The Energy Information Administration (EIA) provides both near-term and long-term projections for capacity additions across all generation profiles. The technology showing some of the most long-term promise, particularly in light of the $369 billion climate and energy package in the Inflation Reduction Act (IRA), is solar.

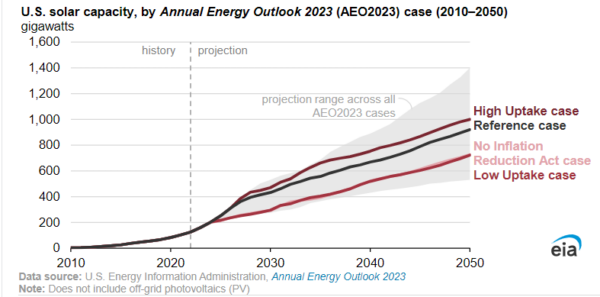

Based on 16 different scenarios, cumulative solar deployment across residential, commercial, and utility scale could range between 536 GW to 1.4 TW by 2050. The IRA may lead to as much as an additional 274 GW of solar deployment over pre-policy projections.

Across all cases, a range of about 700 GW to 1,124 GW of new renewable capacity, from solar, wind and energy storage, will be added over the projection period. Renewables represent about 65% of cumulative additions over the projection period without the IRA. In the reference case, renewables represent 69% of new buildout.

Solar and wind generation together increase from 15% of total generation in 2022 to 39% in the no-IRA case by the end of the projection period. IRA provisions in EIA’s reference case push wind and solar to 56% of electricity generation by 2050.

EIA said energy consumption may rise by as much as 15% by 2050, driving demand for solar buildout. Federal, state, local, and utility carbon reduction goals, as well as a push for corporate solar procurement and consumer interest in clean technologies will all drive demand forward. This demand will be amplified by provisions in the IRA, which include investment tax credits, production tax credits, grants, pilot funding, and more.

However, these capacity additions and emissions reductions range widely based on assumptions of how the IRA is implemented, and how bonus credits within the legislation are appropriated. Low-case projections for IRA bonus content place renewables buildout in a similar range to a no IRA environment, suggesting that there is still a need for guidance from authorities to evaluate the true effect of the historic legislation.

EIA’s reference case places cumulative solar deployment at 920 GW by 2050, about 194 GW more than the no IRA case. The administration’s Issues in Focus: Inflation Reduction Act Cases in the AEO2023 takes a deeper dive into the 16 scenarios that may unfold.

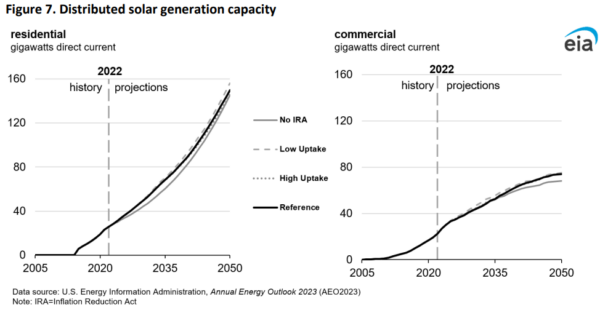

As seen below, in the distributed generation space, EIA expects a strong rise in adoption of residential solar through 2050. Commercial solar is expected to peak out around 80 GW of capacity mid-century, while residential solar will continue to sharply rise towards 160 GW of deployed capacity. EIA projects that over 19.5 million U.S. households will have adopted solar by 2050.

In the reference and high renewables uptake cases, CO2 emissions from the electric power sector decline about 72% to 75% by the end of the projection period below the 2005 levels. This is compared with a 58% reduction in a no IRA case.

Upon passage of the IRA, Nat Kreamer, chief executive officer of Advanced Energy Economy said, “Clean energy manufacturers and developers alike will now have the right financial tools and the policy certainty they need to produce and buy the components that power these innovative technologies here in America. That’s going to translate into millions of family-supporting jobs and billions in energy savings for American households.”

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.