Every time a portfolio of solar power based securities earns an A rating, an angel gets its wings. It’s somewhere in the contract – it’s true.

The Kroll Bond Rating Agency (KBRA) has delivered preliminary ratings Mosaic Solar’s most recent security offering. The whole of the portfolio, Mosaic Solar Loan Trust 2018-2-GS (46 pages), was found to be worth $317,522,000.

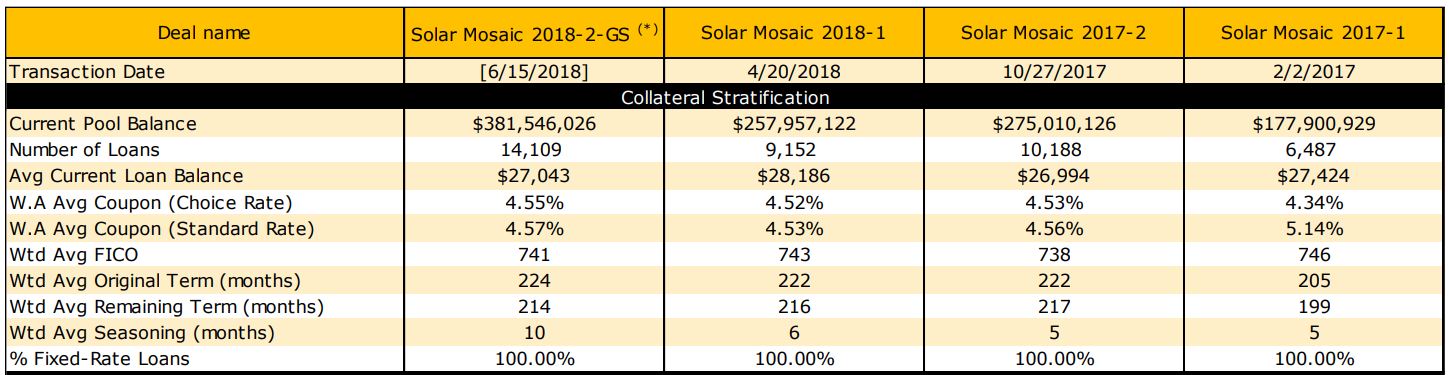

The portfolio’s original value of $381 million has been paid down, leaving 17.8 years – with an average ‘seasoning’ of ten payments. The average current balance is $27,043, with an interest rate of 4.55%. The average FICA core is 741, and 94% of the pool balance is paid via ACH. There are just over 14,109 accounts in the portfolio.

The report noted that ‘layering’ of risks, and the chance at multiple factors occurring at once, could increase rates of default higher than expected. Specific risks noted:

limited performance data and use of proxy data, the impact of manufacturers, installers or performance guarantors failing to honor their warranty/guarantee, collateral with interest rates and/or monthly payments that may increase, longer term consumer loans, changing technology and O&M risk born by the borrower.

It was also noted that Mosaic is a relatively young company, privately held and “has incurred significant operating losses and negative cash flow since inception.”

While Mosaic does pull from many states – 32 plus the District of Columbia, it was noted that this portfolio saw the concentration of receivables in the top five states of 72.98%. California borrowers represent 43.74% of the outstanding principal balance of the April 30, 2018 pool. The next larges state concentrations are in Arizona (9.04%), Texas (7.13%), Utah (7.03%) and Florida (6.04%).

This is at least the fourth securitization through KBRA that Mosaic has done. The total of the four deals are just over $1.09 billion.

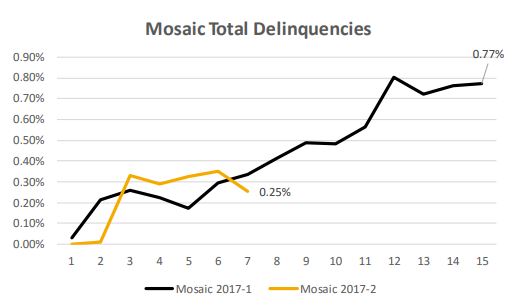

Portfolio side, for the two portfolios from 2018 – Mosaic 2018-1 and the current 2018-2 – the current delinquency rate is below 0.01%. All accounts must be current to be included with the portfolio when it is delivered to investors.

2017 portfolios, 2017-1 and 2017-2, have been seeing an increase in delinquency rate but are holding well under 1%.

With Mosaic Solar breaking a billion through KBRA alone, and so many other groups doing well in this market – Dividend getting an AA, equity groups buying developer pipelines – we’re building a backend of experience in the global financial markets. The backend will soon be defined as broad liquidity – and broad liquidity brings significant market opportunities.

And while we did see the residential market drop in 2017, we’ve seen it flatten in Q1 2018, but new technologies might offer opportunity to grow volumes and loan sizes. With Mosaic’s portfolios pulled from 2017 and 2018, it might be challenging to surmise the growth opportunities in the market as a whole – however – it is clear Mosaic has taken a larger share of the marketplace.

Globally, there are hundreds of trillions in potential investment capital. The solar industry would be happy with one or two of those – we got about $160 billion of it last year.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.