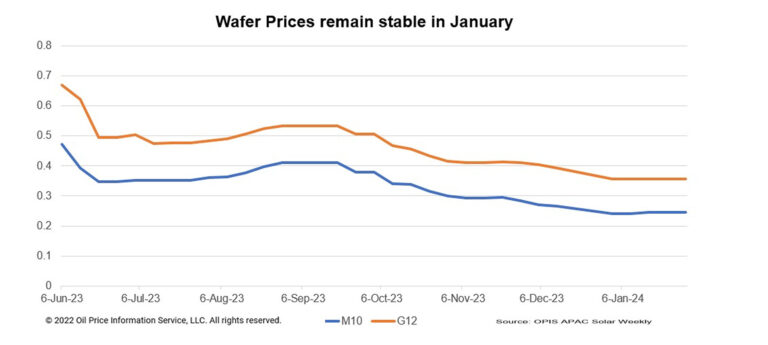

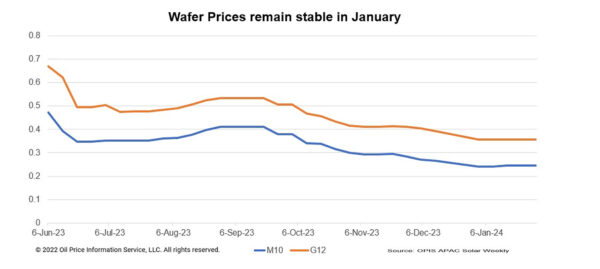

Wafer FOB China prices have stayed consistent for the third consecutive week due to a lack of significant changes in the market fundamentals. Mono PERC M10 and G12 wafer prices remain steady at $0.246 per piece (pc) and $0.357/pc, respectively.

Cell manufacturers who intend to keep up production throughout the Chinese New Year break have started to accumulate raw materials, which has increased the volume of wafers traded. The amount of wafers produced and in stock is adequate to meet downstream demand, momentarily dashing wafer makers’ expectations of additional price increases.

Divergent views exist regarding the near-term outlook for wafer prices in the marketplace. According to a market observer, polysilicon companies appear to be banding together to drive up polysilicon prices perhaps as a result of the relative scarcity of N-type polysilicon. This foundation may lead to an increase in wafer pricing, the source said, adding that wafer makers may boost prices even if demand does not recover in the near future because of manufacturing cost considerations.

On the other hand, a downstream market participant believes that there aren’t enough fundamental prerequisites for price hikes in the supply chain market as a whole due to the oversupply of upstream materials. The polysilicon production output in January is expected to be equivalent to about 70 GW of downstream products, significantly greater than the module’s January production output of roughly 40 GW, according to this source.

OPIS learned that only the major cell producers will continue regular production throughout the Chinese New Year break, with nearly half of the existing cell capacity in the market suspending production during the holiday.

The wafer segment is expected to reduce plant operating rates during Chinese New Year but is less evident as compared to the cell segment, resulting in higher wafer inventories in February that may exert downward pressure on wafer pricing in the coming weeks.

OPIS, a Dow Jones company, provides energy prices, news, data, and analysis on gasoline, diesel, jet fuel, LPG/NGL, coal, metals, and chemicals, as well as renewable fuels and environmental commodities. It acquired pricing data assets from Singapore Solar Exchange in 2022 and now publishes the OPIS APAC Solar Weekly Report.

The views and opinions expressed in this article are the author’s own, and do not necessarily reflect those held by pv magazine.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.