The recent report “Energizing American Battery Storage Manufacturing” by the Solar Energy Industries Association (SEIA), noted that credits offered through the Inflation Reduction Act (IRA) have spurred adoption of electric vehicles, energy storage and other forms of electrification. However, domestic battery manufacturing is still in its nascent stages.

Just over a year ago, in quick response to the IRA incentives, a raft of manufacturers announced plans to set up shop in the U.S. And the announcements continue: Freyr announced a multi-phase project that is expected to bring battery manufacturing to Georgia. Kore Power recently received a conditional loan commitment from the DOE Loans Program Office, receiving $850 to build battery cells for electric vehicles and grid-scale storage. LG Energy Solution quadrupled its announced investment in two manufacturing plants in Arizona.

While the announced build-out of domestic manufacturing is promising, many questions remain as to whether the manufacturers can overcome the many hurdles on the way to meeting the growing storage needs. According to the SEIA report, U.S. manufacturing capacity for all lithium-ion battery applications is currently at 60 GWh, while demand for battery energy storage systems (BESS) in the U.S. is likely to increase over six-fold from 18 GWh to 119 GWh by 2030.

The SEIA report forecasts that the announced manufacturing facilities could increase domestic capacity to over 630 GWh over the next five years. However, much of this supply may be directed toward meeting demand of EV manufacturers, rather than that of non-vehicle applications like BESS.

SEIA said over 25% of the new factories have not publicly stated their intended markets and some (if not all) of their capacity may go to BESS, so there is still hope for steady supply.

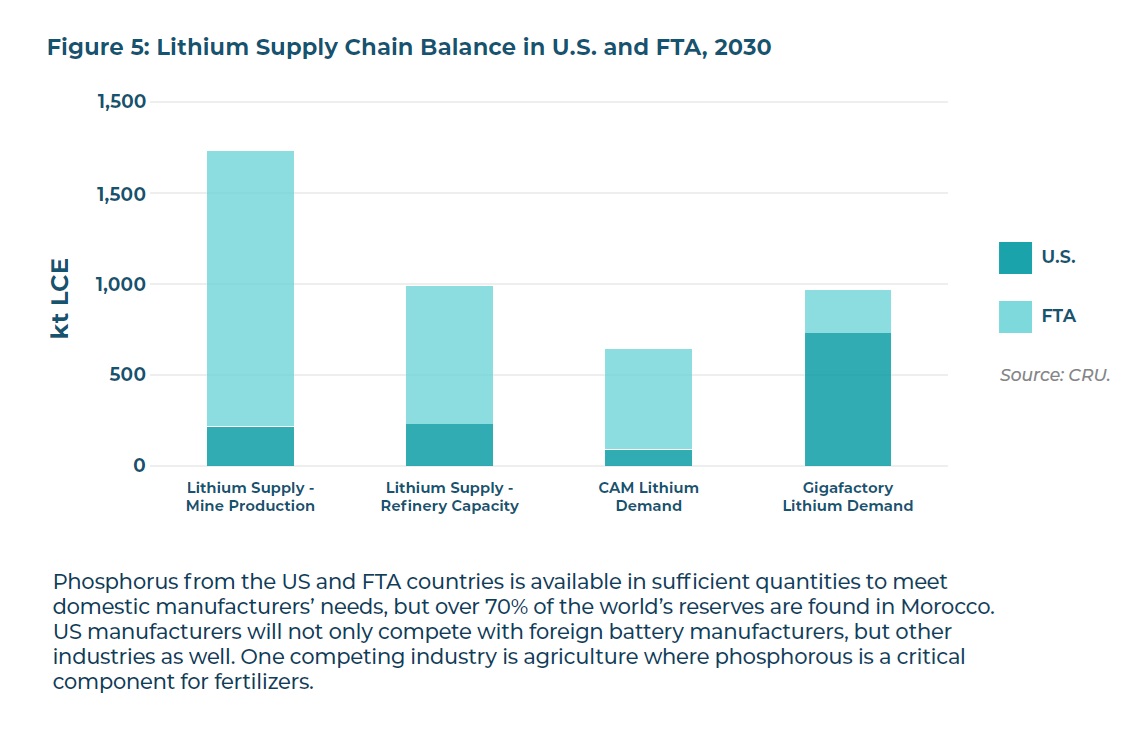

Material supply and cost

The majority of batteries manufactured in the U.S. are lithium, and while the U.S. has vast reserves of lithium other materials are needed such as phosphorous and graphite. These materials are sourced primarily from outside the U.S., so domestic manufacturers are competing on a global scale, often finding high prices and short supply.

Workforce challenge

Workforce challenge

As with the rest of the renewable energy buildout, securing a strong, skilled workforce is a challenge. According to the SEIA report, roles critical to energy storage supply chains include mining, chemical and electrical engineers, machine operators, production technicians, and more. While apprenticeship incentives are part of the IRA, growing the workforce long term requires committed collaboration among manufacturers, government agencies, training facilities, and other stakeholders.

Building a domestic renewable energy supply chain includes support for energy storage development at all levels, and the report contends that this will require investment, partnerships with experienced manufacturers, and collaboration with allies

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.