It’s solar earnings season and there’s a clear, non-surprising theme: The first quarter was strong and largely unimpacted by the pandemic, but the second quarter and 2020 as a whole is uncertain.

We’ve already heard that story this week from Sunrun, Enphase, SolarEdge, First Solar and now its SunPower’s turn.

In SunPower’s case, the company had “solid first quarter execution,” according to CEO Tom Werner who sees hope for May and June — after a harrowing April.

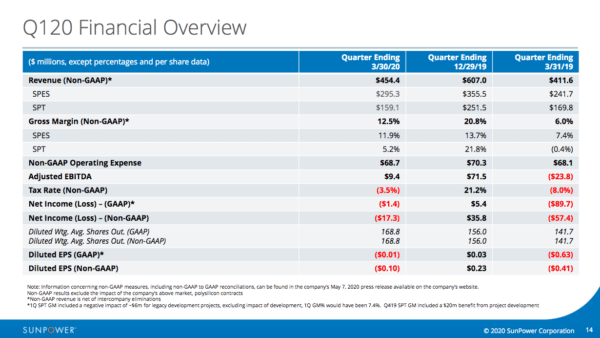

Financial highlights from the solar manufacturer’s first quarter:

- Quarterly revenue of $454.4 million, down from the previous quarter’s $607 million

- Net loss of $1.4 million

- 50% year-over-year volume growth in distributed generation demand

- Expected profitability for commercial segment in second half 2020

- Spin-off of Maxeon Solar expected for Q2 of 2020, pending regulatory approvalh

- New homes backlog >45,000 homes

“We had a strong start to the year, exceeding our margin and adjusted EBITDA guidance,” said Tom Werner, SunPower CEO. “However, we have seen a material impact across the industry and our business, caused by the Covid-19 virus pandemic during the second quarter.”

Demand for the company’s storage product “remains strong with a pipeline exceeding $320 million and attach rates in excess of 30%. In particular, we are seeing significant traction for storage in California’s innovative self-generation incentive program, driven by strong customer interest in resiliency.”

SunPower Technologies, the international portion of which will soon be Maxeon Solar Technologies, saw year-on-year shipment growth of 29%.

Werner said, “We expect our remaining facilities to resume production in the coming weeks and expect to have sufficient existing inventory to meet our commitments for the second quarter.”

Guidance for Q2 but not for 2020

SunPower is not providing fiscal year 2020 guidance at this time, but guided for next quarter.

- GAAP revenue of $290 million to $330 million

- Gross margin of -9% to -3%

- Net loss of $120 million to $100 million.

- MW deployed in the range of 340 MW to 400 MW.

- The company expects Q2 2020 Adjusted EBITDA guidance in the range of –$40 million to –$20 million

SunPower has put cost saving measures into place that will save a claimed $100 million and has “identified up to $500 million in potential liquidity over the next 12 months, including our $55 million revolver which remains undrawn.”

Shifts at SunPower

Late last year, SunPower announced it would be spinning off its high-efficiency manufacturing business into a new company, Maxeon Solar Technologies. Maxeon products have historically led the industry as the world’s highest-efficiency solar modules. Tianjin Zhonghuan Semiconductor, one of the world’s largest silicon wafer makers, is putting $298 million into Maxeon Solar.

SunPower just entered a $1 billion partnership with Tech CU that gives the solar panel efficiency leader access to a significant chunk of capital for its loan program. The new partnership provides financing opportunities for potential U.S. residential solar and storage customers.

Last month, the company offered “zero money down” promotions that can reduce the upfront costs of going solar for U.S. customers.

SunPower recently announced that it is temporarily cutting executive pay, reducing the workweek for some employees, and that it has already idled its factories in the U.S., France, Malaysia, Mexico, and the Philippines in response to the impact of Covid-19.

SunPower has more than 8,000 full-time employees worldwide, of which about 2,000 are in the U.S.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

Mr. WESOFF, please do something never done by anyone before: speak well of SUNPOWER! It is the most popular game in recent years, among the various financial gurus: who speaks worse around the SUNPOWER? There is no one who sees beyond …. or rather no one sees better what there is to see. If a quarter is fine for SUNPOWER … comparisons are made with the quarter that went better … to say that things are not going as hoped. If the quarter went worse …. ok … that’s it. I don’t know why this race has been going on for years, above all I don’t understand who benefits this massacre of the American company that produces the best photovoltaic panels in the world. I would have an answer: HEDGE funds! Those who hunt for troubled companies and ruin them as reputation even if they make huge efforts to get back on top. The American stock exchange allows hedge funds to destroy companies that are worth, and to enhance companies that are worth less than zero! But I think this game of massacre … is about to end: the listing of MAXEON SOLAR TECNOLOGIES will blow up the structure of well-organized disinformation in the USA. The CHINESE shareholder will know how to protect his investments well and indeed will increase them … and the FRENCH shareholder TOTAL will be able to see absolutely unexpected NEW SUNPOWER quotations, because they are cleaned of the problem of the cost of polysilicon (paid too much compared to market prices). Please make a difference, look far … beyond … the cold quarterly result and give concrete indications on the future of a company that perhaps should have remained entirely American, but that the US government has always neglected … leaving that competition took it away.Cordially.