Fitch Ratings has given Topaz Solar Farms, LLC’s $1.1 billion ($857.4 million outstanding) senior secured notes a “C” rating.

The Fitch Ratings glossary defines a “C” rating as “exceptionally high levels of credit risk” meaning “default is imminent or inevitable, or the issuer is in standstill.”

The credit rating of the Topaz project has been at “C” for more than year — because of the looming liability of having a bankrupt offtaker, PG&E — although the utility could emerge from chapter 11 in June of this year, pending a decision from the California Public Utility Commission.

In the meantime, the ratings document affords some insight into mega-project performance.

History of Topaz

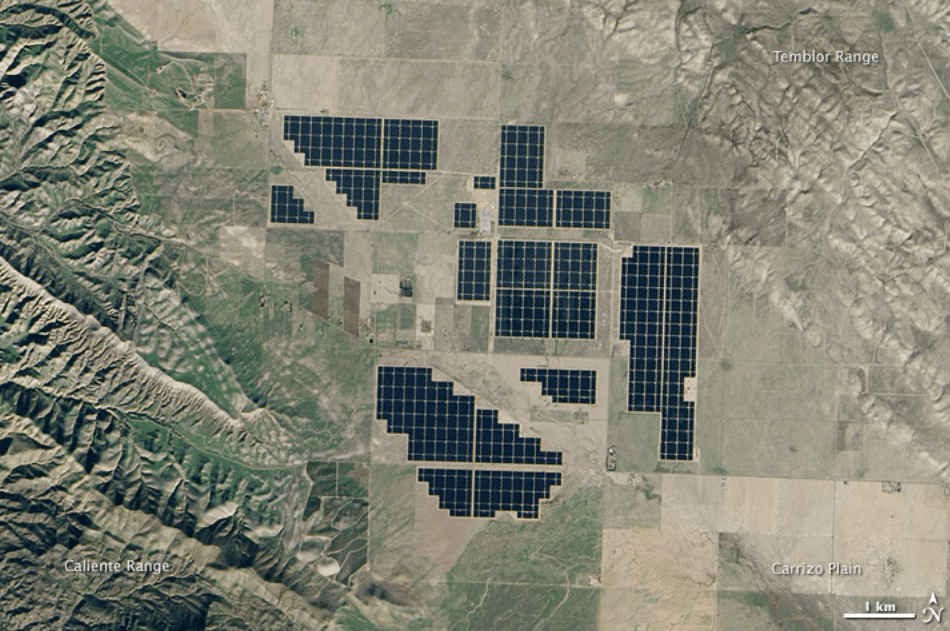

In 2014, the 550 MW Topaz Solar project achieved full commercial operation and, for a while, was the largest solar plant on-line in the world. PG&E purchases the electricity from the Topaz project under a 25-year fixed price power purchase agreement.

First Solar installed more than nine million thin-film cadmium-telluride solar panels at a fixed tilt of 25-degrees across 9.5 square miles of disturbed farmland in San Luis Obispo County on California’s Carrizo Plain. Construction of the MidAmerican Solar-owned project began in 2011. First Solar continues to operate and maintain the plant.

Followers of ancient history will recall that this project was originated by OptiSolar in the aughts and that some of the Topaz real estate was once intended for an Ausra CSP solar power plant.

Project performance details

According to the ratings document, Topaz’s “very stable” operational performance “has exceeded the base case forecasts for over four years of commercial operating history and exhibits healthy financial metrics, with modest leverage and strengthening debt service coverage ratios.”

According to the Fitch document, in 2019:

- Actual output from Topaz was 103% of the P50 forecast and above Fitch’s base case.

- Availability was steady at 99% (compared to Fitch’s base case estimate of 97%).

- Energy lost due to maintenance and soiling did not impact operations significantly.

- PG&E-directed curtailment was ~11,600 MWh in 2019 — less than 1% of generation.

- Topaz is not undergoing adverse impacts to operations or staffing due to the coronavirus.

Fitch’s base case utilizes the P50 electric generation estimate, 97% availability, 0.9% annual panel degradation, a 2% energy output reduction, and a 2% inflation assumption.

Financial performance details

The Topaz plant had strong performance in 2019.

- The plant posted $199.2 million in revenue in 2019, down 10% from 2018 due to lower insolation and other factors, according to unaudited financial data.

- Cash flow available for debt service decreased from $210.4 million in 2018 to $178.5 million in 2019.

- PG&E has been current on all PPA payments with Topaz since filing for bankruptcy protection in January 2019.

Fitch admits that the “metrics are consistent with a strong investment grade profile” but the project rating “reflects Topaz’s exposure to a bankrupt utility counterparty” for all of its revenue under a long-term PPA.

Upgrading the rating?

The rating of this project will get a boost if and when PG&E emerges from bankruptcy. The Topaz PPA represents a significant portion of PG&E’s contracted capacity and is expected to be included under the reorganization plan.

The CPUC will vote on the proposed bankruptcy decision on May 21. PG&E will have access to a $21 billion wildfire insurance fund if it emerges from bankruptcy by June 30.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

Seems to say more about PG&E than utility scale solar. Something good has to emerge out of the bankruptcy of PG&E because the grid must go on.

By Fitches’ own numbers: “According to the Fitch document, in 2019:

Actual output from Topaz was 103% of the P50 forecast and above Fitch’s base case.

Availability was steady at 99% (compared to Fitch’s base case estimate of 97%).

Energy lost due to maintenance and soiling did not impact operations significantly.

PG&E-directed curtailment was ~11,600 MWh in 2019 — less than 1% of generation.

Topaz is not undergoing adverse impacts to operations or staffing due to the coronavirus.”

Point 4 of approximately 11.6GWh of electricity “thrown away” is less than 1% of generation. But what is the actual (value) of being able to store this non-fueled power stored to use during the expensive TOU rate spiking time of the day? Just a lousy 150MWh energy storage system could have made a big difference in supplying stacked grid services into this one asset. Now technology is bring forth electronic switching inverters that can “reform” the grid and act like a large mechanical generation site to keep the grid from oscillation and react to grid demands in the millisecond to seconds time frame. It’s sounding like Topaz solar farm needs to shed PG&E to get on with its life and multi-year operations prospects.