In October 2017, NRG asked California regulators to withdraw consideration of its 262 MW Puente Gas plant in Southern California’s Ventura County. The project was controversial, as it had been planned for a low-income area, but that was not what made this project historic.

Due to two other generators going offline, there was a need for capacity in the area, which the Puente plant would have addressed. Instead, utility Southern California Edison put forward an alternate plan involving transmission upgrades, energy storage, and renewable energy, which California Public Utilities Commission (CPUC) found could meet these needs. And this led to Puente becoming the first gas plant in the state’s history to be rejected by CPUC.

It would not be the last time decision-makers in California passed over gas infrastructure in favor of clean energy. In the past year, two upgrades to gas power plants have been cancelled, and three existing gas plants have lost lucrative contracts, without which they will likely be shut down.

Additionally, in March 2018, the state’s grid operator approved a plan by Pacific Gas and Electric Company involving a combination of grid upgrades, renewable energy, and storage instead of renewing the contract for a petroleum-fired plant near Oakland. This is not to mention the roughly 100 MW of battery storage that CPUC approved in May 2016 to make up for unavailable gas generation due to the Aliso Canyon leak.

Neither is this limited to California. In February, utility Arizona Public Service (APS) announced that it will sign contracts involving 50 MW of battery storage and 65 MW of solar, as the result of an all-source solicitation wherein the solar+storage project beat out gas peaking plants to meet demand between 3:00 p.m. and 8:00 p.m. in the summer.What all of these examples point to is clean energy – combinations of solar, wind, batteries, and other non-fossil resources – outcompeting both new gas projects and in some cases existing plants.

Crisis in conventional generation

Conventional generation is in crisis in the United States. This started with coal plants, which have been under multiple market pressures. Between cheap gas from hydraulic fracturing bringing down wholesale power prices and the cost of complying with new emissions regulations, coal has simply been unable to compete with a massive build-out of new gas projects. And with U.S. electricity demand stagnating since the 2008 recession, generation has become a zero-sum game.

The result is that 37 GW of mostly old and uncompetitive coal plants retired between 2010 and the end of 2015. In a few regions such as California, Texas, and the Plains States, solar and wind have also contributed to even lower power prices, however in most regions there is too little of either for much of an effect to be seen, with gas already crushing prices.

However, in the last few years a new trend has emerged. Solar, wind, and battery storage are representing a new threat not just to coal, but to other forms of generation including gas plants.

California is one of the regions on the tip of that spear, and this can be seen clearly in statistics. The output of gas power plants on the California Independent System Operator (CAISO) grid has been falling every year since 2014, and represented only 28% of generation in 2017. The capacity of gas plants in CAISO has also fallen each year, with the retirement of less efficient combustion turbine peakers more than making up for a modest increase in new combined cycle units. As all of this is happening, renewables are continuing to boom, with solar alone reaching 19% of California’s power supply in 2017.

Economic and technical factors

The vast majority of the wind and solar that has gone online, both in California and nationally, has been supported by mandates and incentives, most notably renewable portfolio standards. But solar and wind are now competing directly in the market, and their low prices have led to new market drivers, such as increasing corporate procurement of renewable energy, contracts signed under the Public Utilities Regulatory Policy Act of 1978 (PURPA), and many of the nation’s largest utilities voluntarily procuring and/ or building large-scale solar and wind projects.

Just as gas outcompeted coal, large-scale solar and wind are now outcompeting gas in the energy market, with contract prices as low as $30/MWh for solar and below $20/MWh for wind, and solar project bids as low as $22/MWh. Additionally, once solar or wind plants are built they will always out-bid any thermal energy source, which has to buy fuel in wholesale power markets, as renewables have near-zero marginal cost.

However, gas plants do not only supply energy. Many gas plants, especially “peaker” plants supply flexible capacity to the grid, and for this, intermittent solar and wind are not in an equal position to compete.

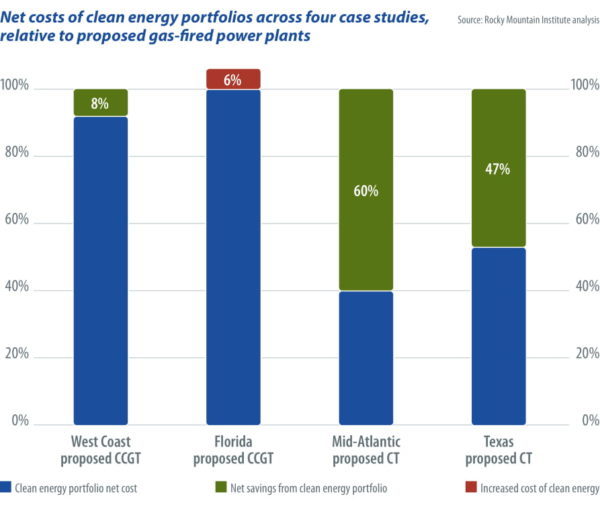

However, energy storage and other resources can supply this flexible capacity when paired with renewable generation. Earlier this year, Colorado-based research organization Rocky Mountain Institute (RMI) published The Economics of Clean Energy Portfolios, an economic analysis of clean energy portfolios including renewable energy and batteries, and also such resources as demand response and energy efficiency, combined with system upgrades in order to compete with gas plants.

The findings of this report were stunning: In three out of four case studies from across the United States, these clean energy portfolios took care of the requirements that gas plants had previously met, at a lower cost. And in the fourth case, the cost was only slightly higher, reinforcing the findings of decision-makers in California.

Rush to gas

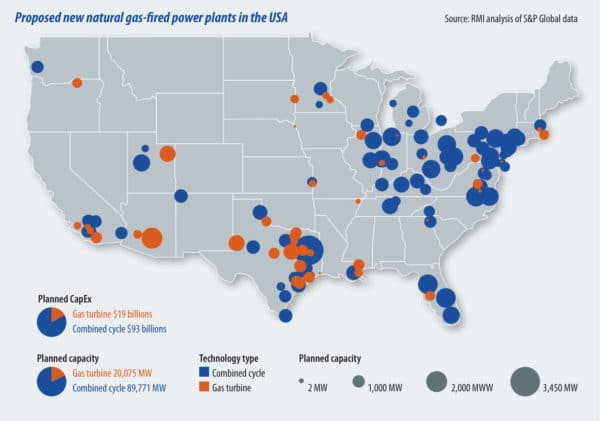

These revelations about the ability of solar and storage to compete with gas come as utilities and developers are preparing a truly massive build-out of gas-fired generation in the United States.

The U.S. Department of Energy’s Energy Information Administration (EIA) estimates that a total of 21 GW of new gas plants will come online by the end of 2018, as part of 110 GW of gas plants that are planned over the next seven years, with many in Texas, as well as on the PJM Interconnection grid which serves much of the Eastern United States. According to Rocky Mountain Institute, this will represent a $112 billion investment, plus another $30 billion worth of pipelines.

To an outside observer, this rush to install gas plants may seem strange. However, it is important to remember that both utilities and the EIA continue to predict that electricity consumption will rebound, despite making this assumption consistently over the past decade and being proven wrong year after year.

In its latest Annual Energy Outlook, the EIA has also predicted that virtually no solar will be built from 2020-2025 after the 30% federal Investment Tax Credit (ITC) declines, which is contrary to the findings of all major clean energy research firms. Finally, many market observers are betting on gas prices staying low.

And this 110 GW may only be the beginning. Based on average plant ages at retirement, RMI estimates that roughly half of U.S. thermal generation will retire by 2030. The organization estimates that if we replace all of this capacity with gas plants, this will represent $520 billion in capital expenditures.

Geography

It is already a fact on the ground that clean energy is replacing both new and existing gas plants in California. But for the rest of the United States, this competitiveness varies according to policy, gas plant design, and geography, with the last being the most fundamental.

“Geography dictates everything,” Mark Dyson, a principal at RMI and an author of The Economics of Clean Energy Portfolios, tells pv magazine. This includes not only the productivity of solar and wind, and thus the per kilowatt hour price of its generation, but also wholesale electricity prices and daily load profiles, which in turn dictate ramping and flexibility needs, and which in turn are influenced by the kinds of clean energy that have already been deployed locally.

When looking at the composition of clean energy portfolios that could replace gas plants, RMI used solar only in two of the four cases – in Texas and Florida – and not in PJM and California, where it relied on wind and other resources. And in all cases, the study bet heavily on energy efficiency, energy storage, and demand response.

RMI explains that solar was left out in California as it is already struggling with the duck curve, and that as such more solar will exacerbate flexibility needs. This does not mean that solar with storage is not able to compete, but that wind has a greater advantage. Texas shows the opposite. There the greatest need is still to meet peak demand in mid-day, and here solar is uniquely positioned to compete with gas, even if not paired with storage. The same is true of Florida, although solar is less productive there than in Texas.

The PJM Interconnection grid represents a more nuanced situation. While RMI chose not to include solar in its clean energy portfolio, like much of the rest of the United States, peak electric demand is still during the daytime in the summer. Also, as the region is seeing more wind than solar deployed, hourly wholesale prices could tip the economic balance in favor of solar.

Types of gas plant

There is another critical factor to consider as to whether or not clean energy can outcompete any given gas plant, and that is the kind of gas plant that is being considered. Gas plants broadly fall into two main categories, based on the kind of turbine: combined cycle gas turbines (CCGT), which are mostly used for base load or mid-merit generation, and combustion turbines (CT), which are used as “peaker” plants.

CCGT plants are more expensive to build, and burn gas more efficiently, but typically cannot ramp as quickly. CT plants are cheaper to build and conversely less efficient, but able to ramp faster. CCGT represents most of what has been deployed in recent years, and what is planned for the next decade.

Two of the plants in RMI’s analysis were CT, and two were CCGT. Broadly speaking, CT plants were far less competitive. As they run at higher per kilowatt hour costs, RMI found that they could largely be replaced with demand response and energy efficiency, both of which are cheap. The competition was much tighter between the clean energy portfolios and CCGT.

Policy

While geography may be the fundamental factor, policy is the most definitive. The simple fact is that solar, wind, storage, and other elements of clean energy portfolios will not be chosen for their economic advantages if these advantages are not properly valued, or if they are not allowed to compete with gas plants.

An unfortunate real world example of the latter can be seen in Michigan, where the Michigan Public Service Commission (MPSC) gave DTE Energy approval to build a 1.1 GW gas plant despite a Union of Concerned Scientists (UCS) analysis which suggested that clean energy could meet the same needs for only two thirds of the cost. In what can be seen as an admission of regulatory capture, one commissioner noted that MPSC did not fully consider alternatives to DTE’s request.

Where clean energy projects and portfolios are allowed to compete, the area of valuation is critical, particularly for energy storage. Batteries and other forms of energy storage can provide multiple value streams from multiple uses, but are often prevented from doing so in different grids due to market structures.

Where clean energy projects and portfolios are allowed to compete, the area of valuation is critical, particularly for energy storage. Batteries and other forms of energy storage can provide multiple value streams from multiple uses, but are often prevented from doing so in different grids due to market structures.

This is expected to change with the implementation of the Federal Energy Regulatory Commission’s Order 841, which was finalized earlier this year and requires grid operators to craft rules to allow energy storage to participate in markets. However, it will still take years for grid operators to create and finalize these new market structures. “Different ISOs are in different stages of that, but we are all headed in that direction,” notes Janice Lin, Executive Director of the California Energy Storage Association and CEO of Strategen.

But issues of valuation can affect other resources as well. In its report RMI assumed the ability to procure energy efficiency and demand response in many of its clean energy portfolios, but the valuation of such resources and their ability to participate in meeting capacity needs varies from grid to grid.

Existing and future gas plants

It is important to note that RMI’s analysis has shown clean energy as competitive under current policies. When $7.50 per ton price on carbon was added, clean energy won every time. So when climate change is considered, it is unlikely that there is a credible rationale to build another gas plant anywhere in the United States.

But the story of clean energy outcompeting gas does not end there. It is important to note that in California clean energy is not only replacing new gas plants, but existing ones as well. This was clearly laid out in a recent UCS study, which found that at current prices a solar-heavy clean energy portfolio could cost-effectively replace a quarter of California’s existing gas fleet. Similar analyses have been done in other states, with Strategen reporting positive findings regarding the ability of batteries to replace gas plants in Minnesota and New York.

This may not happen if utilities are allowed to continue to call the shots. As the recent case of Entergy New Orleans fake support for a gas plant shows, some utilities are willing to go to great and ethically dubious lengths to support their chosen forms of generation.

Requiring open-source solicitations has been identified as a key means by which to force utilities to consider clean energy options. And as utility Xcel Energy’s recent solicitations in Colorado have shown, even industry insiders have been surprised at the low prices that have come back.

Ultimately, the question is not whether or not clean energy will outcompete any given gas project. Given the continued price declines for solar and battery storage, the question is when. This means that even if any of the 110 GW of gas plants that are being planned are considered competitive when built, many of them may not be for long.

So even if utilities and developers pursue such projects, this story is not likely to go the way they plan. When these plants become large piles of idle steel that have defaulted on their loans, the investors who collectively poured hundreds of billions of dollars into them – as well as utility ratepayers who are on the hook for paying them off – may have grounds for lawsuits against those who deceived them on expected returns.

But for the solar, battery, wind, and energy services industries, this is an opportunity worth hundreds of billions of dollars, ripe for the taking.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

Like too many other articles of this kind, this one frustrates me because of it fails to critique its own solutions. If you are going to plan the future, the first rule is to second guess yourself. You need to figure out why your intended solution might be flawed, and modify them so that they work better.

At RMI, the original founder, as well as the group itself, seems to pride themselves on being the gadflies of the energy world, challenging convention and daring someone to reply. In this case, they would be in a better position to do this if batteries had a more stable track record of performance and if their prices were not so clouded by press releases and hype.

To my knowledge, most of the utility battery systems built in the U.S. thus far are for niche markets such as extreme peak demand, and the solar-integrated ones are subsidized by the ITC and in some cases (such as Hawaii) state tax credits as well. However, in ERCOT where I live (and probably most other ISOs), the majority of our electric use is baseload. If you are arguing for universal adoption, then you have to account for baseload, not just peak.

And assumed battery life of 20 years? We can only hope this holds.

Regarding the potential for DSM, it is theoretically vast. But in this country, it is mostly voluntary on the part of individual customers, even if there are utility programs to incent it.

Hello Mr. Robbins,

I am unsure what you mean by using the term “baseload” regarding electricity use. I have only ever seen baseload used as a term relating to generation, not consumption, and in that regard it is a somewhat archaic concept.

If what you mean is that there is ample electricity demand at non-peak times, then that is easily addressed by solar and wind combined with batteries. Batteries can meet a variety of electric needs, and there is no reason why they can only be applied for the use cases that you describe. Nor is there any lack of a track record of performance for batteries, as we have had large-scale energy storage on various grids for many years.

However, in terms of ERCOT the pressing need is meeting peak demand, given that this has an outsized impact on both electricity prices and drives new capacity procurement. For this solar works quite well (with or without batteries), which is why many gigawatts of solar are being built in ERCOT right now. DSM can also work, but you need to design the market so that calls for DSM activation go out in advance, as California has done: https://pv-magazine-usa.com/2018/09/10/california-grid-operator-opens-doors-for-behind-the-meter-batteries-distributed-resources/

Also, while there is still a lot of work to be done in making the policies work in other grids there are a number of programs that do incorporate DSM.

As for assumed battery lives of 20 years, I don’t in any place assume this for lithium-ion batteries. I am under the impression that flow batteries perform better in this regard. But even if lithium-ion batteries have to be swapped out, that isn’t a critical failure. The solar industry does this all the time with inverters.

So while you at times raise interesting points I do not see how this in any way refutes the central findings of the RMI and UCS reports which I cite in this article, or my central point which is that clean energy portfolios are now able to out-compete gas in many places on price alone while meeting the same grid needs. One thing to keep in mind about these portfolios is that they often incorporate multiple solutions and can have different portions of DSM, batteries, solar, wind, etc.