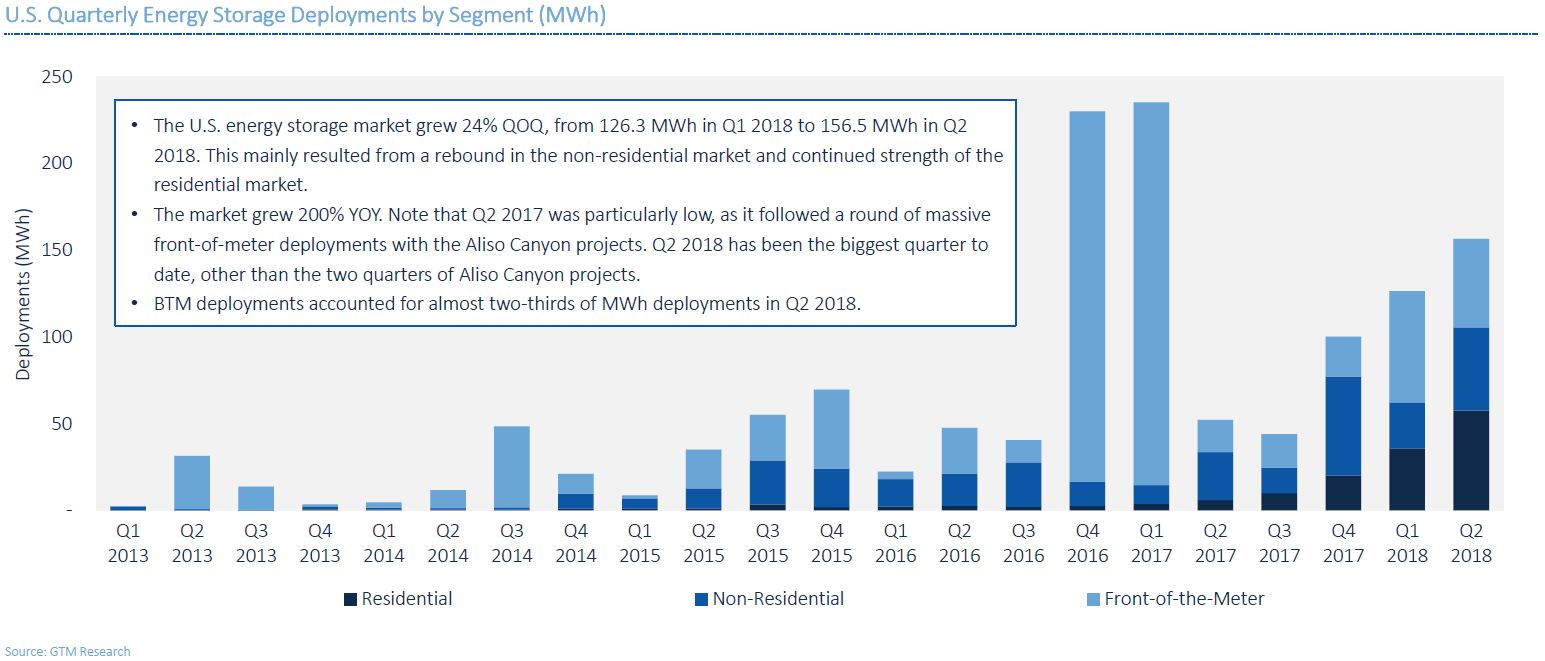

The headline for residential energy storage growth during Q2 is just as splashy as the 9X growth in the first quarter. Although this time we get overall market growth of 200%, a new “non-emergency” peak volume of installations, and relatively strong contributions from all three sectors.

The report, US Energy Storage Monitor, by Wood Mackenzie Power & Renewables shows 61.8 MW / 156.5 megawatt-hours (MWh) of energy storage deployed in the quarter, versus Q1 2018 which saw 43.6 MW / 126.3 MWh – growth of 42% and 24% quarter over quarter, respectively. Compared to Q2 2017, the growth rates were 60 and 200%, respectively.

The report notes that California and Hawaii dominate the residential market, and are expected to continue to do so, with 72% of all installations. However, Massachusetts and Arizona have a chance at making a move pending their own market adjustments.

The residential market has shown the most consistent growth of the three sectors, with positive quarter-over-quarter numbers since the beginning of 2017 – cumulatively experiencing 60.6% quarterly growth.

In fact, during this quarter residential was the leading sector in both MW and MWh installed. This aligns with prior research communicating 74% of residential customers have shown interest in energy storage.

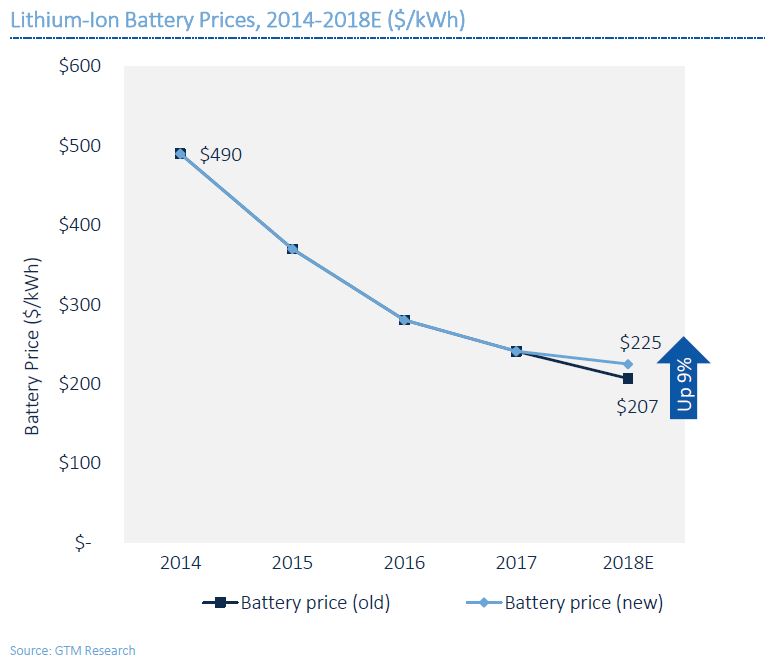

However, this growth is constrained by supply starting right about now, as evidenced by Tesla shutting down one Powerwall line for the Model 3, and Green Mountain Power still being short Powerwalls for their distributed power plant, and anecdotal evidence of the Sharp SmartStorage system having a six month wait. Wood Mackenzie expects the second half of the year to show flat growth relative to the first half of the year in the residential market due to these supply constraints.

These supply constraints are also slowing down declines in the cost of energy storage. While it was initially expected that battery prices would fall 14%, Wood Mackenzie has revised its outlook and now expects only 5% decrease in prices this year.

Commercial and utility scale installation volumes are more uneven from quarter to quarter, with fewer numbers are larger installations, representing a less mature market.

Wood Mackenzie projects that 393 MW / 774 MWh of energy storage will be installed in 2018, growing to 3,890 MW / 11,700 MWh in 2023.

There are breadcrumbs that Wood’s aggressive growth projections are on track. PG&E recently signed a series of projects larger than all of 2018’s projected installation volumes, Tesla is projecting ‘mad growth‘ (though globally, not just USA) of 300-400% in 2018 AND 2019.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

But more battery factories coming … https://www.bloomberg.com/news/articles/2017-06-28/china-is-about-to-bury-elon-musk-in-batteries