Sunrun is becoming an entity unto itself. The might, driven by the heft of 1.5 GW of managed capacity, puts the company in a position to have greater access to hardware, better installation pricing, access to revenue streams competitors do not have, stronger securitization quality, and the resources to think, plan and create markets where none existed before.

Sunrun’s Q4’18 report capped a very strong 2018, which saw the company’s first quarter with over 100 MW of solar power deployed, over $240 million in total revenue, and a continuing increase in the future value of the revenue from solar systems.

Sunrun’s Q4’18 report capped a very strong 2018, which saw the company’s first quarter with over 100 MW of solar power deployed, over $240 million in total revenue, and a continuing increase in the future value of the revenue from solar systems.

Q4’18 saw 115 MW deployed, up from 85 MW Q4’17, and 99.8 MW in Q3’18, a 35% and 15% increase, respectively. Full year volume deployed grew from 323 MW to 373 MW, a 15% increase. 2019’s volume deployed is expected to grow another 16-19%.

Sunrun exceeded guidance on “cash delivered” from its building investment portfolio – with $63 million in 2018, and an expectation for greater than $100 million in 2019.

The company’s earnings per share were $0.32 below analyst estimates of $0.27, however, revenue for the quarter came in at the aforementioned $240 million versus the broad estimate of $199 million. The earnings per share shortfall seemed mostly to be the result of significantly increased volume deployed in the quarter, and the costs associated with that construction.

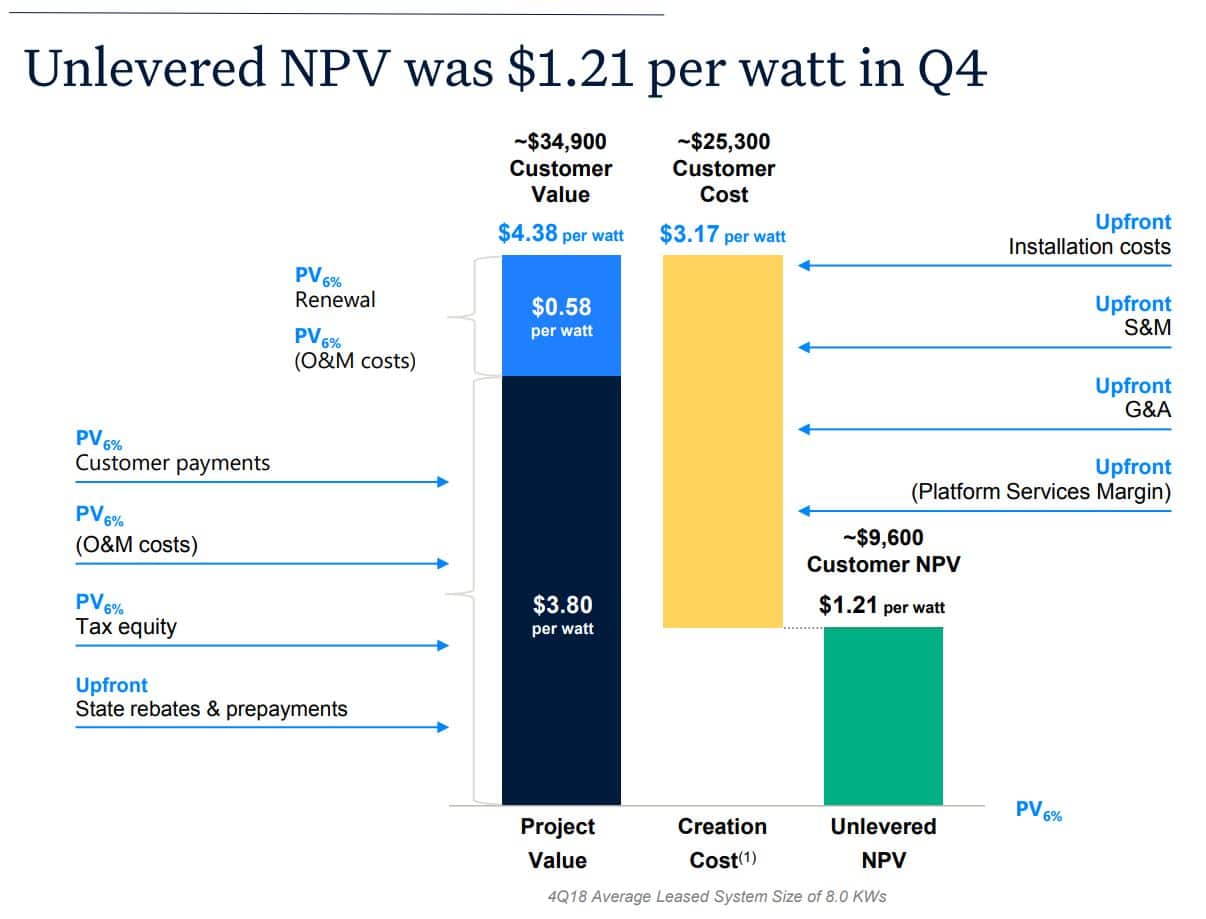

The company estimated that 2018 installations have a net present value of $1.08 per watt, and the company expects it to increase this going forward. The fourth quarter saw that value peak at $1.21 per watt installed. A future increase is expected even with the strong up-front costs of training and deploying teams to find new leads in Home Depot.

Sunrun’s 115 MW of volume installed in Q4’18 created $116 million of net present value, a 28% increase over Q4’17 of $91 million created.

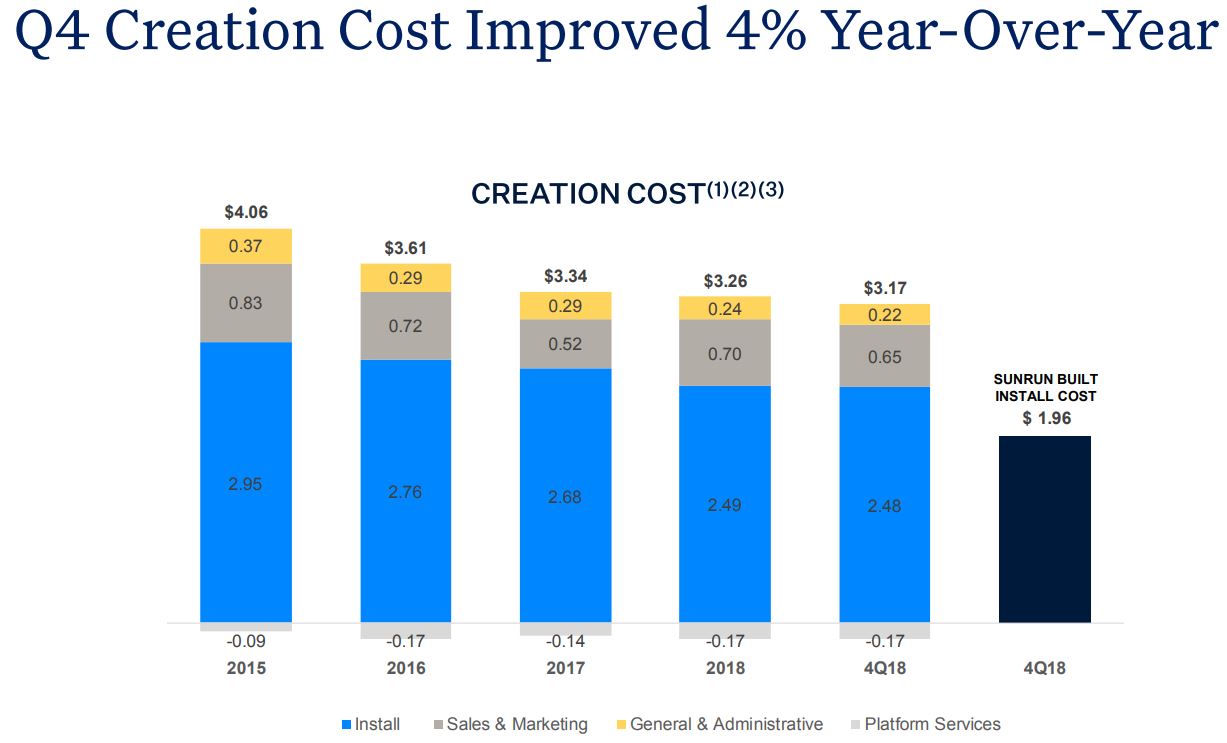

Though pure installation costs were still up over costs in 2017 of $1.89/Wdc, the company held the average price to $1.96/Wdc in Q4’18. Sunrun also said that it expects further operating efficiencies.

Sunrun hopes that by levering the safe harbor provision of the Investment Tax Credit, cost efficiencies and depreciation benefits that local solar companies cannot offer home owners will help it sustain double-digit growth for the next decade.

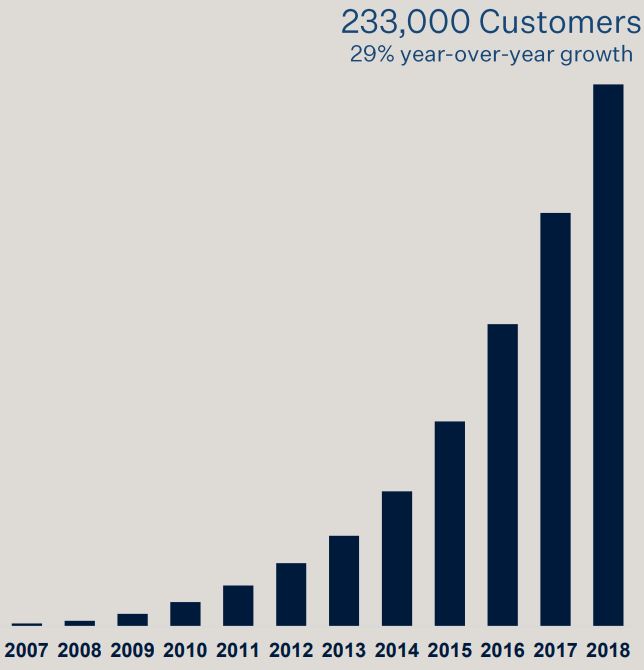

The company now totals more than 233,000 customers and 1.58 GW of solar power deployed. With the United States recently passing 2 million solar power plants, that means 1 in 10 solar systems are financed, owned and/or deployed by Sunrun.

Sunrun’s energy storage product – Brightbox – was a big topic and “nearly” hit the company’s 2018 goals of 5,000 units deployed. The company reached that number during Q1’19, and Sunrun hopes to at least double that volume over the course of the year. The company will require an estimated 5,000 units deployed into the New England ISO region to feed its future 20 MW contract in the wholesale electricity markets.

Help us learn more about you and what you want to read by taking pv magazine USA’s reader survey.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

A beast.

I look forward to the day I can have a 6 KW system for $6,000, installed.