It’s well known that North Carolina has driven solar development in the southeast. North Carolina’s implementation of PURPA kick-started a utility-scale solar market that helped the state rise to second in the nation in terms of total installed capacity, a crown it should be proud to wear, but hold onto tightly, as the throne it sits on is not a safe one.

The Southern Alliance for Clean Energy has released its second annual Solar in the Southeast report, highlighting the region’s development and state standings over the last year. What stood out this year was that growth was not limited to the usual suspects, showing that the region is more dynamic as a whole than it has ever been.

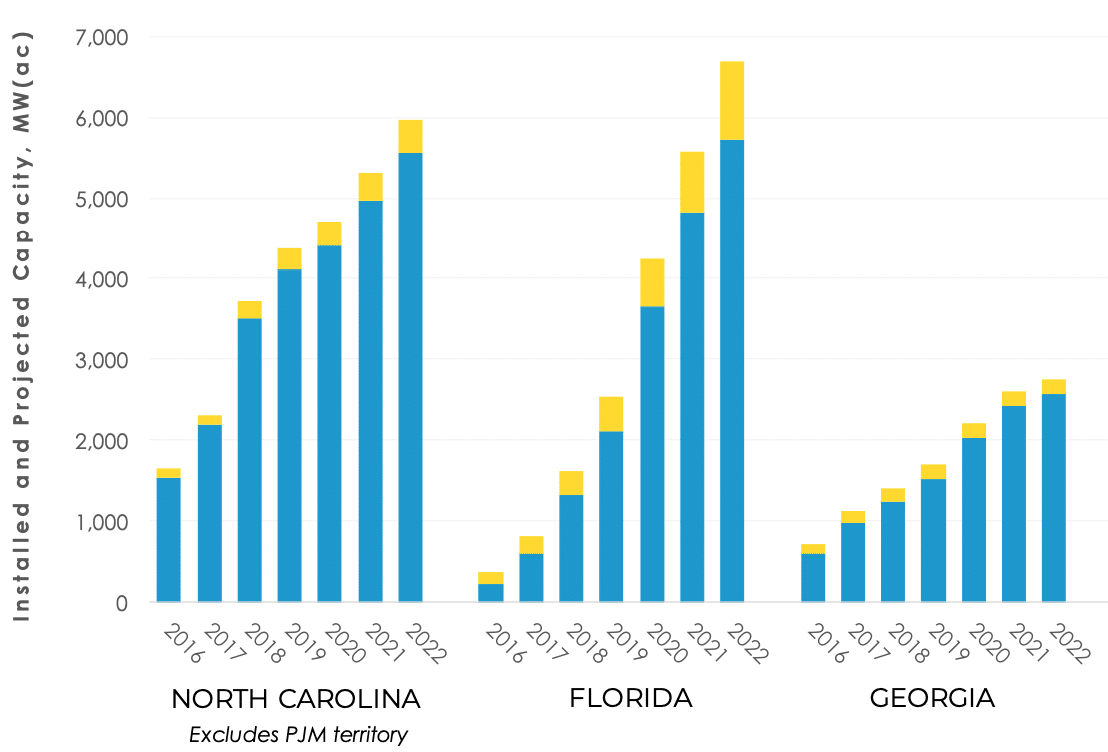

Part of the shrinking disparity in development has come from two of Florida’s utilities; Tampa Electric and Florida Power and Light (FPL). Specifically, FPL’s 30 x 30 plan to add almost 10 GW by 2030 is driving the momentum that is expected to allow Florida to overtake North Carolina for the region’s top spot by 2022.

That massive spike in blue in Florida from 2019 to 2020 represents the first step of the ’30 x 30′ plan, which will add roughly 1 GW in utility-scale projects per year. While utility-scale development between the two states is similar in that time period, it’s the growth of distributed solar, which Duke has successfully limited in its service area, that is poised to set Florida over the edge.

FPL isn’t the only company driving development, as three Florida utilities are expected to rank above the regional average for watts per customer by that 2022 mark. Tampa Electric is set to lead the way with 934 watts/customer, followed by FPL at 734 and Duke Energy Florida at 676.

Speaking of utilities, the graphic below shows how each one stands in installed capacity as of the end of 2018:

The region’s utilities hit a collective 8,035 MW in capacity last year, with that number expected to reach 10,000 by the end of this year, 17,000 by 2021 and nearly 20,000 by the end of 2022. So for an area that has, outside of a few, historically underperformed, the future is looking bright.

TVA comes in behind IOUs

However when talking about the Southeast, it’s hard to ignore the areas that have historically lagged in solar development. To the surprise of many, Tennessee Valley Authority (TVA) announced over the course of the last year a total of 677 MW of new solar projects, 377 MW of which are to be located in Alabama, with the other 300 MW going to Tennessee. This unprecedented growth is driven by utility-driven development, but rather procurement by tech giants Google and Facebook.

This is reflected by the prediction that TVA will add only 167 watts/customer by 2022, a mark that is bested by even Alabama Power, which is poised to add reach 335 watts/customer, up from 67 in 2018. TVA is predicted to add so little solar by 2022, that it joins the Seminole Electric CO-OP, NC Electric Cooperatives and Santee Cooper as the infamous list of companies whose 2022 watts/customer averages are set to be below the region’s 2018 average.

But, while those utilities may be slow to embrace solar, they are luckily not the only ones that spur development. The emerging interest of big tech companies to invest in the area is an encouraging prospect, especially if it continues in the service areas of these underperforming utilities. And, as weak as the bottom may be, we’re set to witness a national heavyweight bout for both regional and national solar prestige among the region’s two top players, with South Carolina and Georgia set to make strides as well.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

In Florida they are just putting in solar so they can not pay much for DR, behind the meter solar.

Also likely in 2020 we’ll have a free market grid like Texas if it isn’t stopped by the utilities, solar utilities will beat the pants off FPL, Duke, TECO.

Already microgrids are legal and with solar matching our demand so well, will be hard to beat.

Especially as EVs become the on demand storage, generation choice along with home, business battery packs solves the storage

problem..

And home, building RE fueled CHP solving much of the winter power needs.