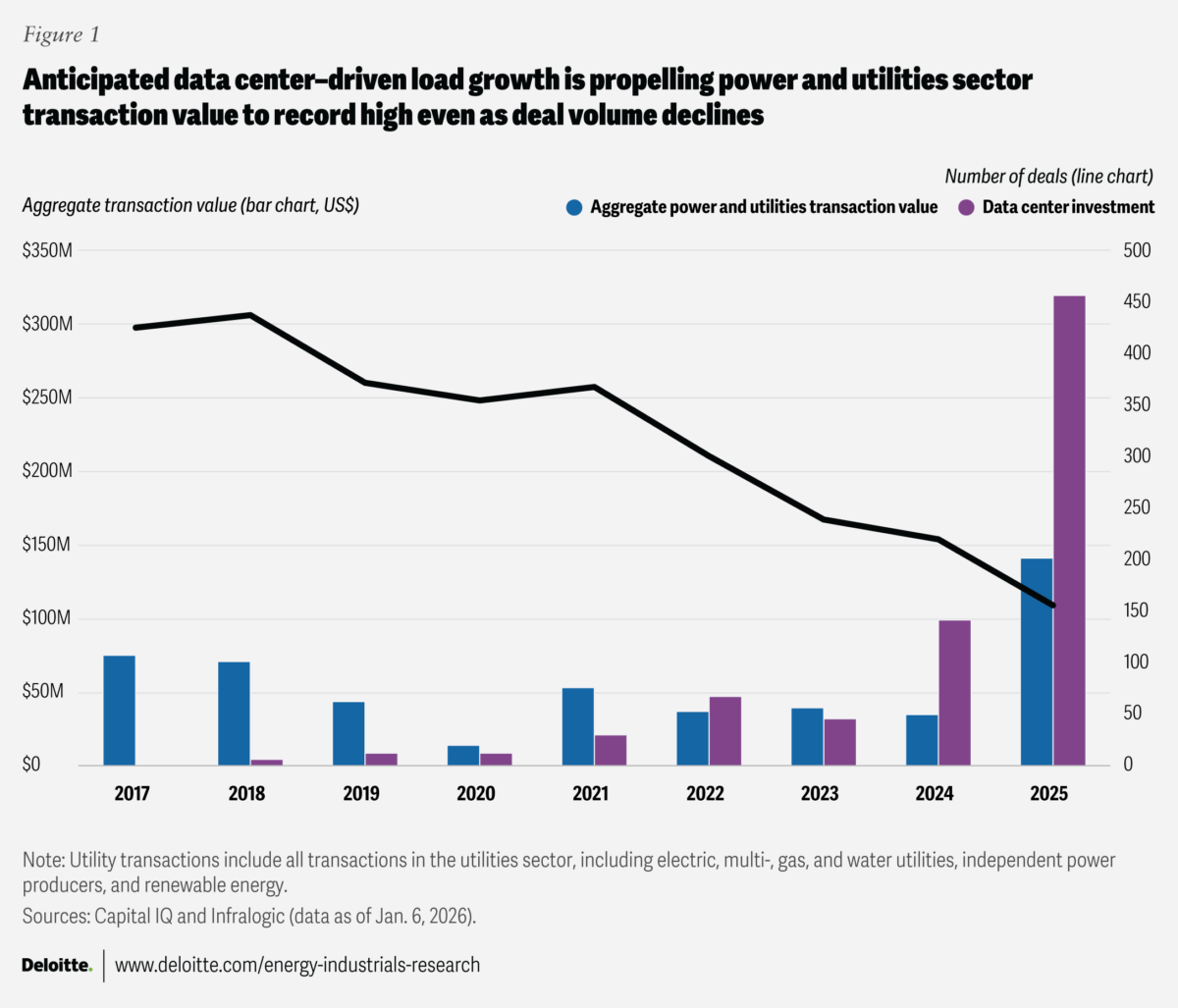

The solar and energy storage sectors are emerging as a bright spot in the U.S. power and utilities mergers and acquisitions (M&A) landscape. According to a report from Deloitte, the hunt for “scale at speed” to meet the energy demands of AI is reshaping how assets are bought and sold.

While wind energy acquisitions have faced a downturn, solar and storage activity has increased, more than offsetting those declines. This shift reflects a market that is moving away from speculative, early-stage project grabs and toward “de-risked” assets that can provide firm capacity to a tightening grid.

“Buyers appear to be favoring solar-paired storage and multi-market exposure as tools to manage nodal, congestion, and regulatory risks,” said the Deloitte report. “This preference is likely reinforcing the demand for de-risked assets with firm interconnection positions.”

The report highlights a significant trend toward solar-plus-storage portfolios. As the U.S. grid faces unprecedented pressure from AI data center growth, the ability to provide reliable, dispatchable power has become a premium commodity.

This has led to a “laser focus” on late-stage projects. Developers are increasingly rotating capital by monetizing mature projects—often those supported by long-term power purchase agreements (PPAs)—to fund the next generation of their development pipelines. In 2025, this “developer capital rotation” accounted for 21% of all renewable asset deal volume.

The bankability of these deals is also being bolstered by large tech companies like Google, Microsoft, and Amazon whose offtake agreements provide the financing certainty needed in a higher-interest-rate environment.

The U.S. solar sector remains highly fragmented, with over 1,500 owners across 152 GW of operating capacity. Deloitte said this creates a massive opportunity for strategic “roll-ups” by utilities, independent power producers (IPPs), and infrastructure investors looking to achieve vertical integration.

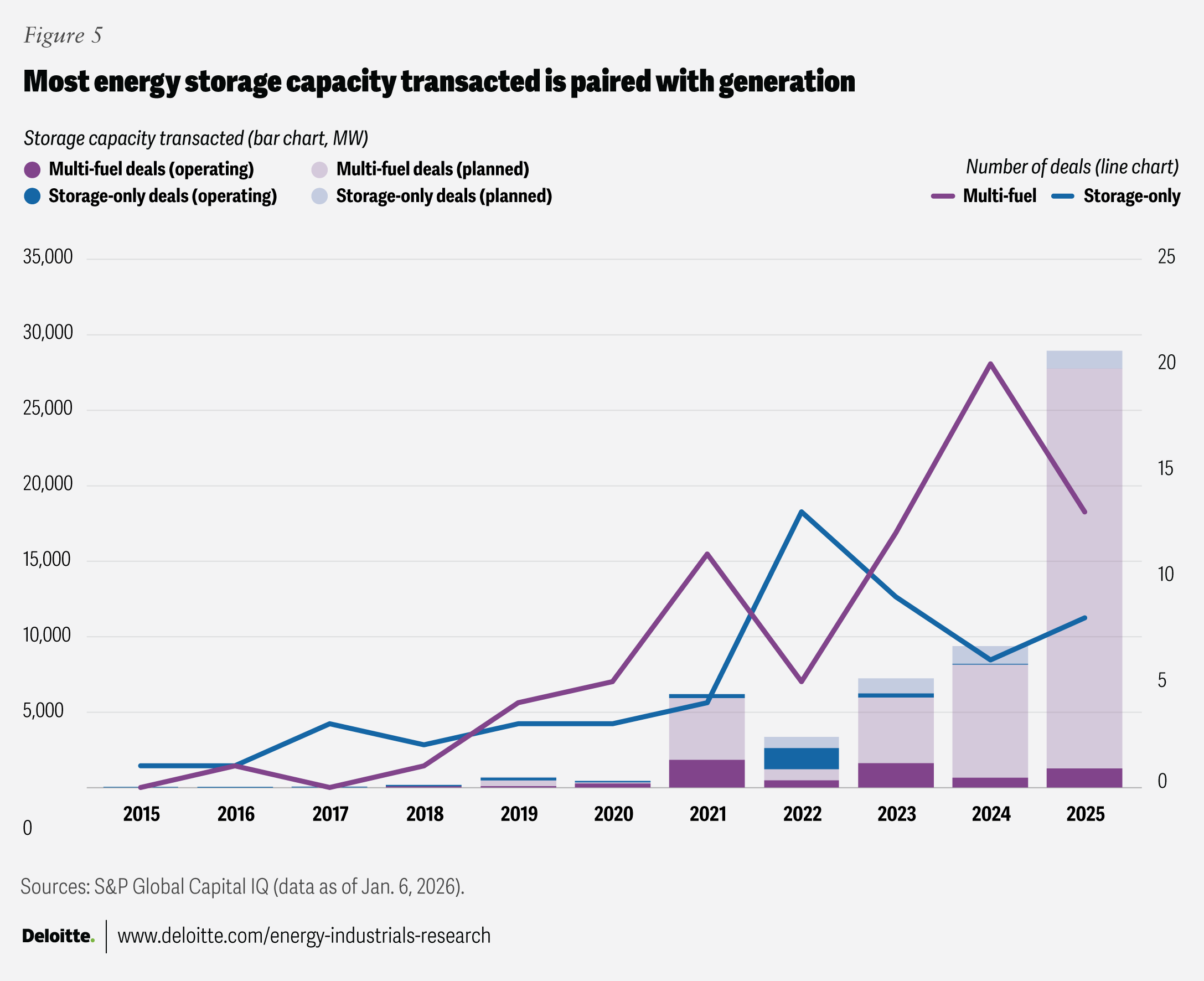

The report also highlights increasing M&A activity in the battery storage sector, where firms are acquiring everything from raw materials to asset management software to secure their supply chains and capture higher margins.

Despite the momentum, the market is navigating a complex regulatory environment. Tax credit transferability and safe-harbor rules continue to dictate the timing and valuation of transactions. While uncertainty around corporate tax liability softened pricing for some 2025 Investment Tax Credits (ITC) in late 2024, the fundamental drivers remain strong. The push for decarbonization, coupled with the urgent need for energy security, continues to keep solar and storage at the forefront of the energy transition.

According to data from the Energy Information Administration, solar, batteries, and wind are expected to make up 93% of all U.S. capacity deployments in 2025.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.