I stared at the slide intently, trying to identify the mistake buried in the math behind the charts. The presentation to our investment committee outlined a portfolio of projects – at this point they were merely seedlings with little more than site control – worth well over $1.00/w each….in net margin. This was a meeting about an emerging market in the US with projected 2020 in-service dates, not a meeting about California rooftop CSI projects in 2010. I was not buying it, and the body language in the room suggested I wasn’t alone.

“Um, sorry guys, I have to stop you. I’m not saying we shouldn’t be really excited about these projects and supporting them confidently, but you do realize that at the end of the day we’re not getting those margins, right?”

I was met with silence, glances around the room and more silence, until a senior developer spoke up.

“I think it’s right. Check the model, tell us where it’s wrong.”

I knew that soon our team would be inheriting these development aspirations as project finance team expectations, so I accepted the invitation.

I couldn’t find anything “wrong.” The model was thoughtfully constructed and as “right” as it could be, with defensible, moderately conservative assumptions. After years of incessantly lecturing folks not to debate and whine about the outputs of a model just because they don’t like the result, here I was not able to back up my claims at the assumption level. Yet I, and others on the investment committee, were still convinced we were right: there is no way those margins would ever hold. How did we know?

With enough time and reps observing the delta between early model value/margin estimates and final results, a clear theme emerges: projects tend to get sucked back toward the zero margin zone, and the further away they appear to be, the more their margins stand to drift over time.

Fancy models with bells, whistles, and defensible assumptions aside, I was confident the final picture would look much less rosy.

Fortunately, this trend holds on both sides of zero. Just as fat margins thin considerably over time, projects facing a loss often scrape and claw their way into the black. Hence the “rubber-band effect” – all projects feel the gravity of zero margin, regardless of where they start on the spectrum of profitability.

Why does this happen? Why can’t we trust development-stage models replete with high margins and rich IRRs or discard nascent opportunities when we realize our initial EPC estimate is low by 20%?

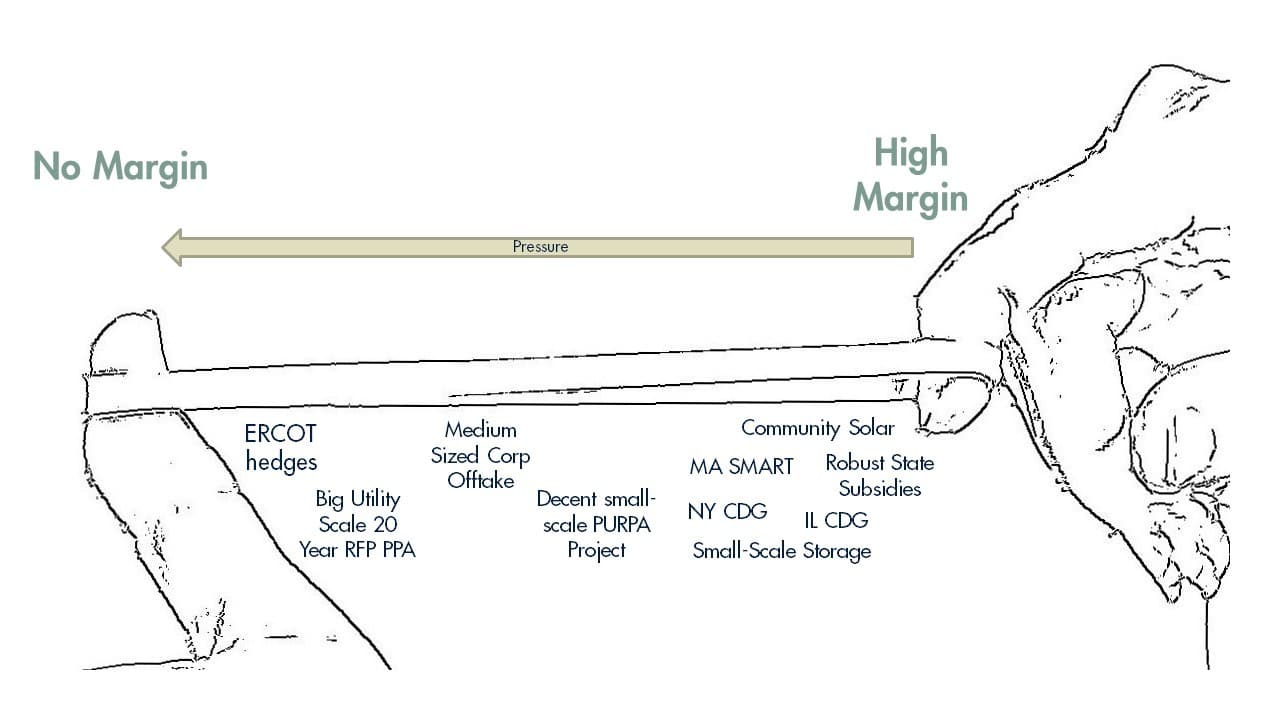

Downward Pressure

Let’s first consider projects which seem very rich at the concept stage.

Scarcity forces efficiency and abundance causes waste. It’s simply human nature. This phenomenon manifests itself internally, within the walls of the project developer/integrator, and throughout the expansive universe of external stakeholders.

Along the assembly line of developing and building a solar project, every cog in the machine has an opportunity to prioritize speed and progress over efficiency, eroding margin in the process:

Development team

Developers are often measured by their ability to get projects done, as much or more than their ability to generate profitability. Certainly, in a situation where profit erosion is less noticeable because the final margin is still attractive on an absolute basis, a developer could be forgiven for instinctively prioritizing progress and speed. After all, who will complain if a project ultimately clears with an $0.75 development margin instead of the whole $1?

Despite losing substantial value, it’s still a fantastic result. Maybe this manifests itself as particularly generous lease rate offers to landowner, taking the first bid from an injection study consultant or choosing not to challenge the utility on their feasibility study estimates.

EPC

Without the extraordinary pressures of a razor-thin project, maybe only 2 bids are sought for major equipment, instead of 6. Maybe the design and engineering team chose “safe” designs which prioritize construction velocity over cost. EPC teams are often asked to perform minor miracles by squeezing costs out of builds on the fly, but the impetus to do that is usually a project at risk of being underwater. The notion that cash is fungible is easy to forget, so those holding an EPC firm/group’s feet to the fire may be saving their “please perform a miracle” bullets for tighter projects.

Project Finance

When a flow of funds with fat margins looms on the horizon, there is often a lot of pressure to get to flow of funds day as quickly as possible. Just like everyone else, project finance professionals must make trade-off choices between speed and quality. With less time comes sloppier execution and less room for creativity. The goal becomes completion, not perfection. Like the EPC group, project finance folks have to ration themselves when it comes to applying pressure to their partners.

If I’m working on two deals with the same tax investor at the same time, one of them has $0.04/W of margin, and the other has $0.24/W – which one am I going to beg for higher credit pricing on? Which deal, generally, is likely to get more of my finite time and attention?

Often the very programs or regulatory regimes which facilitate higher margins also come with restrictions and requirements, which challenge margin realization. Certain Massachusetts programs had 9-month build cycle requirements and North Carolina state tax credits had placed-in-service deadlines. When staring into the abyss of potential disaster, altogether losing a massive value source, teams working to complete the project are not likely to quibble over a $25k change order, nor should they. In the same vein, state/local programs often come attached to local socioeconomic objectives which give preference, officially or unofficially, to local companies, which conveniently get overlooked when out-of-state firms consider pursuing an opportunity, only to experience years of headwinds not captured in early models.

Local economic development is just one example of sources of external pressure which can combine to create the effect of a feeding frenzy. When there is “room” in a deal, it’s usually either well-known, discoverable or at least felt by a variety of parties who may subtly adjust their choices and behavior to “get theirs.”

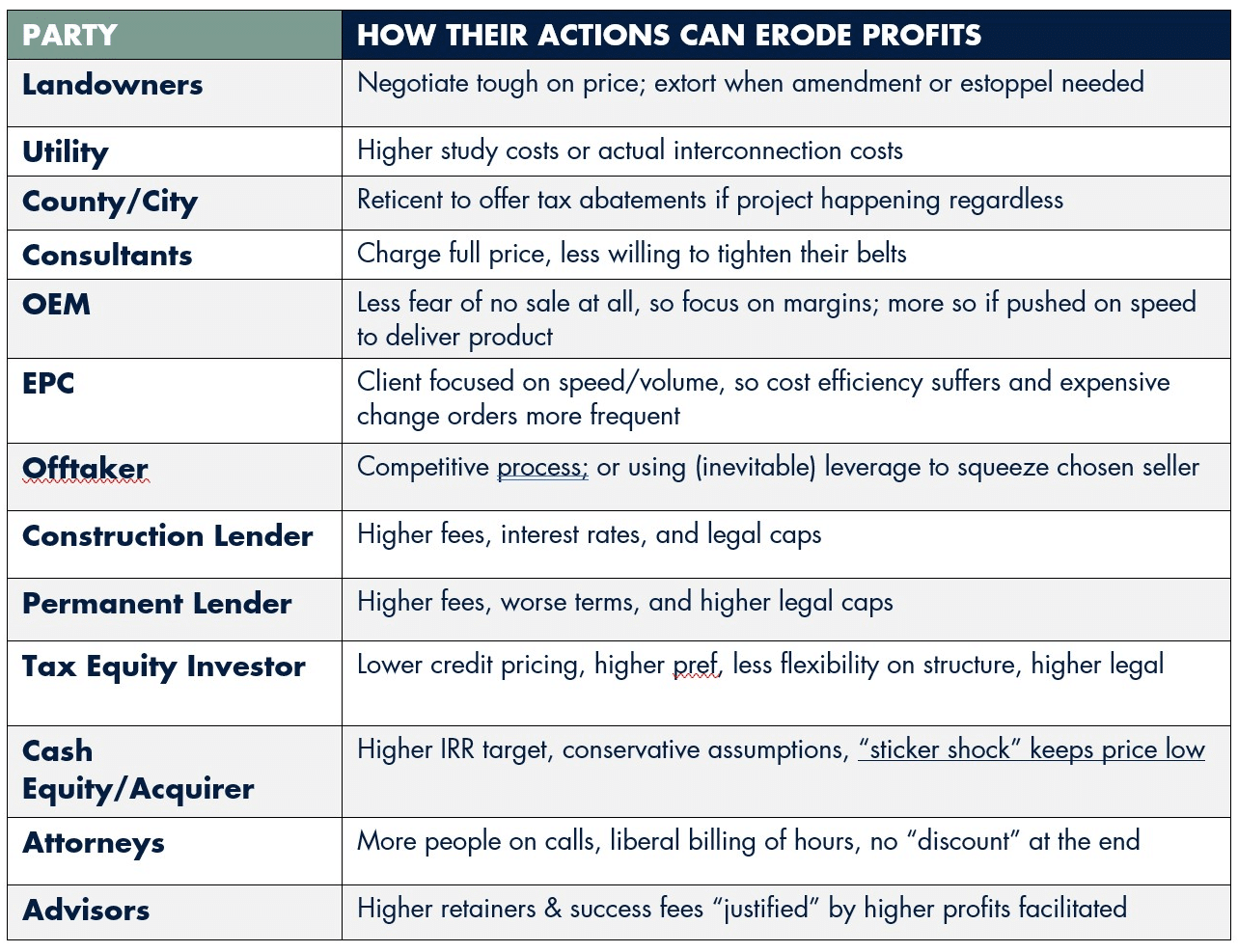

Just think about all the different groups who have a chance to grab at what would otherwise be developer margin:

Every one of those parties can seek to extract value that would otherwise go to the developer and has more leverage to get it, because the threat of killing the project is not credible. It also feels morally acceptable when the developer is doing just fine and the money grab won’t put them in the red.

That should not be read as judgement – in an industry riddled with dead deals and thin margins forcing every stakeholder to take a hit, we all have to make up for it somewhere.

Fair or not, profit erosion adds up. The important thing is to acknowledge the phenomenon, mitigate it to the extent possible and plan for some disappointment relative to expectations set by an early financial model.

Upward Pressure

Thankfully, there are two sides to this coin.

How many times have you asked yourself how RFP bidders could possibly bid such an impossibly low price in a PPA RFP, only to find out years later the winner(s) got the project done and appear to have even made a little money on it? No sane bid model could possibly have suggested that the price was a safe and rational number to bid, yet something made it work in the end.

Similarly, that experience of struggling to kill a seemingly underwater project in the pipeline because you just have a hunch it’ll find a way into the black.

Ever wonder how it is that most of us market participants remain optimistic about the potential to make a living in our industry amidst simultaneous headwinds from tariffs, sunsetting subsidies, sinking power prices, etc.?

I believe it’s a simple hunch: I don’t know exactly why or how, but one way or another, many of these power plants are going to happen and happen profitably. Anyone who has been participating in this market long enough knows that this is well-founded, if dangerous, intuition.

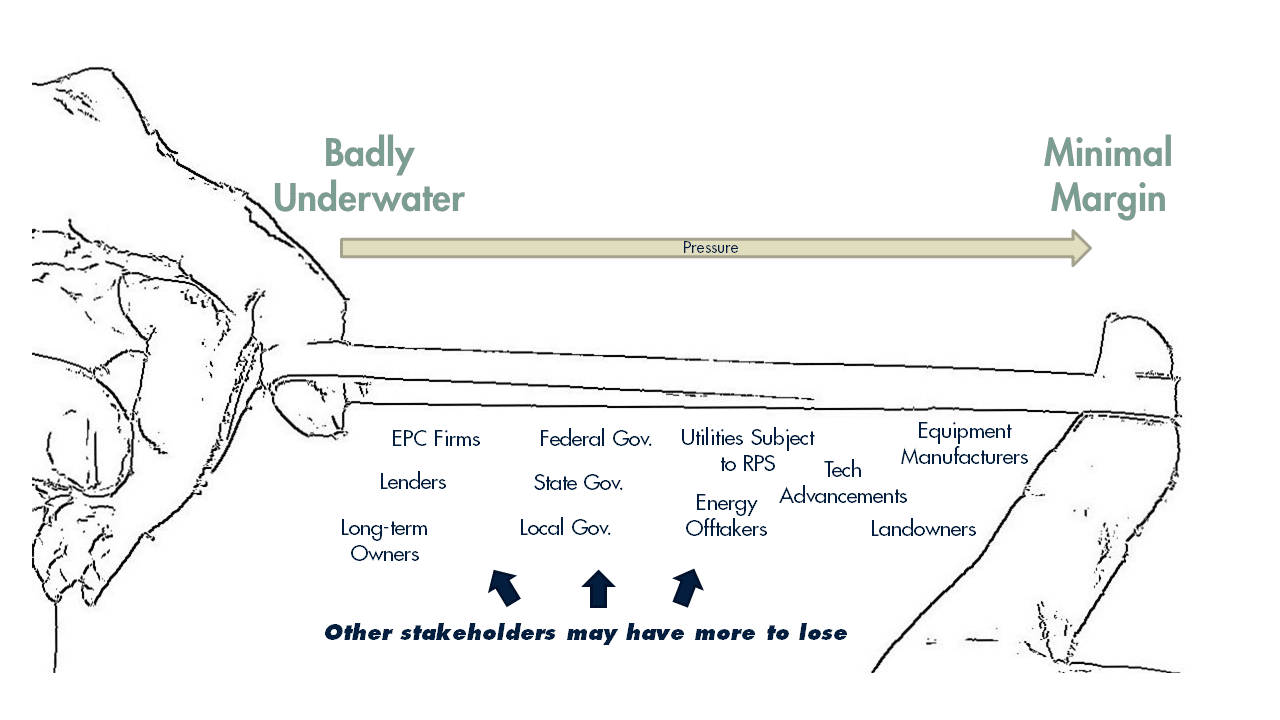

Consider the following framework for exploring why: which stakeholders will be harmed if this project is not built and who has the most to lose?

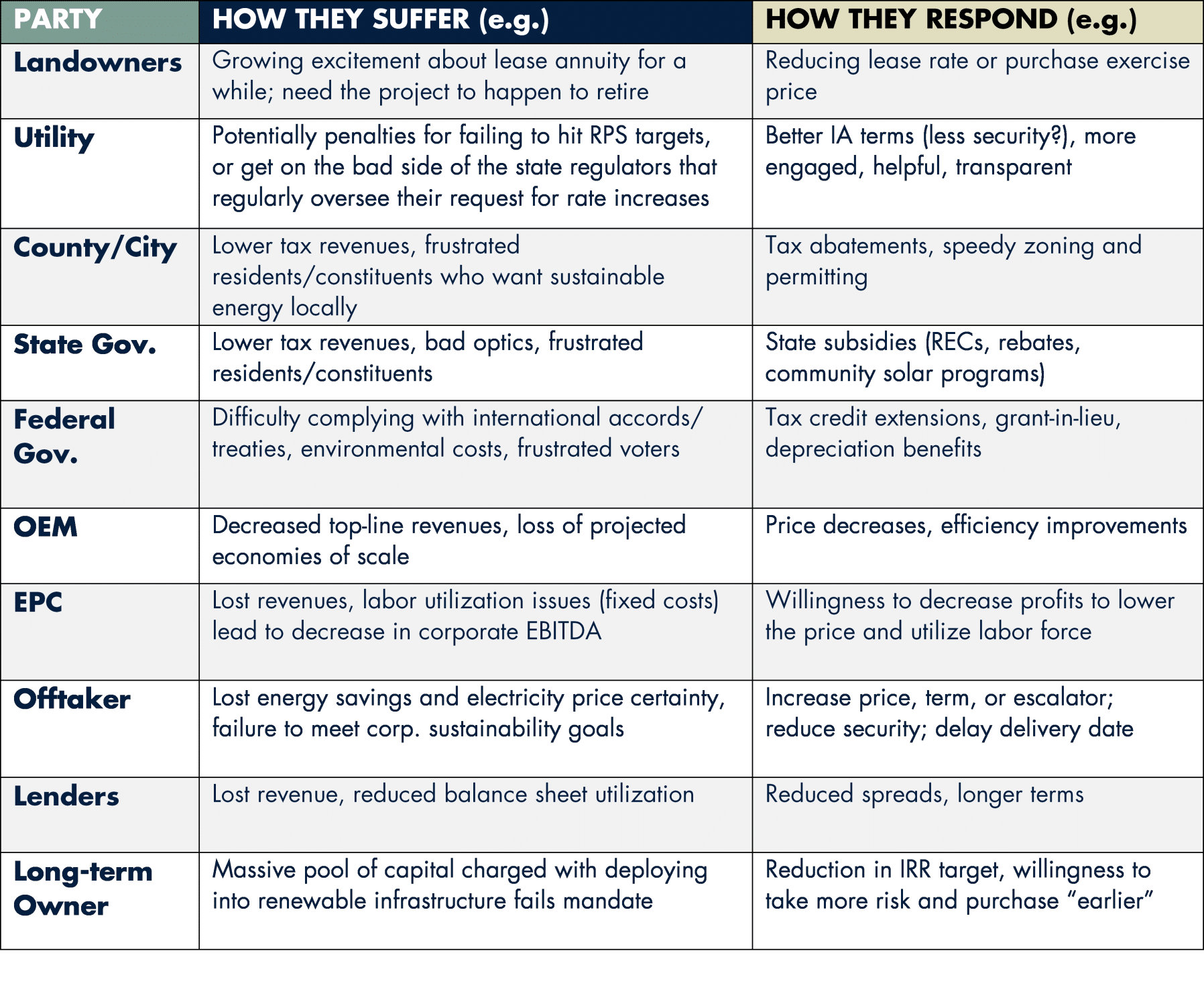

The regulatory environment and, to a lesser extent, the prevailing sentiment of voters, shareholders, ratepayers, or customers, imposes pressure on a variety of institutions, who face consequences if not enough renewable and/or storage projects get built. Perhaps more importantly, many stakeholders stand to suffer more economic pain as the result of a project dying than the developer would. In the same way developers lack leverage in high-margin projects, they can credibly threaten to bury a project and any associated benefits if it stands to lose money.

Taken individually, none are reliable behavioral patterns on the single-actor level. For example, utilities rarely change the terms of an interconnection agreement and energy offtakers are loath to adjust terms once signed. The overall theme holds: these are the types of reactions and responses we have seen over the years when thin-margin projects face the chopping block. Anticipating some help from other stakeholders-to-be-revealed-later is not delusional. In some cases, that expectation is mere table stakes. Were the ultimate source of the external “help” known and arrival assured, all players would bake it into their strategy and models.

In reality, the renewable energy and storage playing fields are too dynamic and multivariate to enjoy such visibility, so instead we are often asked to take a leap of faith that there’s a break or two of unknown origin out there for us if we sit tight. It is an intimidating proposition that occasionally fails to deliver, but here are a few examples from the last decade where help did arrive.

1603 Grant, 2009

The financial crisis obliterated the tax equity market as corporate profits, especially banks’, the primary source of tax equity at the time, evaporated. Unclear on how any project would be financed, many developers froze investment. But, the federal government made supporting clean energy a priority in the ARRA bill and instituted the 1603 “grant-in-lieu-of-tax-credit,” which allowed applicants to take the subsidy as cash from the US Treasury instead of a tax credit from the IRS. It served its primary purpose reasonably well, saving rooftop projects and the first utility-scale solar project in the country, but it also had the secondary effect of drawing in a new class of “cash investors” into the sector. That momentum, first catalyzed by the 1603 grant, is still felt today.

California CSI program, 2008-2014

In the early days of distributed generation, California decided the federal objectives for integration of clean energy fell short of the state’s objectives, so they instituted a performance-based-incentive to supplement the federal tax credit. It was a very powerful program that served to dramatically accelerate the adoption of solar in state, while providing healthy margins to residential, commercial, and industrial developers.

Module cost curve, 2010-2015

Cost reductions for solar modules exceeded even the most optimistic projections during the first half of the last decade. The Chinese government’s desire to bolster a burgeoning solar module manufacturing industry, which was a major source of domestic jobs, fueled the rapid cost declines. The China Development Bank and quasi-governmental financing institutions pumped incredibly cheap capital into module companies. Volume, market domination and job creation were the goals, not profitability. The math is simple: economies of scale + minuscule margins + abundant cheap capital = great module prices. Developers who took a bet on aggressive cost curves in 2009-2012 reaped major rewards.

YieldCo’s, 2013-2016

Terraform Power started a short-lived (but incredibly powerful) trend of publicly traded asset-ownership vehicles dominating the asset-ownership market, which drove project values way up in the process. Their appetite propelled both volume and profitability across the market for a few years. But for a few folks inside SunEdison and some bankers who like to retroactively reframe their optimism about “securitization” as prescience for yieldcos, few would claim they saw this market phase coming.

ITC Extension, 2015

Most of us were preparing for a world without the 30% ITC in December, 2015. Little did we expect the holiday miracle in a bill many believed dead: democrats and republicans horse-traded a lift of the oil export ban for a huge extension to the solar ITC and one-year extension to the wind PTC. The impact this rather surprising development has had on the industry since December 2015 cannot be overstated.

Socially/environmentally conscious offtakers, 2017 – present

Just as many regulated utilities across the country started to reach RPS targets, reducing their appetite for renewable PPAs, the community of corporate and municipal offtakers began to step up and directly procure sustainably generated electricity at a large scale. Google, Amazon, Microsoft, Starbucks, Facebook, Intel, Apple and many others have offered economically viable solutions to what looked like a looming dearth in renewable electricity offtake, while injecting competitive demand into a market getting stale from years of mostly regulated, subsidy-driven growth.

Equity cost of capital, 2017 – present

Throughout the previous decade, a staggering amount of “cash equity” investors – private equity, public infrastructure vehicles, pension funds, sovereign wealth funds – entered the renewable power plant asset ownership market. When the collapse of the yieldco market caused a brief cost of capital increase, many of us feared that projects we underwrote to aspirational yieldco IRRs would die in the red. Alas, these huge institutional pools of money quickly filled the void and continue to play a pivotal role in keeping the industry healthy today.

Bi-facial modules, battery storage, 2018 – present

A calamitous combination of module import tariffs, deteriorating tax equity terms and falling electricity prices left many solar projects staring into the abyss heading into 2018. Though plenty did in fact die, many have been saved by the emergence of production-boosting bi-facials and/or the integration of storage technology into system design and revenue strategies.

Arming inherently optimistic developers with this “upward pressure” argument is, frankly, a bit terrifying. Applied irresponsibly, this idea could be used to justify objectively awful decisions. Any way you slice it there’s a difference between taking calculated risks and gambling. A thoughtful, intentional application of the above would probably ask questions like: “What do I need to believe for this project to end up working?” or “what kind of ‘breaks’ would need to fall my way for this to have value, and what is the probability of those things coming to pass?” then judiciously weighing risks vs. potential reward. Shrugging off an indicative model that says a project (or PPA rate) needs multiple miracles to make five cents of margin is nothing more than a stubborn, reckless gamble.

Conclusion

For better or worse, the low/zero margin zone holds a lot of gravity. No doubt there are exceptions. Ironically, the example I chose to use at the top is arguably one – while many of the forces described earlier put downward pressure on those project margins, they proved to be an exceptionally good fit for a particular acquirer who paid prices in earshot of those I questioned. But developers have often made the mistake of planning for and around healthy margins coming to pass – building large teams, taking on debt, throwing self-congratulatory parties at SPI – only to find themselves in deep trouble when their $0.35/W expected margin actually came in at $0.21/W.

Whether manifested as a little extra patience with a laggard, or tempering expectations for richer projects, all developers and investors concerned with project profitability would be well served to remember that forces tend to pull margins back toward zero.

***

David Riester is a Partner at Lacuna Sustainable Investments, a firm investing in pre-construction (all-stages) renewable energy and storage projects/companies in the U.S. Lacuna is dedicated to creating strong partnerships with management teams in opportunities where capital and experience will accelerate value creation.”

The views and opinions expressed in this article are the author’s own, and do not necessarily reflect those held by pv magazine.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

More by this guy, please.

A well written, knowledgable piece. The large number of variables in project development and execution gives the uninitiated heartburn but this piece lays out well how the downward and upward pressure need to be understood in detail. The risk here is captured in this sentence: “Taken individually, none are reliable behavioral patterns on the single-actor level” which is in the Upward Pressure discussion but is relevant widely in the process. An example, a recent involvement with a county decision in MD to not allow a project to move forward due to an emotional income inequality based response was more than surprising considering the advanced state of the development.