After six months of suppressed global solar power investment in mid-2017, we saw clouds begin to part towards the end of the year on mitigated recommendations from the International Trade Commission in the Section 201 case. In its latest report Mercom Capital is suggesting these clouds have partially returned with ‘trade war’ talk between President Trump and China, and Indian tariffs getting headlines, as the first quarter rolled out.

However, even in the investment fog, the juggernaut of growing capacity continued its expansion as 7.7 GW of solar assets changed hands. New project funding also stayed stable quarter over quarter at $1.9 billion, even in the face of falling component and system prices.

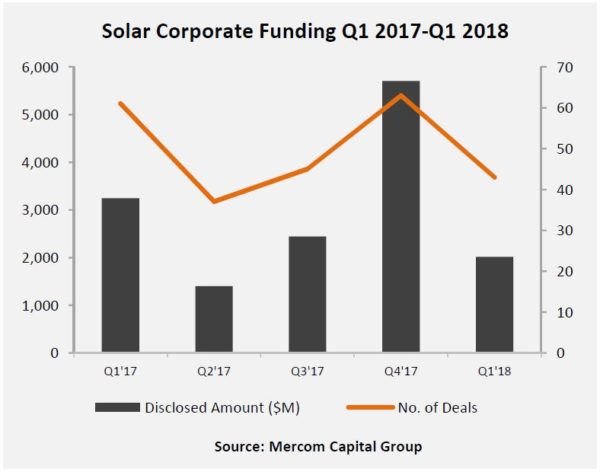

Mercom Capital has released its Q1 2018 Funding and M&A Report, which finds that $2 billion of corporate funding entered the sector, down 65% from the fourth quarter of 2017, and from $3.2 billion in the first quarter of 2017.

Multiple sectors saw overall investment fall:

- VC funding, including venture capital, private equity and corporate venture capital – $161 million invested in 22 deals, down from $639 million in Q4 and $588 million in Q1.

- Public market financing – $103 million for four deals, down from $657 million in Q4 and $461 million in Q1.

- Debt financing – $1.8 billion in 17 deals, down from significantly from $4.4 billion in Q4 and $2.2 billion in Q1.

And in a small, but growing market – we’re seeing the U.S. residential solar power loan market continue its love affair with the American consumer. In a small data set, we saw only a single residential solar funding for the quarter of $400 million by Sunlight Financial. This compares to $213 million in Q4, and $630 million in Q1’17.

This is accelerating, and the first five days of the second quarter saw at least $325 million ($225M/$100M) in residential funding.

As the cumulative capacity of solar power projects keeps growing we’re seeing continued strength in large project financing as 7.7 GW of solar power plants change hands during the first quarter. The estimated 99 GW of solar installed in 2017 pushes the global capacity to over 400 GW, and these projects are producing more than 560 terawatt-hours of electricity annually – roughly worth $28 billion a year (at 5¢/ per kilowatt-hour). With the global market expected to grow to potentially 113 GW (or up to 126 GW by some estimates) – we expect to see the global installed capacity expand by at least 25% this year alone.

This will drive asset management markets upward, significantly and continually as corporate and pension fund groups look to lock in long term fixed energy rates and cash flow.

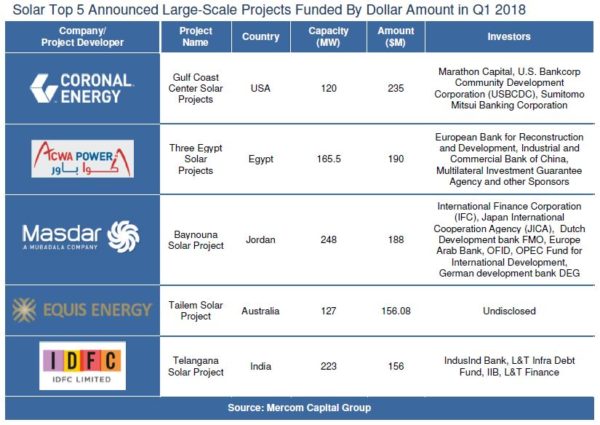

- Large scale project funding in Q1 totaled $2.7 billion in 58 deals, versus $3.7 billion in 49 deals in Q4 and $2.6 billion in 33 deals in Q1’17.

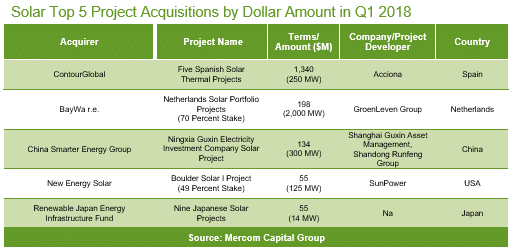

- 80 large scale project acquisitions, vs 67 in Q4 and 49 Q1’17. The announced values for 16 of the projects was $1.9 billion, with the Q4 announced values at $3.7 billion, and $1.9 billion in Q1.

- 20 projects totaling 1.2 GW were purchased by investment firms, 30 projects at 1.3 GW by utilities and independent power products, and 3.4 GW were acquired by project developers in 14 projects.

2017 saw growth over 2016 in solar power funding globally, and the 4th quarter of 2017 was especially strong as a lot of global pressure let loose. However, we are seeing complexity again – with India and Trump making China noise.

Growth will come though – it is inevitable, to a degree. We saw record 96 GW of new solar manufacturing capacity announced in 2017 – from wafers, to cells and module assembly. This capacity will need funding, and with margins being tight – corporations will probably reach out to the markets for capital.

As the solar industry continues to expand, it is becoming a much more nuanced, broad and complex industry to forecast and describe, much like a healthy ecosystem.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.