As California goes, so goes…the world?

Earth’s 5th largest economy has put forth its 2019-2020 Integrated Resource Plan (IRP) – Proposed Reference System Plan (173 page pdf), and it suggests that solar and energy storage will “dominate” through 2030 and beyond. The purpose of the document is to lay a path, based on hard research of both costs and technical feasibility, to move the state toward 100% renewable electricity and, net negative CO2 by 2045.

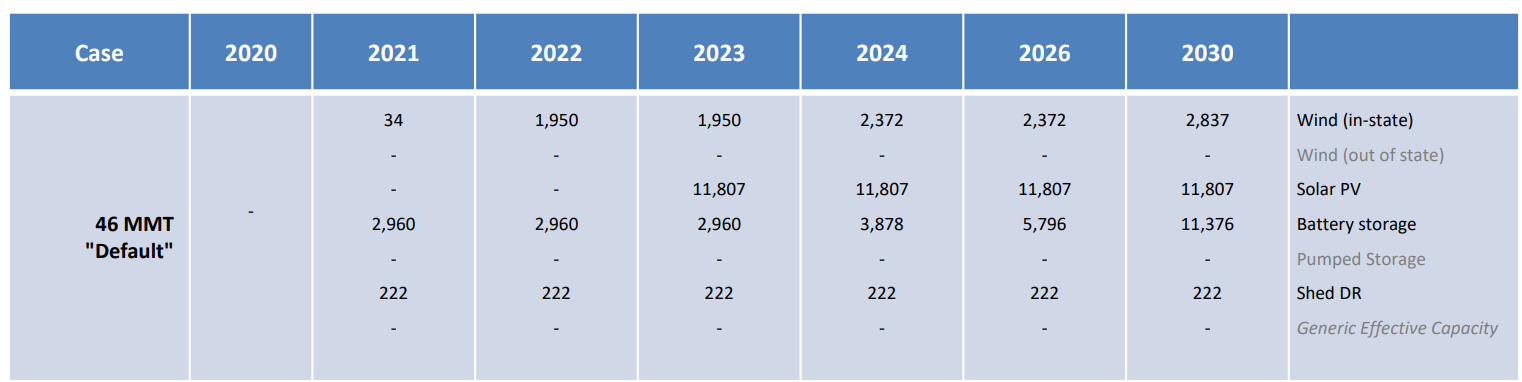

On the slide titled (below), ‘Summary of Annual Resource Buildouts from 46 MMT “Default”‘ the model shows exactly how much volume was considered in an annual basis from various resources. In another area, the 46 MMT model as suggests that by 2030, ~11 – 19 GW of battery storage will be deployed for the main purpose of shifting solar generation into the nighttime. The total (baseline + selected) battery storage RA capacity contribution is ~13 – 16 GW.

In the document are multiple modeled cases, with the 46 million megaton (MMT) of emissions as the current recommended model. It was noted, that while not equivalent, the state’s 60% renewable portfolio standard by 2030 and the 46 MMT model had similar procurement outcomes.

Per the document, all batteries considered in the IRP are 4 hour batteries, though it suggests that lithium ion will transition into 6 to 8 hours batteries by 2030. A battery recently approved by the New York State Public Service Commission is a 316 MW / 2528 MWh 8 hour energy storage facility.

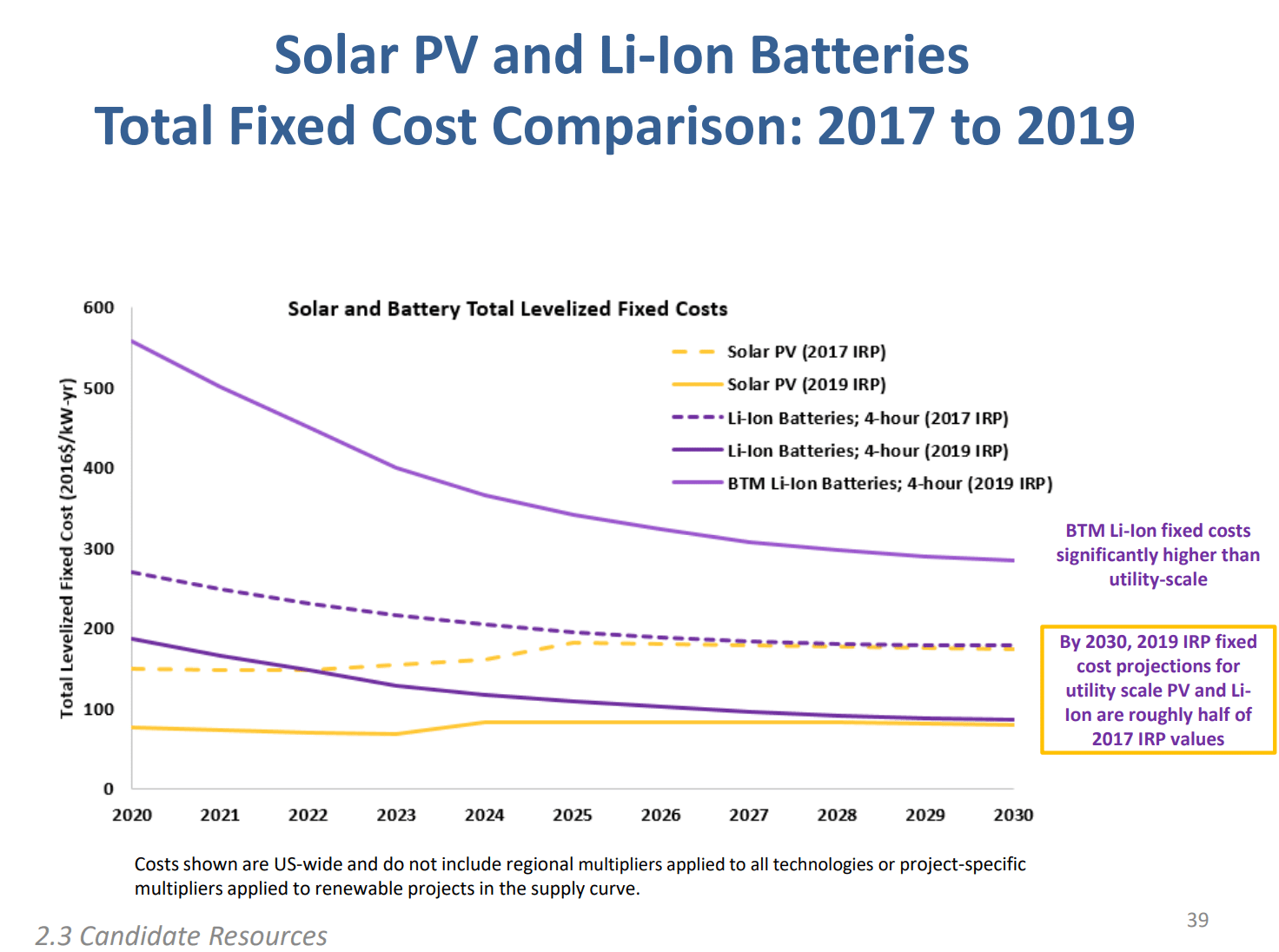

Part of the reason for the very large increase from prior IRPs for solar and energy storage is that both technologies have decreased in pricing much faster than projected (below image) – modeling that utility scale costs are roughly half of the 2017 IRP values. As well, in 2018, the preferred IRP noted that the Marginal GHG Abatement Cost was $219 per metric ton, and had fallen almost 50% to $113 per metric ton.

GHG emissions are modeled higher in 2024 relative to 2023, in large part due to the retirement of the Diablo Canyon Nuclear Power Plant. A capacity shortfall in 2021, followed by retirement of the 2 GW of capacity from the plant in 2024-5, results in all available gas power plants being retained for CAISO ratepayers through 2026 in all core policy cases.

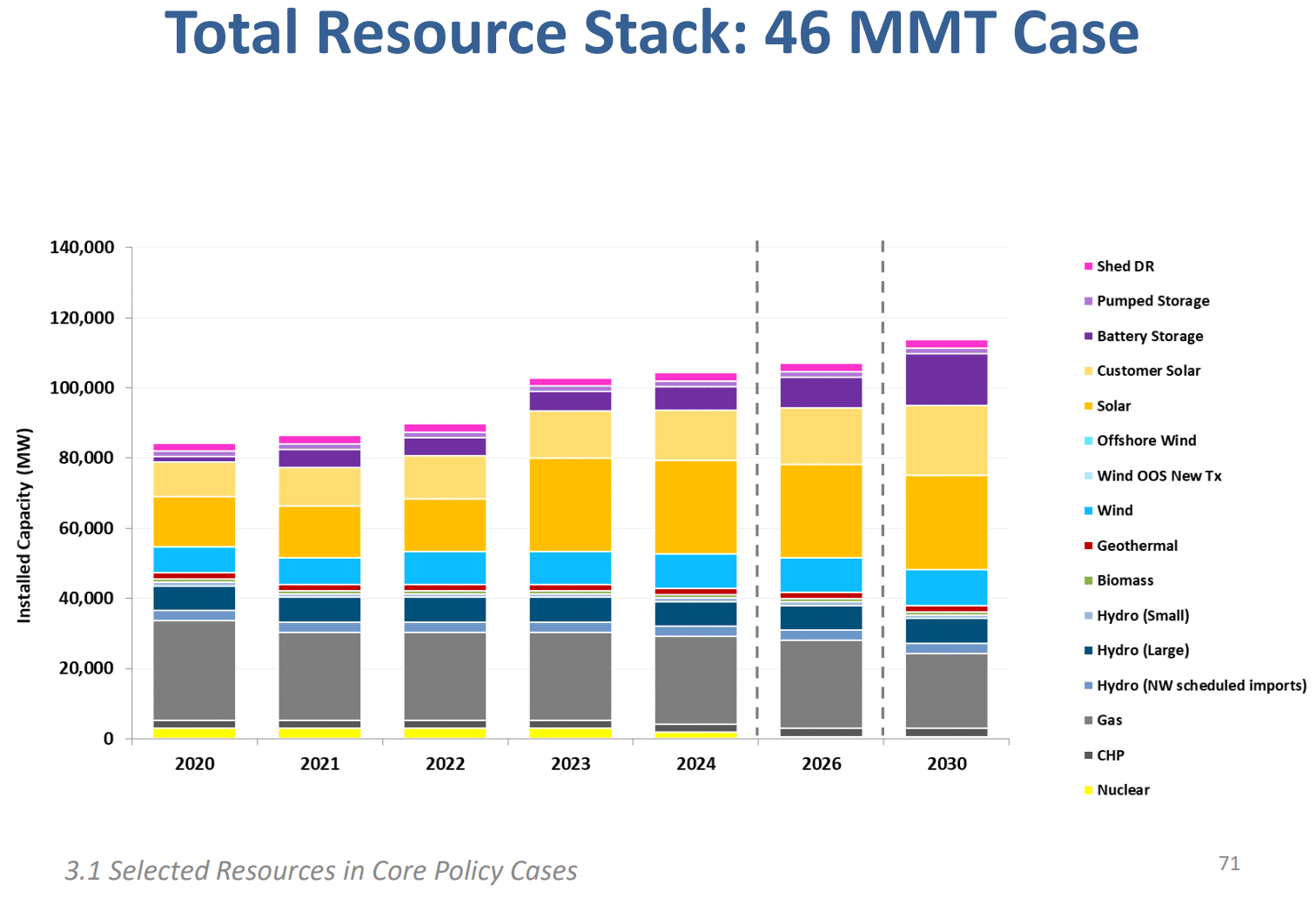

The below chart shows the total resources that are projected as part of the 46 MMT case through 2030. It is projected that to move forward the Levelized Total Resource Cost will be approximately $46.5 billion per year.

Last years IRP, modeled that 5.9 GW of solar and 2.1 GW of energy storage would be deployed by 2030, at a cost of $44.5 billion per year. As well, it included greater than 2 GW of geothermal, which was completely removed from this model.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

These estimates look absurdly conservative.

Having seen the LCOE of both PV and storage decrease by something like 30-50% more than predicted since the 2017 plan, they have adjusted the prices in 2020, but are sticking with the forecast of very little price decline for PV in 2020-2023 followed by a price increase to above 2020 levels and then fairly constant prices. Essentially they are doubling down on ignoring the reality of the falling cost of utility-scale PV power. In the storage arena, they have acknowledged the lower price in 2020 and predicted a somewhat steeper decline going forward than they predicted in 2017, but still nothing like the actual rate of price decreases between 2017 and 2019. So, the estimated cost of storage is somewhat more in agreement with price decreases in the real world, but is still radically less of a decrease than in recent years.

As wildly inaccurate as the price estimates look, they still look better than the predicted sources of power in the coming years. The resource stack between 2020 and 2030 shows no discernable increase in wind power after 2022 and no discernable increase in utility-scale PV power after 2023. I know how you get estimates like that: You include new power developments already contracted for or under construction and assume that, since there are no contracts for new solar or wind farms to com on line after 2023, that must mean that the market will ignore lowering prices and not one more panel or turbine will be erected. That’s absurd.

Obviously, as prices fall, more and more wind and solar PV developments are likely to come online. predicting that construction will cease after 2023 is beyond ridiculous.

Prediction: The 2021 IRP will look a lot like the 2019 IRP, showing much lower prices and more development of renewable power than predicted in the previous plan.

I’m not sure what is gained with the pessimistic and obviously incorrect predictions that the price of renewable power will stop decreasing and that, despite LCOEs likely to be below any fossil fuel alternatives, all deployment of renewable power facilities will cease after those currently contracted for are finished. It’s not true and everyone involved in coming out with these reports must know this.