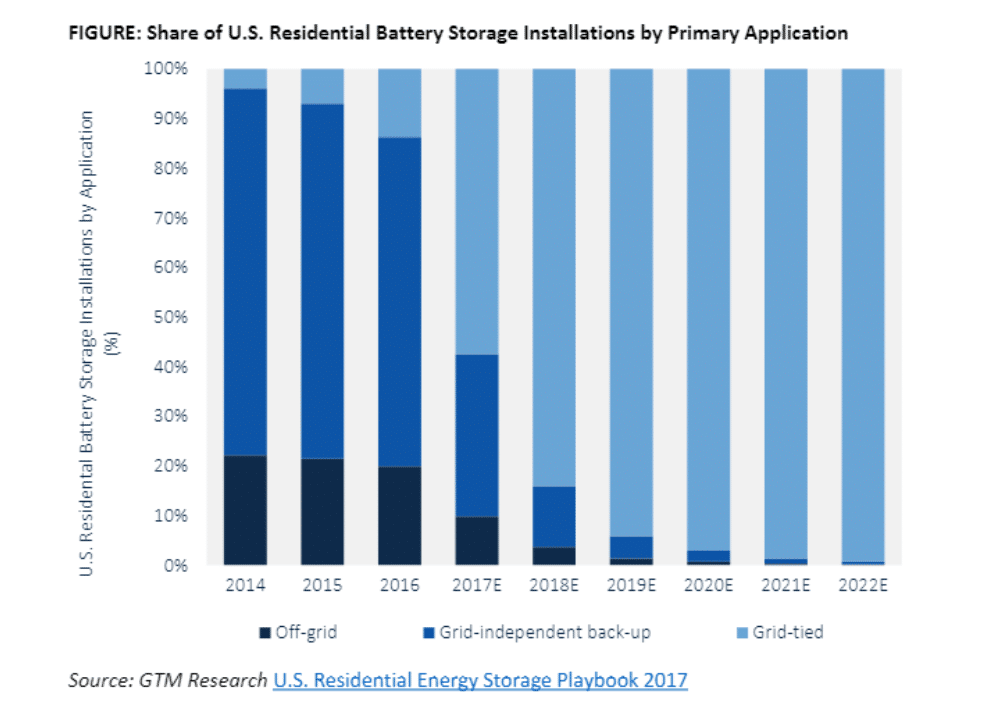

Until 2017, most residential battery storage systems were installed off the grid. However, GTM Research says 2017 is the year that changes, and changes dramatically.

If GTM’s new report – The Residential Battery Storage Playbook 2017 – is correct, installations of grid-tied residential batter storage systems will surpass off-grid and grid independent ones for the first time.

Though GTM admits that it’s hard to count off-grid and grid-independent installations because of the nature of the deployments, their best estimate is that 4,400 residential battery systems were deployed in 2016, with 86% of them being off-grid or grid-independent.

The latest numbers on 2017, however, suggest a reversal of that trend. Instead, the report predicts 57% of 2017’s deployments will be grid-connected, with the percentage increasing to 99% by 2022. With a huge growth in the grid-tied segment, off-grid and grid-independent installations are expected to remain relatively flat.

“It is most instructive to think of the residential battery market not as a monolithic entity, but rather a patchwork quilt of geography and homeowner-specific applications that will be stitched together over time,” write the authors of the report. “Each application lends itself to a specific set of system requirements, which may potentially overlap with the requirements for other applications.”

“Further complicating the matter, homeowner preferences and site-specific constraints may alter or limit what can be achieved by a given system,” they continued.

Currently, only a few markets like Hawaii, California and some northeastern states have the right mix of applications and regulations to fuel a battery storage revolution, but GTM expects falling prices and rate design (among other factors) will drive significant market expansion.

“The underlying drivers of product-market fit, and hence industry growth, point toward a robust future outlook for residential battery storage,” write the authors. “The market has the potential to dramatically evolve over time, and industry stakeholders can drive that evolution through technology, product and regulatory efforts.”

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

A typical off-grid installation is still going to need more kWh of storage per kWh of demand compared to a grid-tied system. In the long term, this doesn’t matter since it looks like grid-tied systems are going to take off so fast, the off-grid numbers will fade into background noise before 2020. But for 2017 numbers, kWh of demand might still be dominated by off-grid numbers, meaning PbA batteries are getting their last hurrah before tumbling into that dark, acidic night.

Utilities aren’t going to sit idly by while a grid-tied storage revolution is happening under their feet. Their efforts to hobble distributed solar PV will come back to bite them as it drives more customers towards on-site storage. Given lax or even paid-off state regulators, we might start seeing steep fees applied to grid tied storage as well. If this happens, there might be a large increase in people defecting from the grid entirely. Only local jurisdiction laws mandating an active grid connection will stem the flow.

This will only happen if utilities maintain an adversarial relationship with distributed solar and storage. If their incentives are aligned more towards fostering solar and storage, there can be many win-win scenarios for all parties involved. Regulators just need to ensure those incentives are changed to turn utilities in the right direction.