Solar is becoming a powerful force as an asset class.

Solar provides revenue generation capability via decades of electricity production. Private equity loves the idea of building solar from the ground up. Developers love the idea of owning the rights to projects. And increasingly, we’re seeing residential solar loan companies come into their own to replace to retreating solar lease.

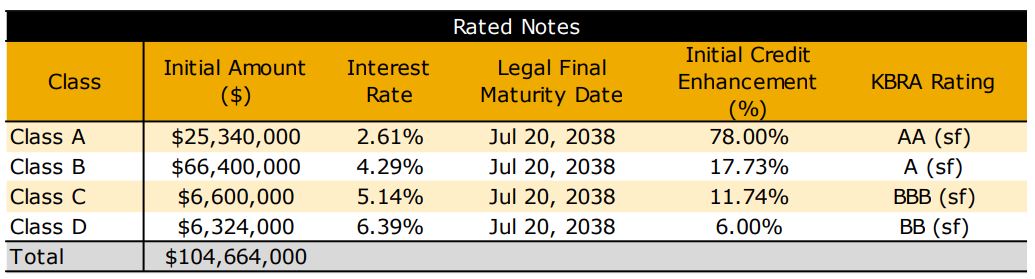

As part of these trends, Dividend Finance has now closed on its second residential solar loan securitization, as the first solar asset-backed security to receive an “AA” rating from the Kroll Bond Rating Agency (KBRA).

The portfolio valued at $105 million portfolio has also received “green bond” designation from Sustainalytics, “pursuant to the standard of the International Capital Market Association“.

The issuance report from KBRA breaks the portfolio down to investment grade-level detail. The base value of the portfolio was built upon 3,376 units with a total value of $92 million. The portfolio is mostly 20 -year residential solar loans in aggregate worth $110.2 million, after accounting for $17 million in ‘subsequent solar loans’.

Loan recipients in the portfolio have a weighted average original FICO score of 747 and 97% of pay through automatic withdrawals direct from bank accounts. FICO scores greater than 700 represent approximately 82% of the current principal balance.

By geography, California borrowers represent 18% of the outstanding principal balance. By state, the next-largest volumes are found in Texas (13%), Florida (12%), Arizona (12%) and Utah (9%) – though the loans cover PV systems in 24 unique states.

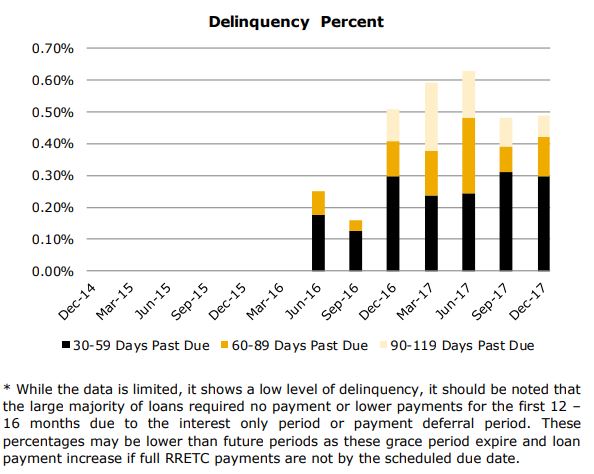

The agency noted the very low delinquency rate of the loans, with some notations regarding interest only, no payment or lower payment periods. These lower delinquency rates are definitely strong drivers of the portion of the product with the AA rating.

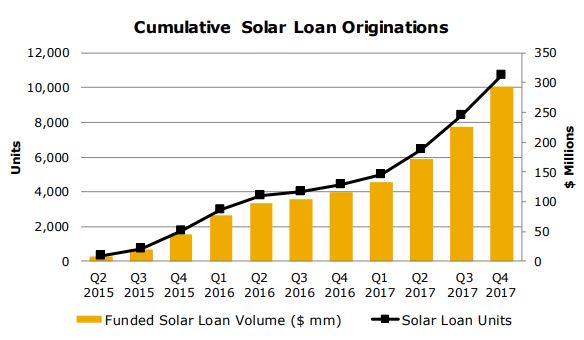

Dividend Finance has grown quickly in recent years, going from $40 million of cumulative loans at the end of 2015 to $100 million at the end of 2016. 2017 saw that $100 million grow by almost 300% to finish just short of $300 million – with Q4 alone adding roughly $70 million (equal to more than all of 2016’s loans).

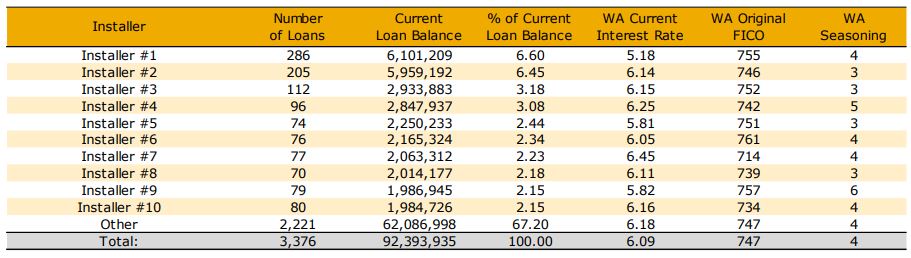

In what must help the executives at the company sleep well at night, the largest installer using Dividend products represents only 6% of the total portfolio – and the top 10 installers represent only 34% of the total portfolio.

The report seems to show a broad business base in multiple respects – many states, many installers, and both an increase in total volume deployed as well an increase in the rate of deployment.

When combined with other reports that residential solar has shown a possible 11% increase in Q1 2018, we might consider that the residential solar finance model at Dividend has the possibility of continued strong growth. If issuances such as this keep up their AA rating, and move quickly when sold into the investment grade marketplace – then we are likely to see the experiment at Dividend continue as they are going to have larger and larger pots of cash to work with.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.