As solar power has moved from a niche to a significant part of our electricity system, the Department of Homeland Security’s Federal Emergency Management Agency (FEMA) has noticed, and put out best practices for design, installation and maintenance of rooftop solar panels to manage hurricanes.

And as renewable electricity pricing continues to fall, while bottom up customer pressure grows, corporate procurement volumes have knocked it out of the park as well. But as pv magazine highlighted yesterday, there are of risks associated with the most common corporate tool – power purchase agreements (PPAs). And even though the first practical, modern solar cell was produced in 1954, the business models are much younger – as most every securitization of solar power notes the relative age of the industry techniques relative to recent business cycles.

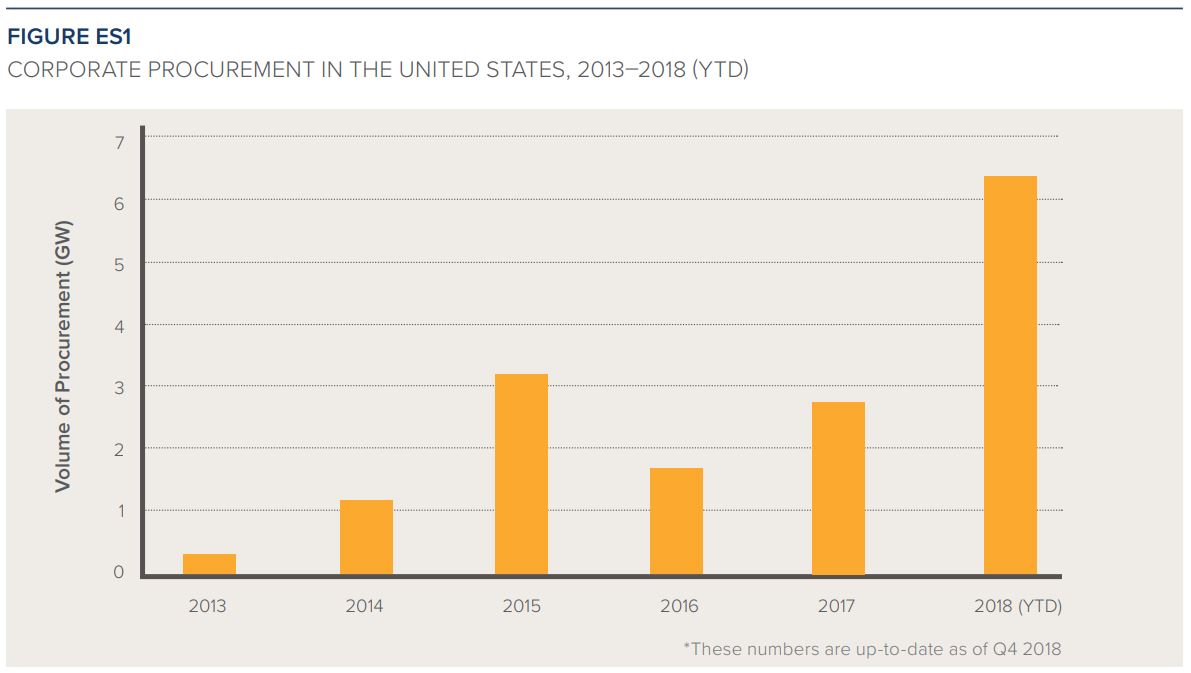

In A Corporate Purchaser’s Guide to Risk Mitigation (registration required), Rocky Mountain Institute (RMI) notes that corporate renewable energy procurement drives 12% of all utility scale wind and solar deployment in the United States – and the volumes are increasing. With this, RMI recommends corporate buyers better educate themselves on five specific risks commonly faced – price, shape, basis, volume, and operational risk – and some of the emerging tools used to manage them – hub-settled contracts, floors and collars, proxy generation, volume firming agreements, and fixed volume swaps.

As PPAs represent 12 GW of the 16 GW deployed to date, they are the most common mechanism for corporate renewable energy deals. The report highlights risks that are are specific to the wholesale electricity market, and are thus risks that corporate entities do not encounter in their core business operations.

As PPAs represent 12 GW of the 16 GW deployed to date, they are the most common mechanism for corporate renewable energy deals. The report highlights risks that are are specific to the wholesale electricity market, and are thus risks that corporate entities do not encounter in their core business operations.

RMI also suggests that the heavy volume of PPAs relative to all renewable deals is actually representative of limitations in the market as the breadth of needs that corporate buyers have is far wider than can be met with PPAs alone. Thus new mitigation and procurement strategies such as long-term renewable energy certificate (REC) agreements, project tranches, and contract tranches are explored.

This leads toward RMI suggesting best practices for buyers to contract for off-site renewable power in a way that meets their risk priorities. To do this they break down purchasers into three business types – SuperComputer, Regular, and Heavy Metal – as a tool to help think about differing needs.

It is no longer activist voices proclaiming the coming of change in the energy industry, it is now utilities shutting down coal plants early, saying that they will not build new gas and coal plants in the future, and whole states moving towards 100% clean energy. But the reality is that if solar and wind are going to take over the number one energy spot (which EIA notes is already happening with new electric generation capacity), then they will need to broaden their offerings to better align with the very large ocean of electricity buyers in the world.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.