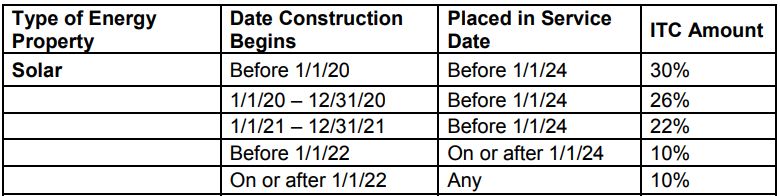

For all practical purposes, medium- and large-scale solar power projects that expect to take a year to two (or more) for development and construction just got a two year extension on the Investment Tax Credit (ITC).

Per the ‘Bipartisan Budget Act of 2018, Pub. L. 115-123, Div. D, Title I, § 40411, 132 Stat. 150 (BBA 2018)‘, and published in Notice 2018-59, the Internal Revenue Service (IRS) has officially noted that it is “replacing the requirement to place energy property in service by a certain date with a requirement to begin construction by a certain later date.”

Meaning that instead of your solar project having to finish by December 31st, 2019, it must now begin (defined below in two specific ways) on or by that date t0 qualify for 30%. This same logic applies to the follow two years and their 26% and 22% tax credits.

The IRS notes that there are two methods for ‘establishing beginning of construction’ – the Physical Work Test or the Five Percent Safe Harbor.

Onsite physical work can take many forms, however, it does include any of the following “preliminary activities”:

(a) planning or designing; (b) securing financing; (c) exploring; (d) researching; (e) conducting mapping and modeling to assess a resource; (f) obtaining permits and licenses; (g) conducting geophysical, gravity, magnetic, seismic and resistivity surveys; (h) conducting environmental and engineering studies

It is notable that manufacturing of hardware necessary to the project that is done off-site counts toward physical work, including assembly of “racks and rails, inverters, and transformers.” However, if those components come from inventory or are normally held in inventory, then they aren’t allowed to be considered “physical work.”

The Five Percent Safe Harbor provision states that construction will be considered as having begun if the taxpayer has paid or incurred – per Treas. Reg. § 1.461-1(a) – 5% of more of the total cost of the project. This does not include land costs.

Keith Martin of Norton Rose Fulbright notes that an equipment or service purchase – a ‘bare payment’ alone – can account for the 5% rule if it is delivered within 31/2 months.

Once work begins, it must keep going – meeting a continuity requirement.

Real world consequences

Also noted by Martin, is that the IRS guidance is not addressed to the directly owned residential solar power market – as this is the corporate focused Investment Tax Credit, and not the Residential Renewable Energy Tax Credit. However, it does apply to third party owned residential solar systems that solar companies lease or use to sell electricity to homeowners.

In the larger commercial and utility scale projects this ruling will absolutely be put into the spreadsheets of financiers at the utilities, which have explicitly stated these solar power tax benefits are driving their decision-making. For instance, in Xcel Energy’s recent long-term plan – which included solar power bids as low as 2.2¢/kWh – the company stated:

Bidders’ ability to take full advantage of the full federal PTC and ITC combined with falling costs for renewable technologies resulted in a robust pool of wind, solar with battery, and solar bids at unprecedented pricing.

This two year window will give investors and utilities reasonable motivation to invest in more projects, even as end of year dates arrive. And this in turn can have repercussions for fossil generation, as Xcel noted that this would allow it to close two coal plants a decade early.

Conversely, there could also be projects whose timelines are extended. For instance, the above Xcel Energy projects could potentially be pushed back up to two years under the expectation of continued declines in hardware pricing for solar panels, batteries and other components.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

Among peers, there is confusion on the time frame the I.R.S. allows a home owner, business owner, Investor, etc., to use the 30% Federal Tax Credit? Do they have 5 years to use the Tax Credit? Do they have 2 years to use the Tax Credit?

How long from install does the owner have to use the 30% Federal Tax Credit?

A link to accurate I.R.S. verdict is appreciated, thank you!

source: https://news.energysage.com/investment-tax-credit-rooftop-solar-happens-dont-enough-tax-liability/

Can the solar ITC carry forward if my tax bill is smaller than my tax credit amount?

Using the example of the $10,000 solar system from above, the ITC amount you would be eligible for is $3,000. But what if your total tax liability for that year is only $2,000? Can you carry over the remaining $1,000 to the next year?

It is fairly clear in form 5659 that, yes, you are allowed to carry unused credits forward into the next year (see lines 12-16 of the form) – and possibly beyond. This means that your tax liability for year 1 would fall to $0, and you would have an additional $1,000 of credit to put towards the following year’s tax bills.

However, it is yet unclear whether you will be able to carry unclaimed credits in the years after the ITC is discontinued.

ITC three scenarios

Figure 1: Comparing how the ITC would apply in three tax liability scenarios: a) $5,000 annual tax liability, b) $2,000 annual tax liability and c) $0 annual tax liability. For simplicity’s sake, we assume that the solar system costs $10,000, making the ITC amount would be $3,000. In scenarios a) and b), the ITC benefits are applied over 1 and 2 years, respectively. In scenario c) the ITC cannot be claimed due to insufficient tax liability (meaning that a solar lease might be a preferable option to purchase).

Interesting law language: https://www.law.cornell.edu/uscode/text/26/39

(a) In general

(1) 1-year carryback and 20-year carryforwardIf the sum of the business credit carryforwards to the taxable year plus the amount of the current year business credit for the taxable year exceeds the amount of the limitation imposed by subsection (c) of section 38 for such taxable year (hereinafter in this section referred to as the “unused credit year”), such excess (to the extent attributable to the amount of the current year business credit) shall be—

(A) a business credit carryback to the taxable year preceding the unused credit year, and

(B) a business credit carryforward to each of the 20 taxable years following the unused credit year,

and, subject to the limitations imposed by subsections (b) and (c), shall be taken into account under the provisions of section 38(a) in the manner provided in section 38(a).

And that cornell page linked to this document, which seems to apply:

https://www.irs.gov/pub/irs-wd/201548006.pdf

Why are they allowing business to do this but not also giving it to individuals who get solar on their roof? Seems like a double standard.

Does this info still stand with the IRS in regards to the definition of “establishing beginning of construction?”

Yes

the recapture of solar energy credit/ does this only apply to commercial projects (if you sell the property before the end of 5 years)?

In some reading the recapture does not apply to the residential solar energy credit?