It has been nothing short of a war. In regulatory proceedings and courtrooms throughout the United States, the solar industry, renewable and distributed energy advocates have had to fight tooth and nail against utilities to keep policies that will allow solar to survive and thrive.

The boundaries of this war have evolved over the last decade, with an increasing number of utilities embracing utility-scale solar but continuing to stubbornly resist distributed solar, at least that which they do not own or at least control.

There are fundamental economic reasons why utilities resist distributed generation. Some of these are technical, but many stem from legal and regulatory structures and assumptions about the role of utilities and what constitutes a natural monopoly.

This is going to have to change.

The latest report by Rocky Mountain Institute, Reimagining the Utility, takes this need for change as its basic assumption, and looks at how electric utilities can evolve to meet these changes including both decarbonization through renewable energy and the rise of behind the meter resources.

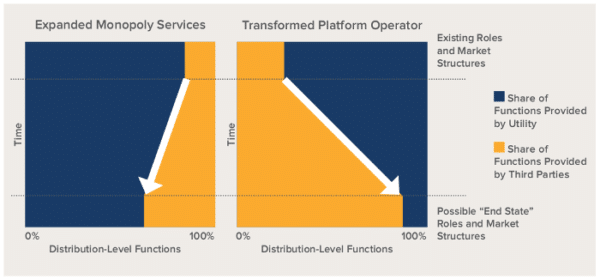

RMI charts two basic paths that utilities can take. Either they can maintain their monopolies but offer the new services that customers, regulators and legislatures are mandating, or they can transform into platform operators.

The tension between these two options can be seen in grid modernization proceedings like New York’s Reforming the Energy Vision (REV), which is attempting to open the distribution grid to competition, and RMI describes REV’s Distribution System Platforms as providing “the most visionary example” of this.

As is being seen with REV, it will more often be the case that utilities – which have often resisted being limited to platform operators – will end up in some hybrid model.

But whatever the case they will not be alone. A primary conclusion reached by the report is that whether or not utilities hold on to their monopolies they will increasingly be interacting with other service providers, either as contractors, competitors, or both.

RMI also notes that the many of the opportunities in the future will not be under current utility functions, but for third party service providers. Additionally, not all efforts that insist upon monopoly control while offering new services will succeed, and RMI cites the failure of Southern Company’s attempt to provide distributed solar to its customers.

But it will not only be utilities which decide which path to take. As in New York and grid modernization proceedings around the nation, it will be up to regulators to shape the roles and boundaries of utilities in future energy systems. And in this process we will see just how much vision these regulators will show – and how much “regulatory capture” will hinder evolution.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.