Data is often tough to come by. Some suggest it is the world’s most valuable commodity. Private companies sign NDAs with partners, with little bits of information coming through that make the partners happy – but not always enough for you readers and other developers who sometimes reach out to us asking for more. So we’ve got to appreciate those who give the world bits of their knowledge.

LevelTen has released its Q3 2019 PPA Price Index: a summary of transactions moving through its online power purchase agreement (PPA) marketplace of utility scale solar power projects averaging 108 MWac.

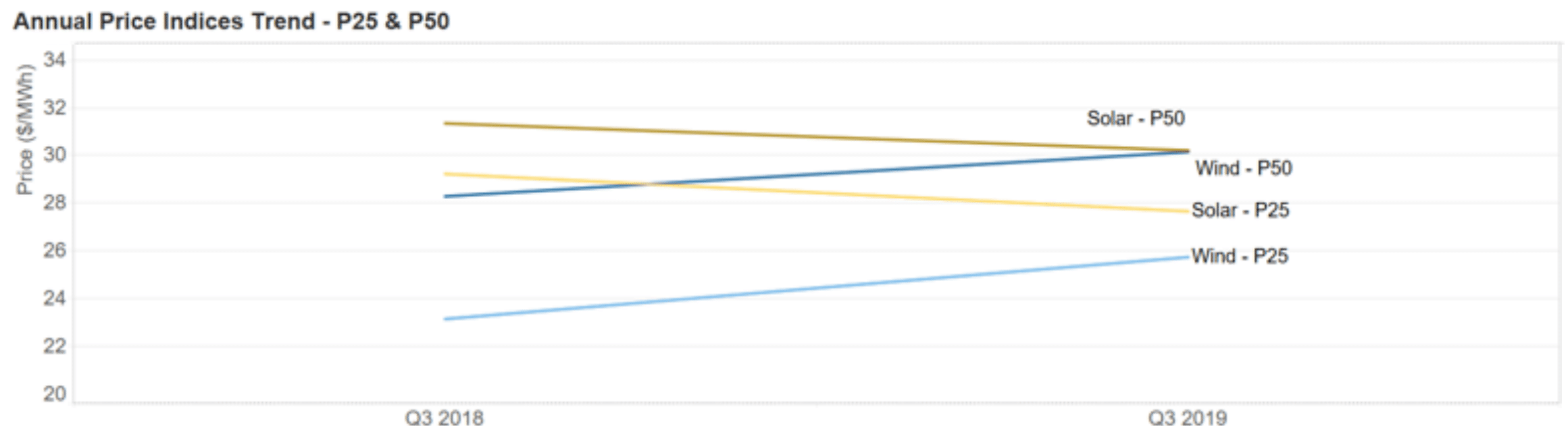

At the highest level, the group has seen solar power PPA pricing fall 5.4% since Q3 2018. Within the period there is variation, such as seeing prices fall 0.5% this past quarter after a moderate pricing increase of about $0.19MWh, 1.0%, in Q2, a healthy 7% fall in Q1, and a bit of a bump up in Q4’18. LevelTen surveyed their customers, getting answers from 33 of them, who report that corporate procurement was driving a healthy amount of recent demand, followed by utility demand, as well the continued price decreases of renewable energy in general.

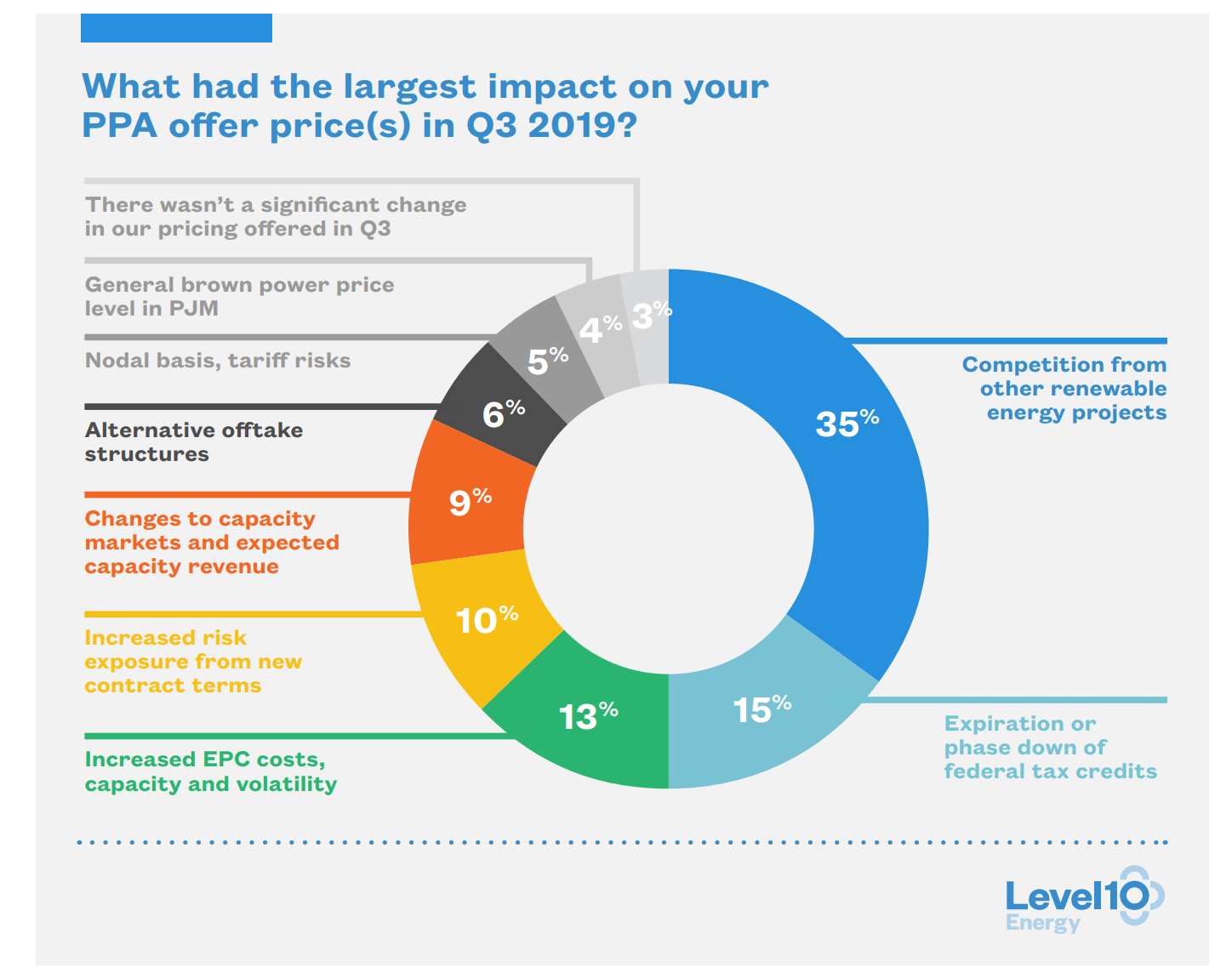

The above chart shows what these bidders felt most influenced their pricing refinements in the past quarter, and while the individual answers here didn’t have specific values associated with them, the average price did fall a small bit in the quarter. We can assume competition pushed prices down, while EPC costs, new terms, and phase down of tax credits pushed up.

The above chart shows what these bidders felt most influenced their pricing refinements in the past quarter, and while the individual answers here didn’t have specific values associated with them, the average price did fall a small bit in the quarter. We can assume competition pushed prices down, while EPC costs, new terms, and phase down of tax credits pushed up.

In a continuing trend we’ve covered in places outside of LevelTen as well, deal terms are shorter – compared to last quarter, average contract lengths solar projects decreased a bit from 14.0 to 13.9 years. In that separate coverage – pv magazine USA has also seen energy storage and solar projects go PPA-free in merchant and quasi-merchant projects. This suggests that project financiers are comfortable putting the big installation cash in up front.

Level Ten also asked where growth was projected to come from – and the northeast PJM region led, with Texas following, with everyone seeing some growth everywhere (even in Japan) – along with that aforementioned corporate+utility+price deductions. pv magazine USA sees broad growth across all of the regions, but there are complexities – like Massachusetts SMART program issues, newly arising procurement demands in California, and the Texas boom.

pv magazine USA has now covered four quarters in a row of Level Ten – pretty soon we’ll have a long-term catalogue to see how this group of customers aligns with how the the larger market has moved.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.