA notes that in addition to this, 21.4 GW of coal-fired plants are already planning to retire over the next six years; although the actual volume is expected to be much greater. The organization notes that 2/3 of the 2018 retirements were only announced in 2017, which it says shows that utilities are shortening their lead times before closing plants.

And while coal plants have been closing for years due to pressure from low-cost gas, IEEFA further identifies the falling cost of renewable energy as a factor in making coal relatively uneconomic.

But this does not mean that solar will necessarily replace all of this coal capacity. Large-scale solar is the least expensive form of electricity in many parts of the nation, and distributed solar brings additional value which can save ratepayers substantial sums in terms of deferring large utility investments.

The coal retirements this year span 22 plants in 14 states, and in some of these locations wind is a more less expensive resource than solar per unit of electricity delivered. But there is a third resource to be considered: gas.

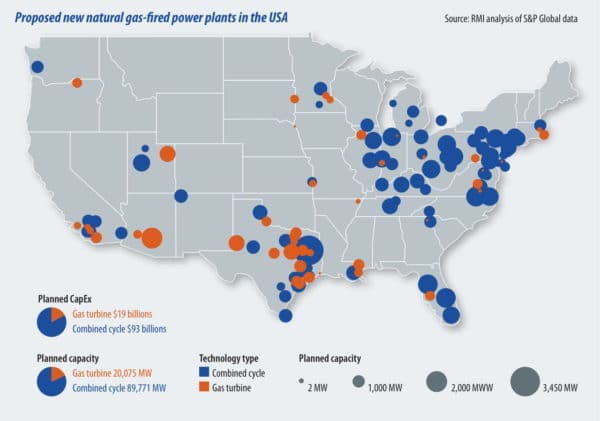

Outpacing the 15.4 GW of coal retirements, the U.S. Department of Energy has estimated that 21 GW of natural gas-fired power plants will come online this year, with 110 GW planned per year over the next seven years.

And decisions will not necessarily be made upon economics. Regulators in Michigan and New Orleans have shown that they will approve the gas plants that utilities want to build without full consideration of other options, and may not reconsider these decisions even amid considerable scandal.

Geography matters

While California may be closing existing gas plants in favor of clean energy alternatives (often portfolios of solutions where renewables are only one component), much of the new gas capacity which is planned is coming in exactly the locations where coal is retiring.

A massive volume of gas plants are planned for the PJM Interconnection grid, with a significant volume in the Ohio River Valley, where some of the largest coal plants are retiring. Furthermore, the state governments in the three states with much of this capacity – Ohio, Pennsylvania and West Virginia – are not exactly leaders in supporting renewable energy.

That does not mean that the entire Midwest should be written off. Indiana utility NIPSCO is planning to replace its retiring coal fleet largely with renewable energy, and in Illinois the Future Energy Jobs Act is leading to a boom in solar at multiple scales.

Two of the other key states where coal plants are retiring – Florida and Texas – also look promising, as they are rapidly becoming some of the nation’s largest solar markets. In Texas this is enabled by the transmission lines build for the state’s Competitive Renewable Energy Zones (CREZ), and in Florida utilities are often voluntarily building massive capacities of solar.

The zero-marginal cost nature of solar (and wind) must also be considered. Even if new gas plants are built, in areas where they must compete in wholesale markets they will be undercut by solar and wind, as these resources have no fuel costs and as such can bid in at zero.

As such, the rush to gas is likely to be a rush to stranded assets, and it remains to be seen how many of the gas plants which are planned will be cancelled even before construction begins.

But ultimately this will be a state-by-state and grid-by-grid fight for the future, as economics alone will not carry the day. The question of how rapidly the energy transition reaches its full potential is a political one.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

According to EIA data there was a total of 21.3GW of NG generation planned to come on-line in 2018. Through August this was supposed to be 18.6GW. Of this 18.6GW only 12.2GW (~66%) of NG had actually come on-line through August. I don’t know if the 6.4GW that didn’t come on-line in the time frame was just delayed or has been canceled. I hope canceled. In the same period 67% of wind projects were completed and 85% of solar. And 165% of batteries.

I hope banks are getting leery about investing in these decade projects that will likely be stranded by lower cost alternatives. One good price hike in NG and fear would certainly be put into the equation. Or if the fracking dominoes actually start falling.