With the U.S. Investment Tax Credit (ITC) set to phase down at the end of this year, the U.S. solar market is seeing not just a boom in construction to qualify for the full 30% ITC, but also a stockpiling of PV modules under the “safe harbor” provision of the policy.

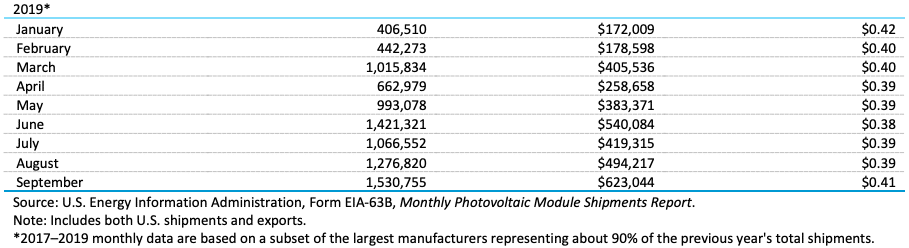

This has been documented by the latest information from the U.S. Department of Energy’s Energy Information Administration (EIA). EIA reports that 1.53 GW of PV modules were shipped in the month of September, more than double the volume a year ago and higher than in any month since at least 2016. This included 1.30 GW of imports.

According to EIA’s data 13.5 GW of modules were shipped during the full year 2016, but it has not released monthly shipment levels for that year, making a comparison impossible.

Many of these modules are likely bound for projects under construction. Wood Mackenzie has reported that at the end of Q2 there were 37.9 GW of utility-scale solar projects under construction in the United States – the highest level to date – and it is unlikely that construction has slowed down since then.

Part of the reason is the “commence construction” provision of the ITC, under which solar projects can quality for the full 30% ITC if they start physical work by the end of the year. Alternately, under the current IRS guidance developers can lock in the 30% ITC through the “safe harbor” provision, by paying for 5% or more of the cost of a project.

This does not apply to individuals, only businesses, meaning that homeowners buying PV systems outright still must complete work by the end of the year to get the 30% ITC. However, it does apply to third-party solar companies, and modules represent more than 5% of total project costs.

This means that there has been a rush to “safe harbor” modules, with Sunrun alone estimating that it will safe harbor 500 MW, and SunPower partnering with Hannon Armstrong to safe harbor 200 MW of projects.

U.S. module assembly on the rise

And while this included 1.3 GW of imports, there were also 230 MW of modules which were either exported by U.S. companies, shipped within the United States, or sold to U.S. contract manufacturers for resale. It is impossible to know how much of which, as EIA has redacted that data.

However, with manufacturers reporting year-long lead times to order modules, there is clearly a market for the new module assembly which has sprung up after the Section 201 tariffs and Republican tax cuts.

First Solar put online its 1.3 GW solar factory in Lake Township, Ohio last month, and while that one is still ramping Hanwha Q Cells’ 1.7 GW module factory in northern Georgia has been up and running for some time. When you add in the 500 MW LG factory in Alabama and the 400 MW JinkoSolar factory in Florida, the United States has much more module assembly than it has seen in some time.

Even this does not appear to have dampened the market, and EIA is reporting that the average price of PV modules shipped in September rose to $0.41 per watt – the highest level since January.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

“With the U.S. Investment Tax Credit (ITC) set to phase down at the end of this year, the U.S. solar market is seeing not just a boom in construction to qualify for the full 30% ITC, but also a stockpiling of PV modules under the “safe harbor” provision of the policy.”

This is the second time, installers have “stocked up” before tariffs have gone into effect. I’m just wondering this time, if the warehousing will be bifacial solar PV panels? The mention of modules shipped at $0.41 might suggest bifacial is being brought in with manufacturing quantities.

Just 15 years ago, solar PV panels were at $5.50/watt, now a “high” since January is $0.41/watt. One can now focus on having their very own energy storage system with their solar PV installation. Even at that comparing simple solar PV grid tied systems from 15 years ago, one can still install a relatively large solar PV system with energy storage, cheaper than solar PV 15 years ago, even with the rebate programs that were available then.