Energy storage is increasingly finding its place in the sun. As a technology, it simply offers too many advantages and meets too many needs to be overlooked: it can ramp faster than a gas plant, it can stabilize voltage and frequency, and it can carry electrons from solar generation to deliver power after dark.

When you add to this the dramatic cost declines for lithium-ion batteries, the combination becomes unstoppable.

Regulators, utilities and state governments are beginning to understand this, and among other policies the Federal Energy Regulatory Commission’s Order 841 is opening wholesale markets to the participation of energy storage. Add in the tax advantages of coupling energy storage with solar under the Investment Tax Credit (ITC), and you have the perfect storm.

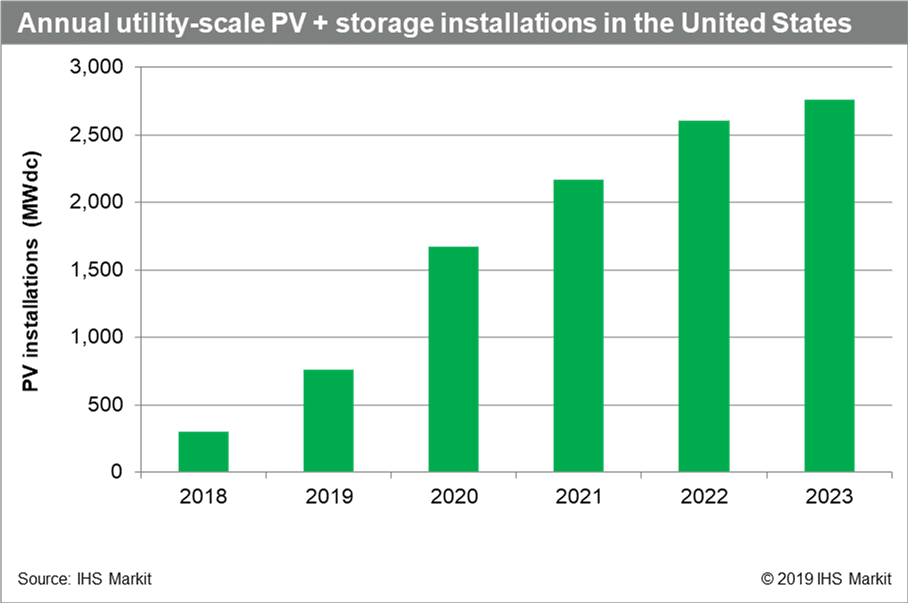

According to IHS Markit, the U.S. grid-tied energy storage market is poised to nearly double this year to 712 MW from 376 MW last year, including both transmission-connected projects and behind the meter storage. The company says that this will allow the United States to surpass South Korea, which was the world’s largest grid-tied energy storage market in 2017 and 2018.

And that is just the beginning. IHS expects nearly 5 GW of energy storage in projects connected to the transmission grid – 90% of which will be lithium-ion batteries – to be deployed in the United States from 2019 to 2023. (note: This portion of the forecast does not include behind-the-meter energy storage).

ITC drop down drives growth

The consultancy says that a big driver of the growth of energy storage deployments over the next four years will be batteries coupled with utility-scale solar, which it expects to comprise more than 40% of battery deployments for transmission-connected projects, or roughly 2 GW.

This is made possible by multiple factors, including falling costs. But a main driver of the growth over this period will be the narrowing window of opportunity presented by the ITC, which drops down to 10% at the end of 2022 and can be used for paired solar + storage if the batteries are mostly charged using solar.

The full 30% ITC can only be claimed if projects start construction by the end of this year, however because of this provision the completion of many large-scale solar projects is expected to be stretched over the full four years, and it is likely that solar plus storage will follow this pattern.

The rise of the solar + storage peaker

While IHS Markit identifies the pending expiration of the ITC as the biggest single impetus for the coupling of solar and storage over the next four years, this is a supporting factor and does not drive the need for this combination.

Instead, in states such as Hawaii and California with high deployment of solar, at times the supply of mid-day electricity is reaching saturation and there is still a need to provide electricity during evening hours. This is resulting not only in deflated returns on solar projects as mid-day power prices crash, but also curtailment.

Adding batteries to a PV systems directly addresses this problem, and the markets in these states and others with high penetrations of solar are the farthest ahead. As documented by pv magazine USA, the state of Hawaii recently approved contracts for six utility-scale solar projects coupled with batteries of equivalent capacity as the solar, at prices of $80-100 per megawatt-hour.

These solar+storage “peakers” where the capacity of generation is fully backed by battery capacity are the exception, not the rule. Overall, IHS Markit expects the 2 GW of batteries to that will be deployed with solar from 2019-2023 to be paired with 10 GWdc of solar – or a 5:1 ratio of DC solar capacity to storage capacity (Editor’s note: in terms of AC capacities of PV systems, this ratio will likely be closer to 3:1 due to overbuilding). This keeps costs low, and even at a 4:1 pairing of solar and battery storage IHS Markit estimates that costs of under $40 per megawatt-hour can be achieved – assuming that the full ITC is claimed.

And it is not only California and Hawaii where these solar + storage projects are being built. pv magazine recently covered a 180 MW solar + 60 MW battery project that was approved by the state siting board in Ohio, with even larger projects in the interconnection queue of Texas’ grid operator.

Of course, much larger opportunities are on the horizon. IHS Markit predicts that by the time the ITC drops down to 10% in 2023, solar plus storage will be cost-competitive with new gas plants. And from there on out, it will be a very different market.

Correction: This article was corrected at 10:57 AM Eastern Time (U.S.) on May 22. An earlier version specified that the 376 MW and 712 MW figures for U.S. energy storage deployments in 2018 and 2019 did not include behind-the-meter storage systems. This was incorrect, and the text has been changed to reflect that this includes both transmission-connected and behind the meter storage.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

A five-year projection of 5 MW of storage with the first year estimated at 712 MW seems to predict a somewhat less-than-imaginable rate of growth. I wonder if IHS foresees a worldwide constraint in supply of batteries during this time frame.

Agree that it is pretty pathetic growth rate of only 13% per year. Especially when they are predicting nearly 90% growth this year.

I think you must be right they are predicting a battery constraint. Which might make sense for 2-3 years, but battery production is growing.

It seems like China ‘owns’ the mass manufacture of Lithium Ion technologies. In 1992 a company in Nevada, Altair-Nano produced the first rugged lithium ion battery technology. The problem is two fold, Lithium Titanate or LTO was developed by Altair-Nano, but is not as energy dense as other, less stable lithium ion battery technologies. LTO is from 80Wh/l to 100Wh/l, where the Lithium, Nickel, Cobalt battery is around 200 to 250Wh/l. The LNC ion battery is good for maybe 2,000 deep charge/discharge cycles. LTO is good for 10,000 to 20,000 deep discharge cycles, more if DOD is kept to the 65% to 70% DOD over the battery pack’s lifetime. Personally, I would like a storage battery that could be charged and discharged twice a day and still last 27 years.