Recently announced policy measures carry far-reaching implications for the US solar industry, beyond simply increasing procurement costs. These are significantly influencing project developers’ supply chain realignment strategies, regulatory compliance risks, and the strategic manufacturing plans of global companies.

Key escalations in US trade policy affecting the solar industry in 2025 include: the increased tariffs implemented on imports from many regions since April 2025; the final antidumping and countervailing duty (AD/CVD) rulings on imports from Cambodia, Malaysia, Thailand, and Vietnam; the petition for AD/CVD investigations initiated in July targeting India, Indonesia, and Laos; and the enactment of the One Big Beautiful Bill Act (OBBBA).

April 2025 tariffs

On April 2, 2025, the White House issued an executive order imposing import tariffs on a global scale, with measures specifically targeting PV cells and modules. Imported solar grade polysilicon and wafers are exempt from these tariffs. Many countries remain engaged in trade negotiations with the United States, though some level of tariff is expected in most cases. On Aug. 12, the US administration announced a 90-day extension to an agreement that maintains a 30% tariff on Chinese imports to the United States, and 10% on US products shipped to China. There is still a risk that these could increase greatly, depending on negotiations between the two powers. The announcement of tariffs has prompted numerous suppliers and US project developers to renegotiate contracts and address fulfillment challenges, resulting in project delays and cautious sentiment.

AD/CVD rulings

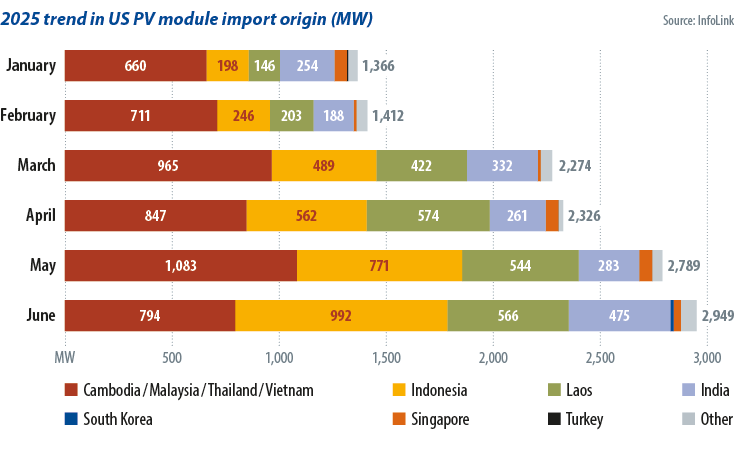

On April 21, 2025, the US Department of Commerce (DOC) issued final AD/CVD rulings targeting solar imports coming from Cambodia, Malaysia, Thailand, and Vietnam, effectively curtailing the strategic relocation of Chinese manufacturers to these countries following previous AD/CVD measures imposed on imports from China. By 2024, Chinese enterprises had established manufacturing clusters in these four countries with over 45 GW of cell capacity and 72 GW of module capacity. Under the new tariff policies, these production hubs are undergoing gradual phase-outs.

A new petition requesting further action on solar imports originating in India, Indonesia and Laos was submitted to the DOC on July 17. Following the imposition of AD/CVD on the four previously mentioned Southeast Asian countries, Chinese-funded companies have shifted manufacturing capacity to third countries like Indonesia and Laos, which are not yet subject to AD/CVD, and are expected to have a combined capacity of 43 GW for cells and 27 GW for modules by the end of 2025. Surprisingly, India is also included in this petition, despite its past exports to the United States making up only a small portion of its overall production.

Supply chain transformation

Tightening trade and supply chain regulations are prompting developers in the United States to rethink procurement strategies and project timelines. With rising import barriers across multiple countries, the previous focus on sourcing low-priced modules is shifting. Projects now face challenges of cost fluctuation and fulfillment risks. Some require financial model revisions, thus delaying power purchase agreement (PPA) signings and prompting adjustments to construction schedules, leading to heightened market caution.

Supply chain compliance is overtaking price as developers’ key focus. US policies increasingly emphasize transparency in module sourcing and manufacturing, prompting developers to invest more in supplier audits and compliance systems. This not only raises soft costs of projects, but also strengthens administrative and legal risk management.

Scrutiny of third-country production is also tightening, as deep ties to restricted supply chains may still pose policy risks despite capacity shifts to other countries. For developers, traditional risk assessments based on “country of origin” are no longer sufficient in what is now a more complex policy landscape.

More developers are prioritizing domestic supply chains as a practical way to reduce policy risks and compliance uncertainty, despite potential tradeoffs in cost or technology. At the same time, some are adjusting project timelines and contract schedules to avoid exposure to policy risks and compliance disputes during regulatory transitions.

In the long term, market competition is shifting from cost advantage to supply chain transparency, compliance capability, and risk management. Developers with robust internal controls and compliance frameworks will be well-positioned to lead in the evolving market.

About the author

Alan Tu is a senior solar analyst on InfoLink Consulting’s solar research team. He monitors policy trajectories and potential impacts on the solar industry. Tu conducts research on cell supply, demand, and price trends, reporting price updates and exploring connections between the solar market and international trading.

Alan Tu is a senior solar analyst on InfoLink Consulting’s solar research team. He monitors policy trajectories and potential impacts on the solar industry. Tu conducts research on cell supply, demand, and price trends, reporting price updates and exploring connections between the solar market and international trading.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.