The U.S. energy storage market over the last few years has been a true roller coaster. As measured by either capacity (megawatts) or duration (megawatt-hours), the amount of storage deployed has swung wildly from quarter to quarter.

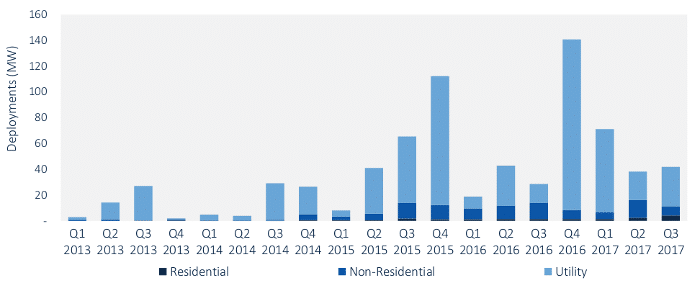

And coming in the aftermath of more than 200 MW deployed during the fourth quarter of 2016 and the first quarter of 2017 – largely due to California’s need for capacity following the Aliso Canyon gas leak – Q3 was another quarter of relatively subdued deployment. In its quarterly Energy Storage Monitor, GTM Research reports 42 MW of energy storage deployed nationally, a 10% increase over Q3 2016.

GTM Research

Nearly 2/3 of this comes from a single 30 MW battery storage system in Texas. And while the commercial and industrial segment had a slow quarter with only 6.8 MW deployed, residential storage reached a record 4.2 MW.

GTM Research attributes this boom in the residential sector largely to California’s Self-Generation Incentive Program (SGIP), the first few rounds of which were fully subscribed even at the increased budget levels recently approved.

Storage in IRPs

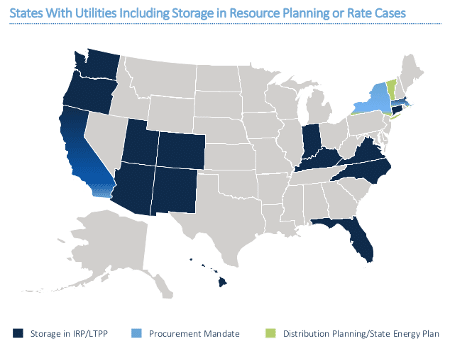

But if one looks too much at the quarter-to-quarter changes in deployment, it is possible to miss the forest for the trees. Increasingly, U.S. utilities are finding a place for energy storage in their long-term plans, and GTM Research reports that utilities in 15 U.S. states have included energy storage in either their Integrated Resource Plans or Long-Term Plans.

But if one looks too much at the quarter-to-quarter changes in deployment, it is possible to miss the forest for the trees. Increasingly, U.S. utilities are finding a place for energy storage in their long-term plans, and GTM Research reports that utilities in 15 U.S. states have included energy storage in either their Integrated Resource Plans or Long-Term Plans.

“Energy storage is increasingly acknowledged in utilities long term resource planning across the country, said Ravi Manghani, GTM Research’s director of energy storage. “Many utilities that hadn’t considered energy storage in IRPs a year or two ago are now explicitly modeling hundreds of megawatts of storage into their resource stacks.”

Manghani says that in these plans, utilities are also increasingly mentioning the multiple benefits that storage can provide to the grid. However, not all of the action here is voluntary. Led by California, four U.S. states have also set mandates for utilities to procure energy storage.

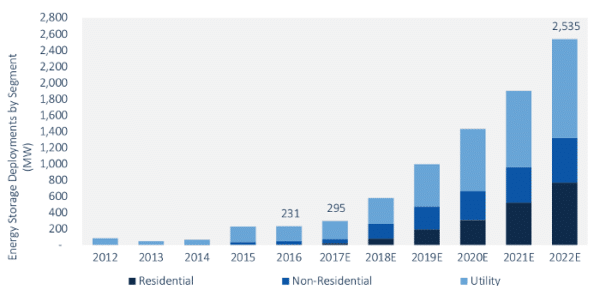

Overall, the combination of utility recognition of the increasing benefits of storage coupled with policy action is expecting to drive increased deployment. Despite the boom in Q4 2016 from the Aliso Canyon deployment, GTM Research still expects energy storage deployment to increase 28% over the course of 2017 to 295 MW.

And this is only the beginning. The company predicts that energy storage deployment will grow by an order of magnitude by 2022, with an estimated 2.5 GW deployed during that year, for a total market value of $3.1 billion.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.