Investments into PV capital expenditure (capex) across the United States are set to grow significantly in 2027, in what is likely to be a breakout year for the domestic crystalline-silicon (c-Si) industry.

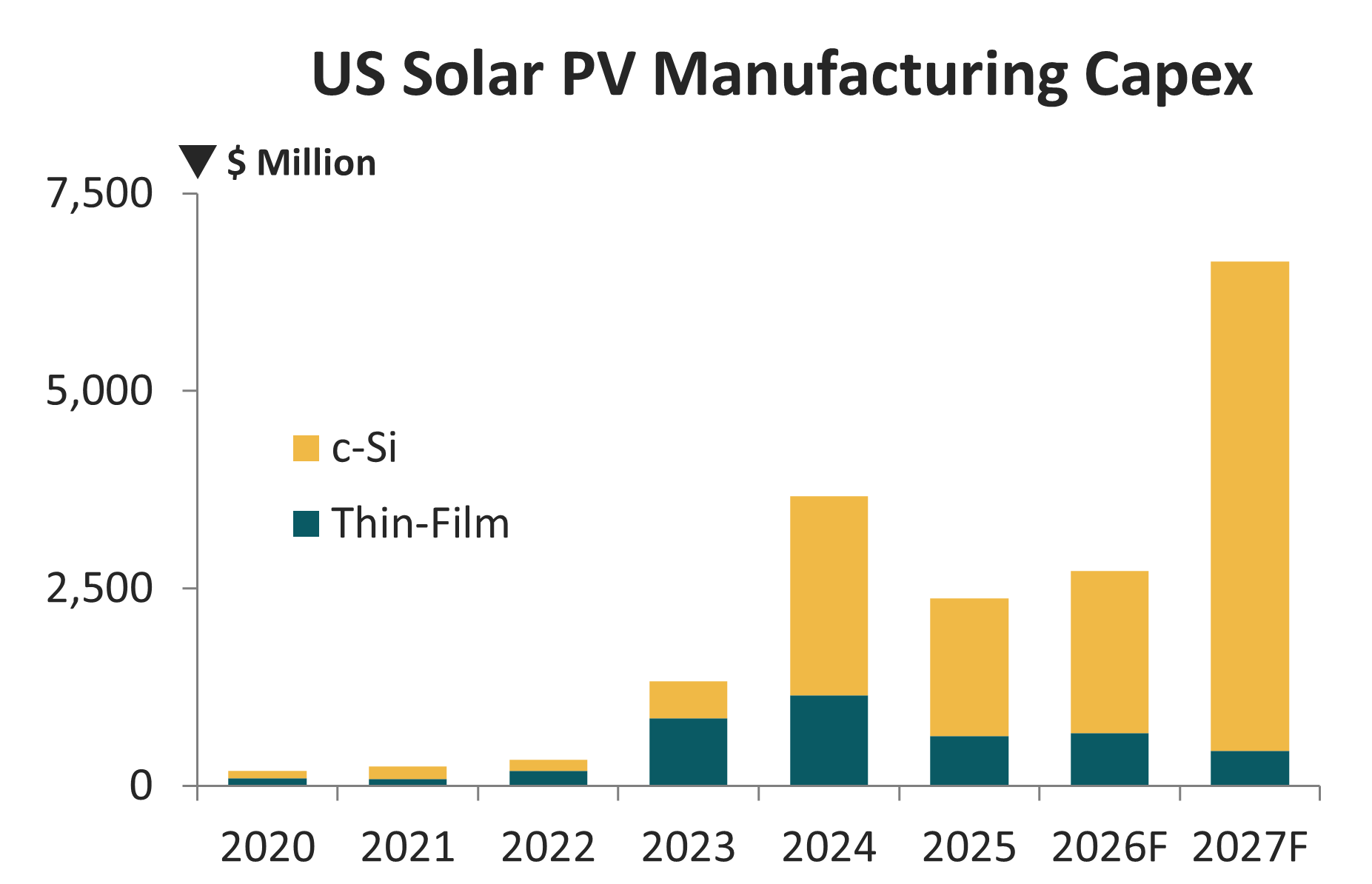

Capex is forecast to reach as much as $7 billion in 2027, representing a year-on-year growth of about 150%, with investments into the c-Si value-chain potentially accounting for more than 90% of spending, compared to about 10% from thin-film (First Solar).

This article provides the first detailed analysis of U.S.-specific PV manufacturing capex, created bottom-up by analysing the investments, effective capacities and production levels of more than 35 domestic producers in the United States; by year back to 2020 and by quarter out to the end of 2027.

The details behind this new analysis form the backdrop to the content that will be presented on-stage at Solar Manufacturing USA 2026 in Austin, Texas on 22-23 September 2026 – the first event to be held in the United States dedicated exclusively to domestic PV production, equipment supply, technologies deployed and materials supply-chains.

Capex and opex the new metrics for domestic production

Since details regarding the Inflation Reduction Act were revealed back in 2022, manufacturing capacity in the United States has evolved in a somewhat lumpy fashion, characterized by First Solar’s new thin-film factories across various states in the Southeast and a spread of c-Si module factories across the country, with Texas taking the lead from a production standpoint.

While a massive step forward for a country that was for years being supplied by factories in Southeast Asia, financed and operated mostly by Chinese PV manufacturers, the investment climate for full value-chain c-Si capital spending has been largely subdued in the United States in the past few years.

This was due to uncertainty. Would the United States continue to be supplied by upstream components produced overseas as foreign companies moved capacity from one country to another to avoid the latest round of AD/CVD tariffs? Or would the requirements on foreign-ownership and control create a void in expansion plans that domestic entities were unable to fill?

However, over the past 6 months, it appears that these uncertainties have been overcome. Legacy issues with foreign ownership appear to be getting addressed now and plans have emerged from companies such as Canadian Solar, Corning and Tesla that suggest a new landscape for domestic PV manufacturing in the United States is imminent.

In short, it appears that the build-out of a domestic manufacturing ecosystem is now an accepted reality; not just for upstream cells, wafers and ingots, but the accompanying raw materials supply-chains feeding into manufacturing activity through the value-chain.

At last, the United States is moving from tracking ambitious capacity announcement plans to analysing capex and operating expenditure (opex); the key metrics associated with a credible and sustainable manufacturing segment.

First Solar’s US expansions to be eclipsed by silicon-based competitors

Since 2023, First Solar was the leading company investing in new manufacturing capacity in the United States, with over $2.5 billion committed between 2023 and 2025 to new greenfield sites in Alabama and Louisiana, in addition to upgrades in Ohio. This level of spending accounted for about one third of all PV capex in the United States during this period.

It now appears that 2027 will be the breakout year for c-Si capex in the United States, driven partly by new capacity additions at the cell stage from existing module producers. However, the major additions in 2027 are coming from the anticipated start of capex by Tesla and an expected round of ingot/wafer and module capacity investments from Corning.

First Solar’s new thin-film factories in Alabama and Louisiana were major contributors to the uptick in U.S. PV capex during 2023 and 2024, with c-Si based PV capex now dominating investments.

Spending on deposition tools from 2027 could be a pivotal moment

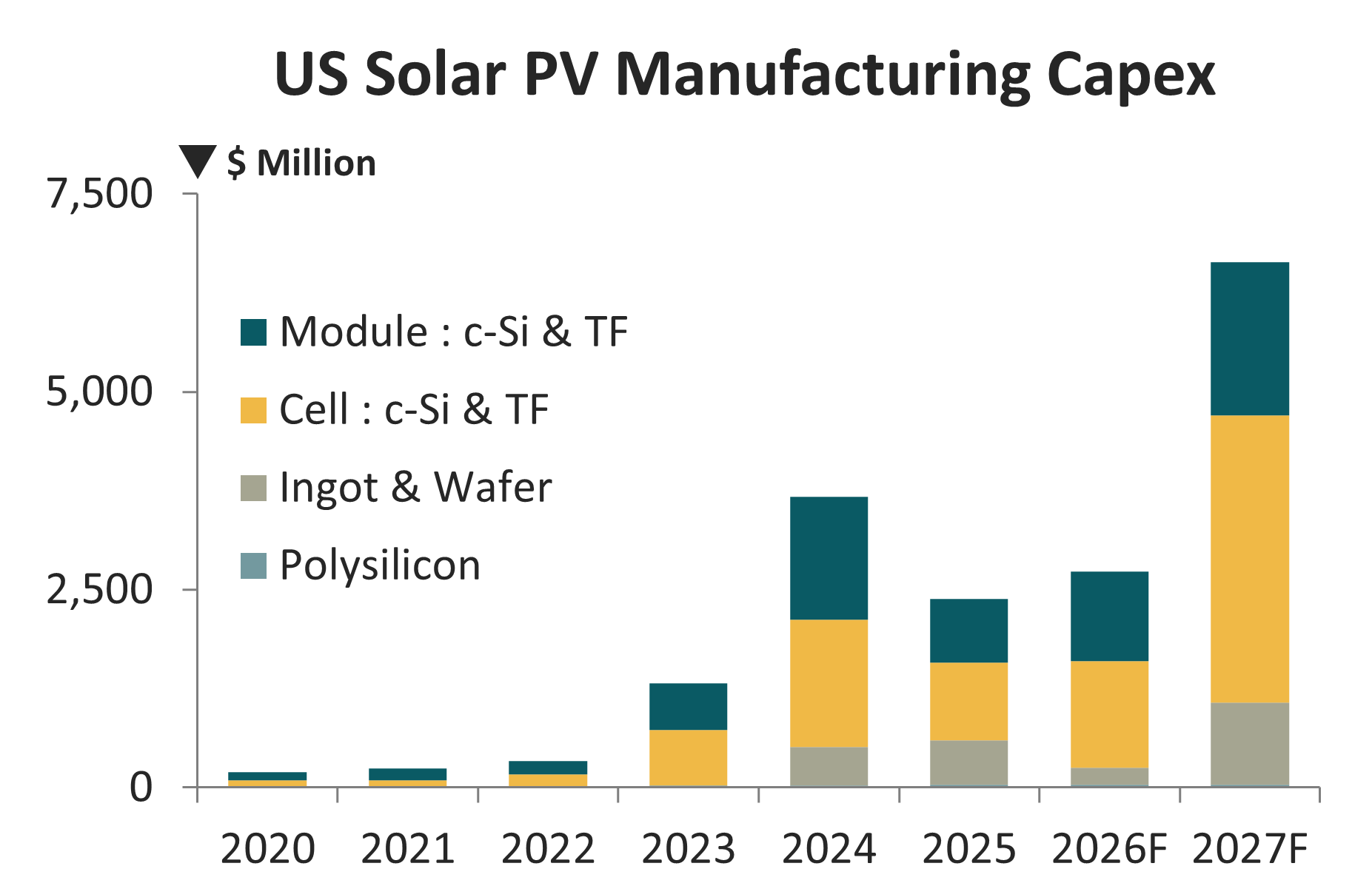

Until now, c-Si spending has largely been focused on new module assembly lines, with most of the deposition equipment capex coming from First Solar’s new thin-film investments. However, this is set to change as cell capacity is prioritized from 2027.

Across both c-Si and thin-film value-chains, deposition equipment is probably the most important aspect of any technology roadmap and in-house technical competence. This was recognized by the China PV ecosystem back in 2017-2018 as the country set out to own deposition tool development and production as the engine for its leading cell producers to move from p-type mono PERC structures to more advanced cell architectures.

While having a strong accumulated capacity for polysilicon production, ingot pulling, wafer slicing and module assembly is necessary to build out a self-contained PV manufacturing ecosystem, technical competence and leadership on critical tools and process flow arrangements for cell fabrication is essential for the United States to become a key player in the PV manufacturing space.

US PV capex in 2027 is forecast to see the first major spending in c-Si cell build-out, with the domestic sector moving from module assembly capability to cell fabrication knowledge and ownership.

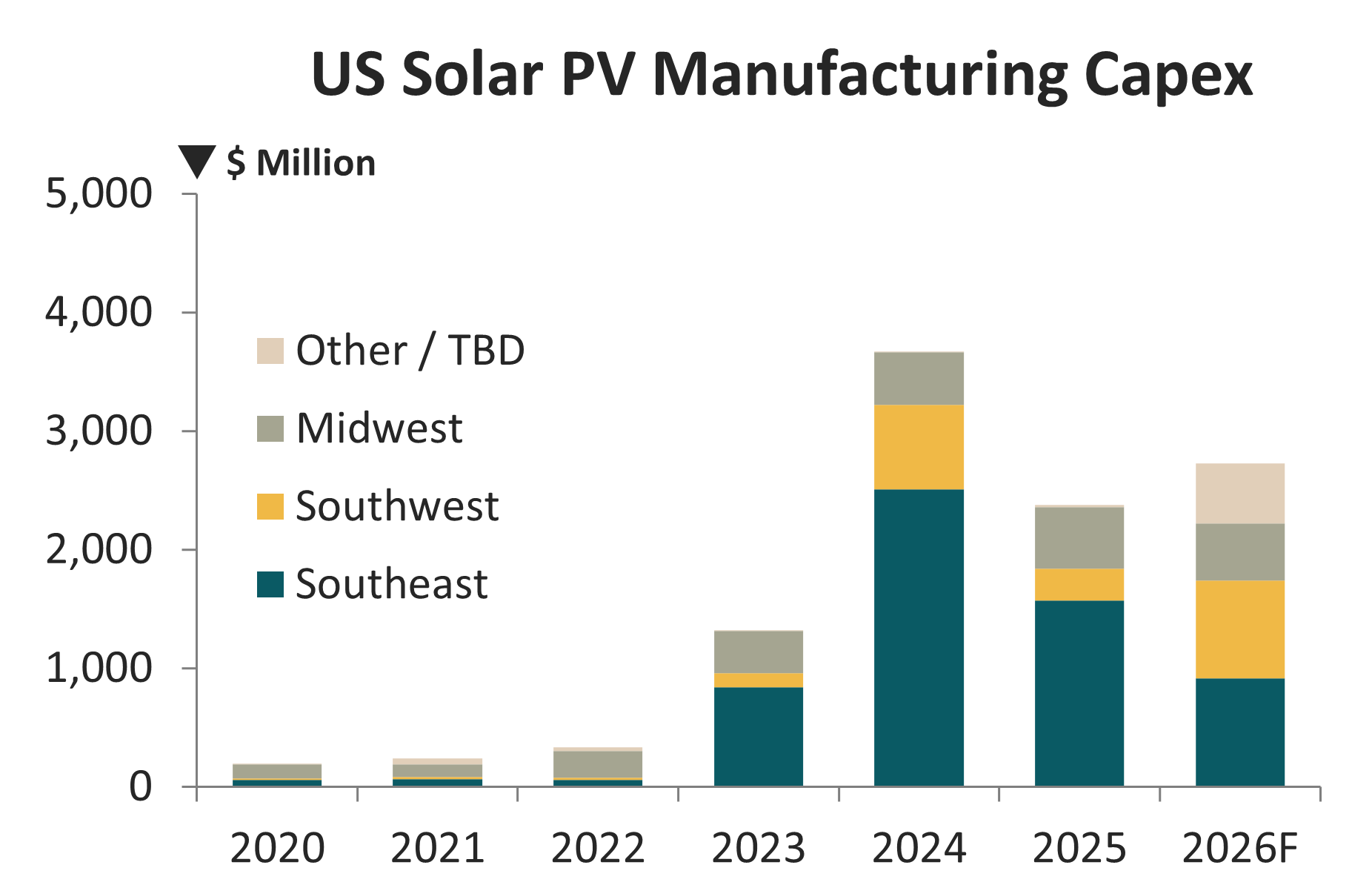

Southeast hubs emerge while Texas still the frontrunner in module production

No different to the bidding wars that tend to exist elsewhere globally when new factory investments are first muted, PV capex in the United States has gravitated to locations where incentives are on offer.

This has created a hub of activity across states in the Southeast including Alabama, Georgia and the Carolinas. All of First Solar’s expansions outside Ohio have been in the Southeast; Alabama, Louisiana and South Carolina.

Texas dominates PV capex in the Southwest, including Canadian Solar, Elin Elektrik, Waaree Energies, VSun, T1 Energy, SEG Solar and Imperial Star.

Outside First Solar’s thin-film capex in Ohio, states in the Midwest have also been the subject of capex, most notably Canadian Solar’s cell build out in Indiana and Corning’s new ingot and wafer lines in Michigan.

However, a large contribution from the capex forecast in 2027 is coming from Tesla’s plans that have yet to reveal a specific location, either as a stand-alone integrated hub or through geographically disperse capacity additions.

States across the Southeast, Southwest and Midwest dominate new PV manufacturing capex today in the United States, with Tesla’s factory location(s) yet to be revealed.

While the spending of the 35-40 companies driving the expansion of PV manufacturing today in the United States can be assigned to specific areas, the largest swing factor in forecasting capex (and the associated additional c-Si production volumes in the United States from 2028 onwards) is coming from Tesla’s plans to establish one of the largest PV manufacturing entities seen in the PV industry.

Forecasting domestic capex is now essential to understanding the growth of US PV manufacturing

Capex is the most important metric for any manufacturing analyst; scrutiny here cannot be underestimated. Granularity on capex at the quarterly level (value-chain and technology / process-flow specific) allows production ramp-up and phasing to be established in a far more credible and useful way than the legacy focus in the United States on unsubstantiated and speculative media announcements.

Capex provides a means of forecasting productivity 12-18 months in advance, but not any longer. In this context, the forecasting to the end of 2027 shown in this article is at the limits and is required to pre-empt firm details on some of the 2028-2030 production activity that could see major changes in the overall U.S. PV production landscape.

This includes expected capex allocations from Corning in 2027 to meet the company’s 2030 solar targets.

But the largest impact to 2027 capex is coming from Tesla’s plans. The scale and ambition of building out 100 GW of c-Si capacity (ingot-to-module, or just cell / module) seems to have spooked the U.S. PV sector, with few outlets factoring in the potential impact of this huge volume of new capacity on the domestic scene.

On the balance of probability, I have included this as a key part of the circa. $7 billion PV capex forecast for 2027, albeit yet to be assigned at any state level.

The question from my side is not debating whether a large portion of the plans will come to fruition, but how to phase the spending at various parts of the c-Si value-chain. The scope for market disruption here is so profound that all stakeholders in the U.S. PV industry need to be taking notice and reviewing what impact Tesla’s plans could have on the overall industry trajectory out to 2035.

The new Solar Manufacturing USA 2026 conference in Austin, Texas on 22-23 September 2026 has been created to understand and map out exactly how the domestic manufacturing landscape in the United States will unfold in the coming years.

If you want to be part of this special gathering and share your views on the domestic manufacturing space, you can get in touch through the contact links on the event portal here.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.