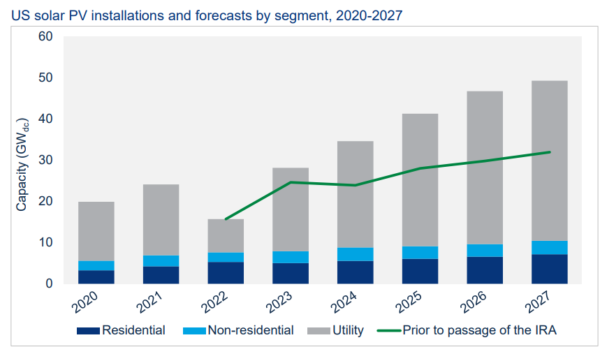

After a hampered start to the year, the United States is set to grow its solar capacity at unprecedented rates. Now that the Inflation Reduction Act (IRA) has been passed, the Solar Energy Industries Association (SEIA) and Wood Mackenzie have lifted the forecast for solar deployment by 40% above prior projections through 2027.

According to the two organizations in the U.S. Solar Market Insight Q3 2022, installed and operational solar capacity may increase threefold in five short years, skyrocketing from 129 GW today to 335 GW by 2027.

Despite this rapid growth, projections for this year have been trimmed to 15.7 GW due to lingering effects of the Department of Commerce’s investigation into antidumping violations by major international solar panel providers. Ongoing international trade and labor concerns, including the Uyghur Forced Labor Prevention Act (UFLPA) may continue to challenge supply and limit deployment in 2023. Full benefits of the IRA may not be reflected in deployment until 2024 at earliest, said the report.

Solar accounted for 39% of all new electric generating capacity additions in the first half of 2022. The U.S. solar market now represents about 4.5% of the nation’s electricity mix. Perhaps the most significant development in the Inflation Reduction Act for the solar industry was the long-term extension of the Investment Tax Credit (ITC) at 30%.

“The Inflation Reduction Act has given the solar industry the most long-term certainty it has ever had,” said Michelle Davis, principal analyst at Wood Mackenzie and lead author of the report. “Ten years of investment tax credits stands in stark contrast to the one-, two-, or five-year extensions that the industry has experienced in the last decade. It’s not an overstatement to say that the IRA will lead to a new era for the U.S. solar industry.”

For the fifth quarter in a row, residential solar had record deployment with 1.36 GW installed, a 37% increase over Q2 2021. This represents nearly 180,000 residential customers installing solar in one quarter. The report said customer demand was strong due in part to power outages and to power price increases. Residential solar installations may drop slightly next year as California’s NEM 3.0 policy takes effect.

Commercial solar installed 336 MW in Q2, down 7% year-over-year, while 2.7 GW of utility-scale solar was deployed in Q2, a 25% decrease from Q2 2021. The extension and expansion of the ITC and other provisions in the IRA boosted Wood Mackenzie’s five-year outlook by 52 GW (47%) over previous projections.

Community solar deployment projects were lifted by 18% compared to the previous outlook. President Biden’s Executive Order has brought relief to the industry, but most of the additions come from Maine and New York. The two states accounted for 72% of the community solar capacity additions in the first half of 2022. In Maine, Net Energy Billing (NEB) projects that are not wrapped up in the state’s interconnection studies are coming online at a fast pace. In New York, Community Adder projects continue to come online, with a healthy pipeline remaining.

System prices continued to climb in Q2 2022 across market segments, mostly due to module price increases. System pricing increased year-over-year by 9% for residential, 8% for commercial, 8% for utility fixed-tilt, and 13% for utility single-axis tracking solar projects.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

Puerto Rico tiene el más elevado costo en energía de todo los Estados Unidos . Pero el desarrollo de la energía Solar va a paso lento.

re: “Residential solar installations may drop slightly next year as California’s NEM 3.0 policy takes effect.” Depending on the NEM 3.0 final decision, that “slightly” could easily become a “massive drop off”. Down playing the potential impacts of an adverse NEM 3.0 decision is just plain poor analysis and reporting. This is the key issue facing the US Solar market today and it is being largely ignored or down played by most market projections. The CA solar market is the major part of the US market and customer owned DGPV is nearly half of the solar going in in CA.

As important as the California segment of the US solar market is, bear in mind it is 10% of the market, If NEM 3.0 were to hobble California, one has to ask if it is total or partial. My bet that it is partial and it would likely be analogous to the situation in Germany 10 years ago with the phase out of Feed In Tariff support. German installations slowed but never stopped. Similarly, California will still have business cases that are not marginal and will proceed anyway. Worst case would less than 50% ?decline in the California installations. In the meantime, the rest of the nation will be expanding so the net loss to the industry as a whole will be negligible. This is not to say there will be serious disruption on the ground in California. Many installers and distributers will have to either move or adapt or shut down which is unfortunate.