In its latest Energy Storage Monitor report, Wood Mackenzie outlined the continued trend of rapidly increasing battery energy storage deployments across the U.S., with data through Q1 2024.

Across all segments, the U.S. energy storage industry deployed 8.7 GW, a record-breaking growth of 90% year-over-year. The nation deployed 4.2 GW in Q4, 2023, and California and Texas installations accounted for 77% of Q4 additions, said Wood Mackenzie.

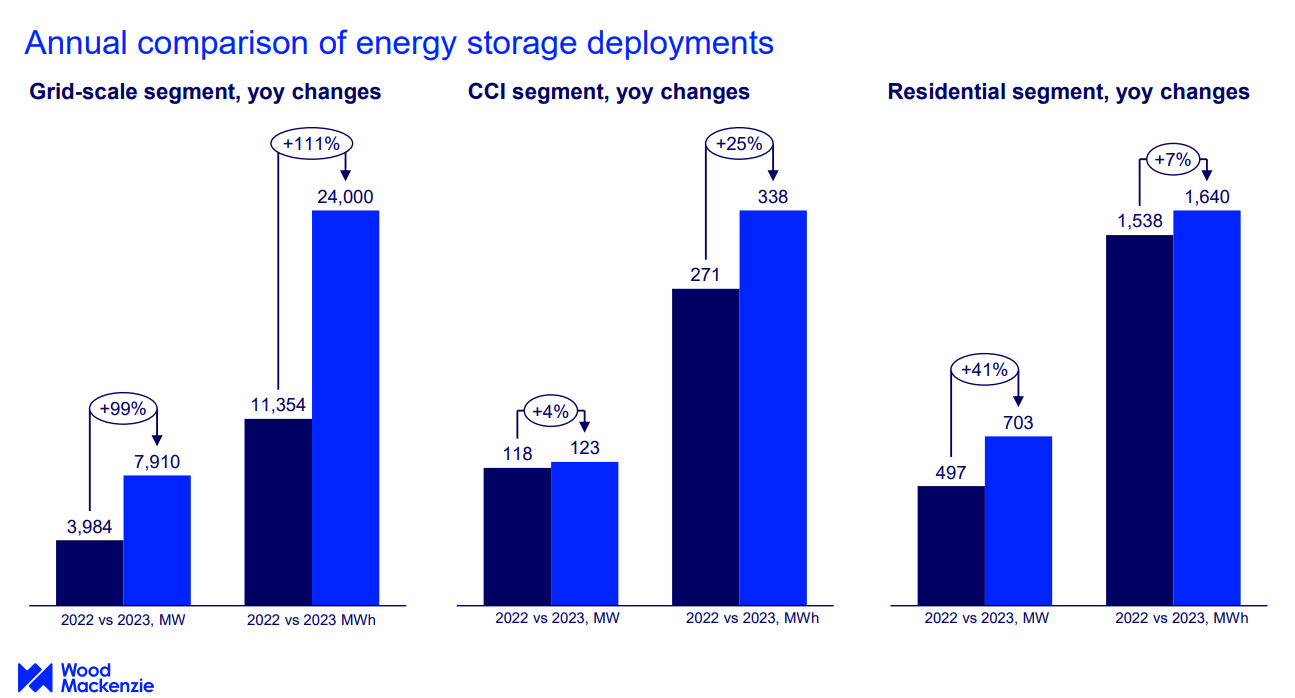

The U.S. grid-scale storage market shattered previous quarterly installation records in Q4 2023, deploying 3,983 MW / 11,769 MWh, leading to an average duration of 2.95 hours. A combination of short-duration energy storage serving acute peak electricity demand times, and four-hour grid-scale batteries are common configurations in today’s market.

The residential energy storage market reached a marginal record quarter in Q4, 2023, deploying 218.5 MW, beating the record set by Q3 of 210.9 MW. The community, commercial, and industrial (CCI) segment deployed 33.9 MW, with the most deployment occurring in California, Massachusetts, and New York, said Wood Mackenzie.

“Q4 2023 was extremely strong for the U.S. energy storage market, helped by easing supply chain challenges and system price declines,” said Vanessa Witte, senior analyst, Wood Mackenzie.

The storage boom has been supported in part by drastically lowering costs. In Q4, battery prices declined rapidly, in large part due to lower-than-expected EV demand in the U.S. and EU, and due to an oversupply of battery grade lithium raw material.

“Chinese OEMs (original equipment manufacturers) are selling DC blocks at aggressively low prices, undercutting competitors in order to gain market share,” said the Wood Mackenzie report. “However, this price pressure isn’t enough for all developers to turn away from the full AC-block solution of a more traditional integrator.”

Since last summer, lithium battery cell pricing has plummeted by approximately 50%, according to Contemporary Amperex Technology Co. Limited (CATL), the world’s largest battery manufacturer. In early summer 2023, publicly available prices ranged from $0.11 to $0.13 /Wh, or about $110 to $130 per kWh. Goldman Sachs predicts that these price reductions will make electric vehicles as affordable as gasoline-powered vehicles, leading to increased demand.

While the grid-scale segment grew 98% year-over-year in terms of capacity deployment, Wood Mackenzie warns this growth curve is not likely to continue.

“Growth flattens in 2025 and 2026 as project capacity is pushed into later years of the forecast largely due to early-stage development challenges such as permitting and siting difficulties, and interconnection queue timelines,” said the report.

Meanwhile, Wood Mackenzie expects the residential segment to grow to 2.1 GW per year in 2024, while CCI is expected to install 1.2 GW annually. It said that the emergence of storage incentive programs and the transition to NEM 3.0 in California will support distributed storage growth in the coming years. It also highlighted strong distributed energy storage growth in Puerto Rico.

“Energy storage has unique capabilities to address grid resilience, with the ability to serve as generation, load, and transmission. These benefits to the grid have been evident, especially in recent years, as storage has provided reliability and stability during critical moments like historic heatwaves. With a robust pipeline, the future for energy storage deployment is strong,” said John Hensley, vice president of markets and policy analysis, American Clean Power.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

Well, I am glad to see that something is booming in the renewable energy market. IMHO – I have been experiencing lackluster renewable energy growth here on the eastern shore states of Maryland, Delaware, and Virginia. Although there is some growth, it’s certainly not at the phenomenal rates that you are reporting.

I just hope you are reporting your data correctly as my data shows just the opposite.