Fitch Solutions Marco Research has released a report, Midwest US Set To Experience Strong Growth In Solar Sector, which makes some very bold predictions about the future of the solar industry in America’s heartland.

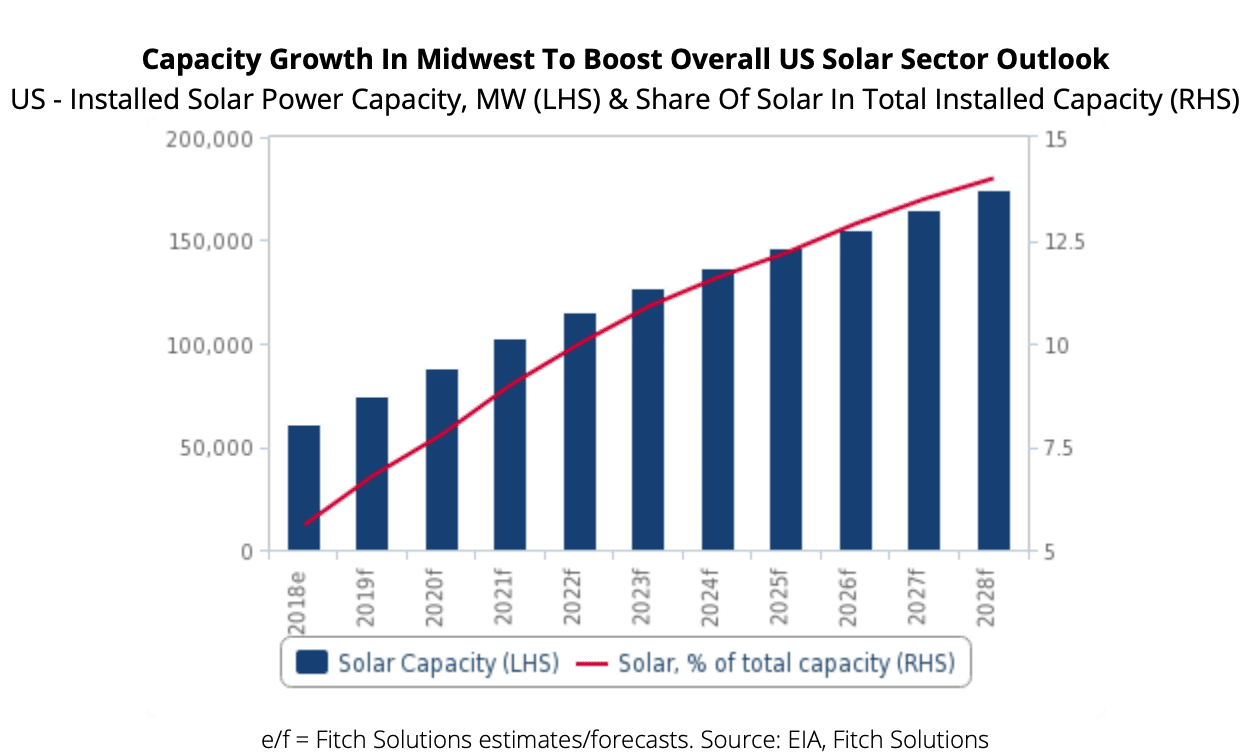

Chief among those bold predictions, Fitch states that it expects the region to contribute heavily to the 100 GW of solar power capacity expected to come to the United States over the next 10 years. This astronomical, gargantuan, whichever word of scope you use to describe, prediction is supported mainly by the region’s large proposed solar project pipeline, with a total potential added capacity of a smidge under 79 GWac that are registered within the MISO, SPP and PJM generation interconnection queues – the grid operators that cover the region.

Before we at pv magazine get to play know-it-all and bring up the estimation that only roughly 30% of all projects in an interconnection queue actually see the light of day (pun intended), Fitch addresses that concern and also offers that 6.6 GW of solar capacity is either under construction or in the latest stages of planning and likely to be completed through 2023.

Fitch expects that this unprecedented development will be driven by the strengthened renewable energy targets of Midwest states, cities and utilities. Chiefly among these targets, Fitch references Wisconsin’s 100% carbon-free electricity by 2050 goal, the 100% renewable electricity pledges made by Chicago, IL and Madison, WI, DTE and Xcel’s plans for carbon neutrality by 2050 and the litany of renewable energy-based requests for proposals sweeping the region.

Strangely, the report doesn’t address the trend of large corporations increasingly adopting renewable generations to fulfill their power needs. The report, however, also attributes the projected growth to year-ver-year improvements in the technologies associated with solar projects, the evert-falling costs of developing and installing solar and the expanding adoption of community solar initiatives in the region.

That last point is an especially interesting one, as in 2019 utilities in Illinois, Missouri and Iowa all launched their first community solar programs, with most being so successful that they led to over-demand and filled their capacities nearly immediately.

These projections by Fitch paint an incredibly bullish view on the future of solar development, one more optimistic than the projections made by Solar Energy Industries Association and Wood Mackenzie. These two organizations are currently projecting a 2019 solar market of 12.6 GW, with Fitch estimating an annual midwest average growth of 83% of that figure. Obviously the expectation is that those annual additions would increase exponentially so that the biggest additions are being made at the end of the decade. The 79 GW project pipeline only includes projects to be completed through 2023, so, if even a third of that goes on-line, that would lend major credence to the optimistic projections of the region as a whole.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

I remember vacationing in Portland Maine last year. The hotel’s car port had chargers and was powered by solar panels. If Portland Maine can do there is no reason the sunnier on average Midwest can’t do the same thing.

New Jersey and Massachusetts have done amazing things with solar also, if I’m not mistaken mostly due to strong REC programs… but in terms of generation capacity and performance, both of those States, Maine and the rest of New England in general are pretty equal in sun hours… no reason why the Midwest shouldn’t perform equally as well…

As a side note, for ease of reference I wish the authors here would add links to their references, I know the Fitch report is behind a register / paywall but would still be useful to have direct link rather than have to google it… minor inconvenience.

Yet another professional play-it-safe projection of linear growth. Is this really likely? Solar power plus storage will become cheaper not only than rival alternatives for new generation, but a rising proportion of existing capacity. That points to an acceleration in adoption – under current policies. The odds are also very much in favour of a further policy shift to renewables. The weighted average of Republican do-nothing policies and Democratic GND ones is very favourable to solar. Or use a cynical public policy armchair: the solar and wind industries gain more political clout as they grow, while that of coal and gas fades. Evidence? The repeated failures of Trump’s coal rescue efforts in the face of market headwinds, and the growing likelihood of ITC extensions for renewables that the Administration opposes. Throw in the inevitable rise in gas prices as the unsustainable and loss-making fracking boom ends and price equilibrium is restored.