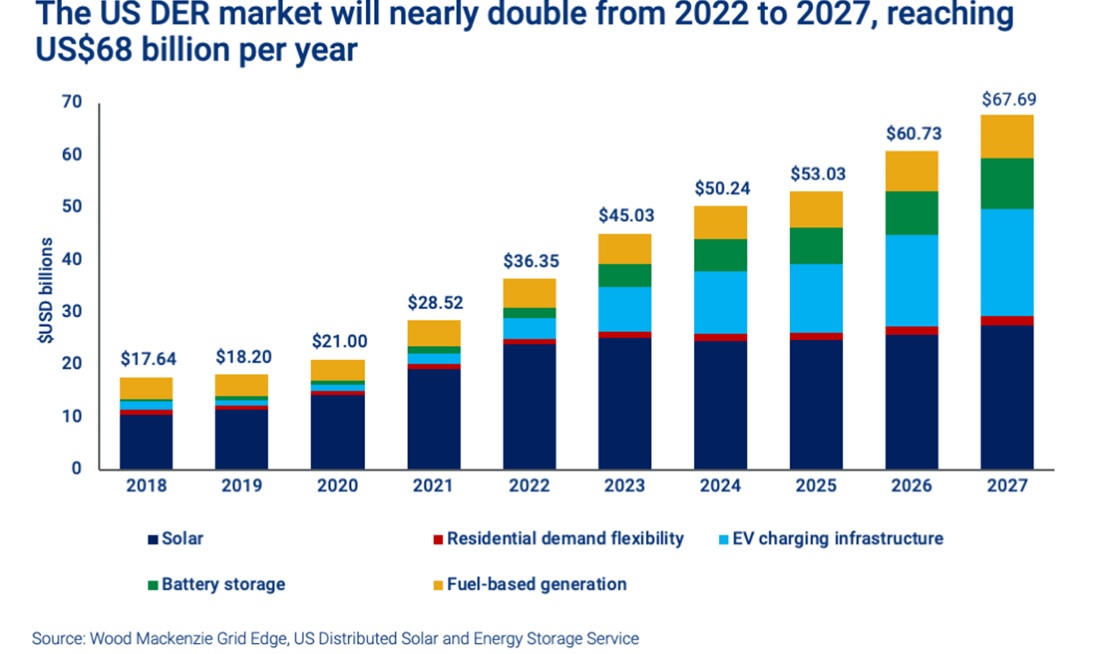

The 2023 US Distributed Energy Resource Outlook recently released by Wood Mackenzie indicates that the U.S. market will nearly double between 2022 and 2027, to reach almost $68 billion per year.

Behind-the-meter capacity will grow 3.7 times more over this period than it did in the previous five years, according to the report. But perhaps the most significant market change is that the electric vehicle (EV) charging infrastructure is responsible for much of that growth.

The distributed energy resources (DER) covered in the report include EV chargers; distributed storage, solar and fuel-based generation; and residential and non-residential demand flexibility.

For this report, Wood Mackenzie defines DERs as:

- Customer-sited – Resources located physically on a customer premise, whether that premise is interconnected at the distribution or transmission level. Community-owned assets on the distribution system are also included.

- Primary use – No maximum MW capacity is applied, but we enforce a primary use restriction, under which, to be included, a resource must serve or control a customer(s)’ local load for electricity and, potentially, heat. Community-owned assets are considered as satisfying.

- Embodiment – A DER must be embodied as a physical asset, whose primary purpose is energy management. Flexibility in customer energy demand, including the willingness to raise temperature setpoints or shut down production lines, is not considered a DER.

- Voltage – A voltage restriction of 69 kV is used for non-CHP generators. This includes all EV infrastructure deployments, which are connected at distribution grid voltages.

Wood Mackenzie analysis shows that 262 GW of new DER and demand flexibility capacity will be installed from 2023 to 2027, nearly matching the 272 GW of utility-scale resource installations also expected during that period.

For the first time, EV charger annual installed capacity will overtake distributed solar and will reach 3.5x solar annual additions by 2027. This market is expected to reach $20 billion by 2027, led by the residential Level 2 ($6.5 billion) and public DC fast chargers ($5.6 billion) segments. Residential charging capacity still holds the majority but will decrease due to infrastructure for buses and trucks reaching 18% of total charging capacity by 2027.

Policies that are driving the growth are federal incentives, not the least of which are the Inflation Reduction Act tax credits along with the National Electric Vehicle Infrastructure Grant program, expected to drive public charger growth along highway corridors. Also driving the growth is grid insecurity of homeowners and businesses owners, which the report says will cause the distributed fuel-based generation market to grow 240% from 2022 to 2027 and the distributed storage market to grow 460%, with storage reaching nearly $10 billion per year.

“Federal incentives, headlined by the Inflation Reduction Act tax credits and National Electric Vehicle Infrastructure grant program, represent the greatest catalysts for growth in the US DER market. Continued failure of system operators to reduce the time and cost of interconnection would be a tailwind, forcing utilities and corporates to look to distributed resources to achieve reliability and clean energy goals,” said Ben Hertz-Shargel, lead author of the report and global head of Grid Edge at Wood Mackenzie.

Another driver is the California NEM 3.0, which initially will cause an estimate 38% contraction of the market in 2024, but then will significantly increase storage attachment rates going forward.

Despite a price decline of 13% over the next five years, distributed solar will still represent 46% of DER capital expenditure through 2027.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.