Trade wars and rapid, negative policy changes in the United States and China aren’t helping the ability of solar companies to raise money, as is reflected in Mercom Capital’s latest quarter report on funding and mergers and acquisitions in the solar industry.

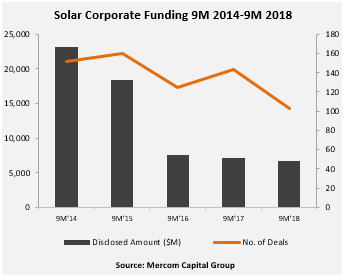

Mercom’s Q3 report shows total capital inflows to the solar industry for the first nine months of this year at slightly below what they were in Q1-Q3 of 2017, with a total of $6.7 billion. Despite public market funding rising 80% to $1.8 billion, venture capital (VC) investments were down 10% to only $889 million and debt financing fell 21%.

Mercom’s Q3 report shows total capital inflows to the solar industry for the first nine months of this year at slightly below what they were in Q1-Q3 of 2017, with a total of $6.7 billion. Despite public market funding rising 80% to $1.8 billion, venture capital (VC) investments were down 10% to only $889 million and debt financing fell 21%.

Among the companies that did receive VC investments in Q3, by far the largest announced deal benefitted U.S. developer Cypress Creek Renewables, which raised $200 million.

But as of Q3, Mercom reports that clean energy companies across the board are seeing depressed stock valuations as the top three markets – China, the United States and India – struggle with trade wars an policy changes.

“Decline in solar demand around the globe has had a strong effect on corporate financing activity in solar especially with most solar company stocks in negative territory at the end of the third quarter,” said Raj Prabhu, CEO of Mercom Capital Group.

There are some caveats to the gloom presented in this report. The first is that Mercom, like anyone in this industry, can only report deals that have been announced. For example, LONGi has built tens of gigawatts of ingot and wafer manufacturing capacity in China over the last few years, and got the money to do that from somewhere. However, the movement of capital in China can be more opaque, and if a company is merely reinvesting capital from its own revenues, this will not show up.

But the recent market changes have hit everyone, including LONGi.

“China’s solar policy change, resulting in a lower solar target and a cut in solar subsidies, has affected the solar supply chain globally,” notes Prabhu. “The solar cell and module oversupply situation, due to China policies, has hit manufacturers. Solar trade tariffs have weakened project pipelines in India, the U.S. market is also not expected to grow significantly this year. All these factors are reflected in the solar public company stocks, most of which are down in 2018 making fundraising challenging.”

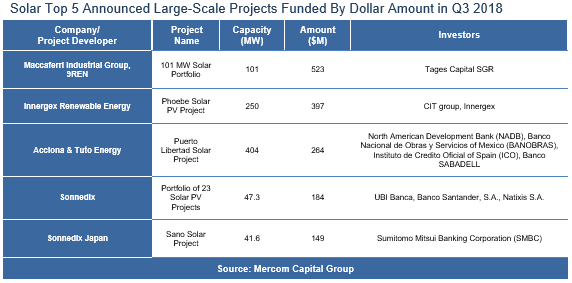

And as manufacturing in particular continues to burn the fingers of investors, many have moved to solar projects. Mercom reports that announced large-scale project funding crossed $11 billion for the first nine months of 2018, and Prabhu notes that project mergers and acquisitions have been particularly robust, with 24 GW of projects changing hands.

“Solar projects continue to be a coveted asset class in the investment community as generating solar assets are now considered mature, producing low risk, attractive returns over 25 years,” Prabhu explains.

This maturity is reflected by who now owns many of these assets. While in previous years many large developers built yieldcos to hold completed solar and wind projects, as widely reported by pv magazine most of those held by solar companies have been sold off to asset managers, such as Capital Dynamics’ acquisition of 8point3 Energy Partners and Brookfield’s acquisition of TerraForm Power and TerraForm Global.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.